Lloyds Banking Group (LSE: LLOY) shares look like a classic UK income stock on the surface: low valuation, decent dividend, and a giant retail footprint.

But the real story is more like a macro trade.

As the UK’s largest retail bank, Lloyds holds a 16.8% share of UK mortgages (£52.7bn), making it also the biggest lender.

So if Lloyds is so dependent on the UK mortgage market, is it really an income stock — or a disguised bet on Britain’s mortgage cycle?

A cash cow, or a housing cycle proxy?

When Bank of England rates rise, Lloyds can earn more on new mortgages and linked loans. When they fall, the bank risks margin pressure and slower lending growth.

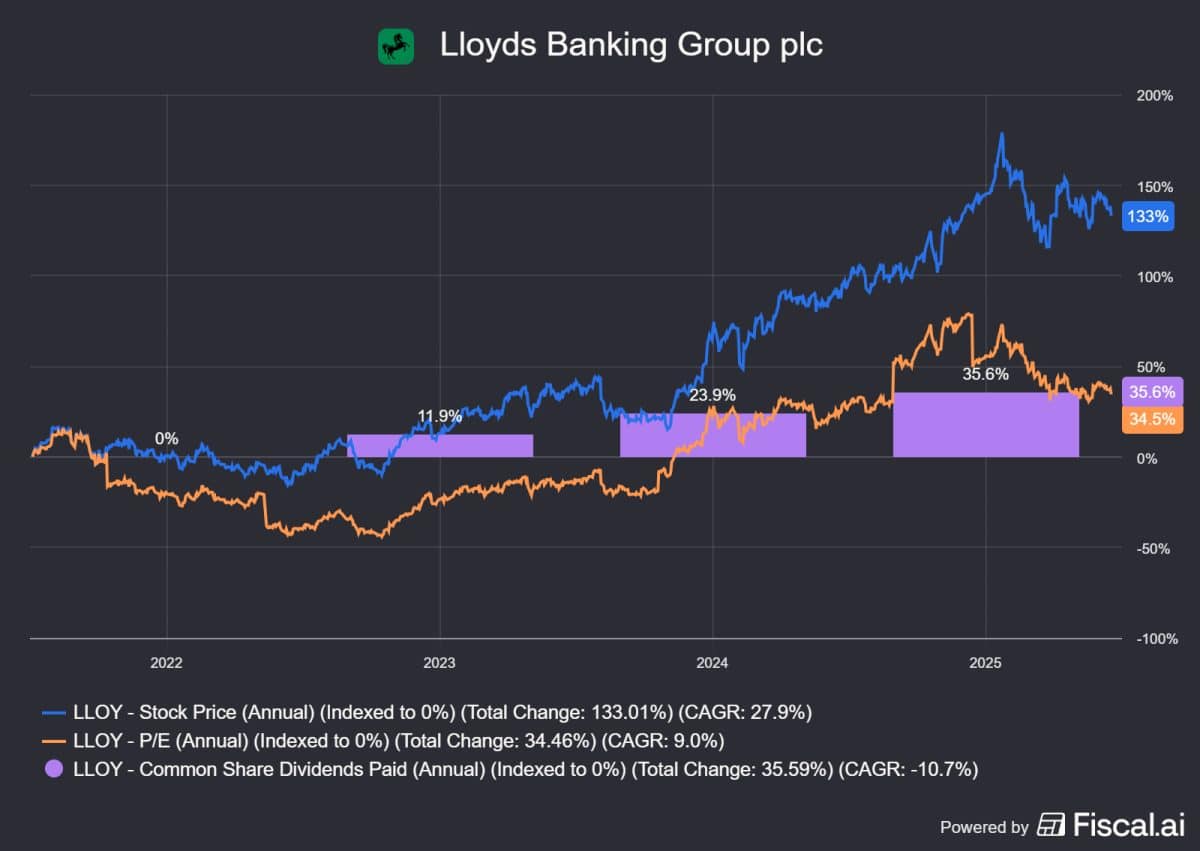

Rates have declined from 4.25% in May 2025 to 3.75% in early 2026, the lowest since late 2023.That’s why Lloyds hit multi-year highs in 2024 and 2025, with analysts upgrading the stock and pushing price targets into the mid‑80p range.

The bank remains the UK’s retail champion, with loans and advances growing 5% to £481.1bn in 2025. But here’s the question: will this optimism persist, or is it just a temporary burst from rising rates and resilient housing?

The hidden risk

Further rate cuts threaten Lloyds’ net interest margins. The bank also faces risk from UK property price weakness and higher unemployment pressuring borrowers. If house prices fall, risk-weighted assets rise and capital buffers tighten.

On top of this, Lloyds still faces serious risk from the motor finance scandal. The bank recently added £800m in charges, raising the total provision to £1.95bn. That scandal cost Lloyds £22bn in historical mis-selling, with the FCA estimating 44% of motor finance agreements since 2007 eligible for payouts.

Lloyds also decided not to challenge the FCA’s compensation scheme, which will pay 14 million unfair agreements with total lender payouts around £8.2bn.

What this means for investors

If you’re considering Lloyds as a stable income stock, you should factor in UK rates and housing. If the UK mortgage market stays resilient and rates don’t fall too fast, Lloyds could keep delivering.

If not, the stock could act more like a cyclical bet than a safe dividend.

Still, for income investors, it exhibits strong financials that make it worth a closer look:

- Share price: ~98.5p as of 8 June.

- Market-cap: £57.12bn.

- Price-to-earnings (P/E) ratio: 14.03.

- 2025 dividend: 3.33p per share (15% growth).

- Dividend yield: 3.25–3.39%.

Not a boring income stock

Lloyds is Britain’s closest stock market proxy for the UK mortgage cycle, which adds macro risk. Its share price is heavily tied to house prices, Bank of England policy, and credit quality.

But with a reliable 3.25%-3.4% dividend yield, its income potential can’t be ignored. That makes it worth considering for UK income investors who are optimistic about housing — with the caveat that it’s not a boring, risk-free income stock.

On the flip side, those feeling more jittery about housing might find more regulated income stability in a utility like National Grid or United Utilities.

Should you invest £5,000 in Lloyds Banking Group Plc right now?

When investing expert Mark Rogers and his team have a stock tip, it can pay to listen. After all, the flagship Twelfth Magpie Share Advisor newsletter he has run for nearly a decade has provided thousands of paying members with top stock recommendations from the UK and US markets.

And right now, Mark thinks there are 6 standout stocks that investors should consider buying. Want to see if Lloyds Banking Group Plc made the list?

Mark Hartley owns shares in Lloyds and National Grid.