Tax rules require REITs (real estate investment trusts) to return at least 90% of their rental income to shareholders each year. This means many of them offer above-average yields. But as a distribution of profit, there are no guarantees when it comes to dividends. After all, 90% of nothing is nil.

Here’s one REIT that’s currently paying an amazing 7.3%. Could this last? Let’s see.

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice. Readers are responsible for carrying out their own due diligence and for obtaining professional advice before making any investment decisions.

What does it do?

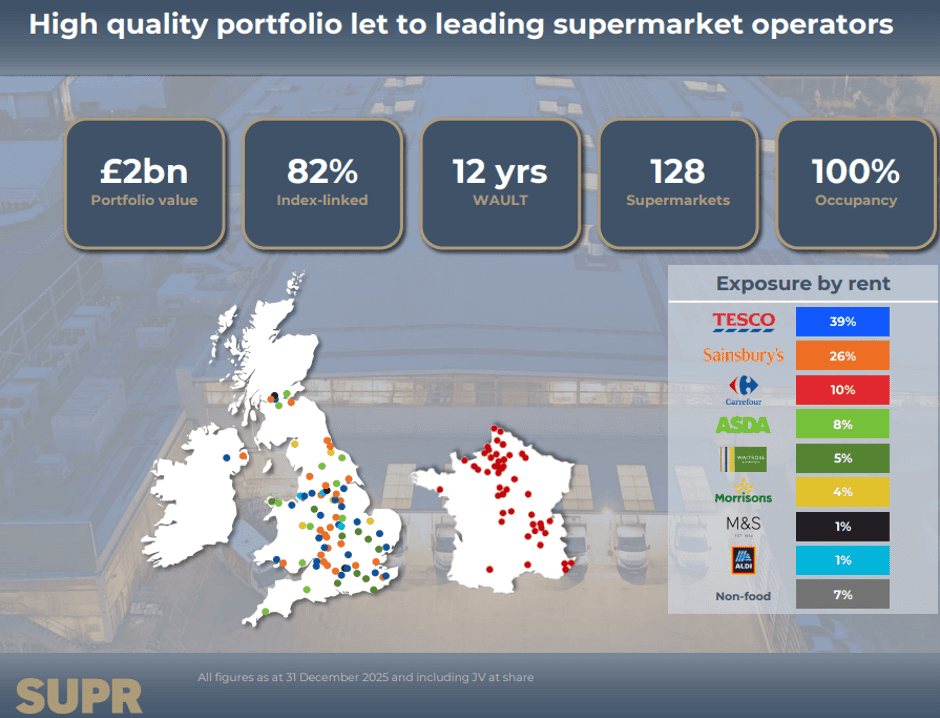

Supermarket Income REIT (LSE:SUPR) owns a £2bn portfolio of grocery stores, which it rents to blue-chip tenants.

From a financial perspective, its operations are easy to understand. It has one source of income, few overheads — despite having a market cap of £1.1bn, it employs less than 20 people – and relatively large borrowings.

As long as it successfully manages the ratio of rents to loan repayments, it should have some cash left over to return to shareholders.

Indeed, because a large proportion of its tenancies provide for inflation-linked rent increases (82%) and the cost of a significant amount of its debt is fixed or hedged (92%), it’s been able to steadily raise its dividend since listing in 2017.

The REIT paid its first dividend in October 2017. Since then, it’s returned a total of 51.65p a share. This is equal to just over half of its IPO price of 100p.

But this highlights a potential issue. The group’s share price is now (14 June) 85p. Shareholders have done well from the trust’s dividends but the loss of capital has, no doubt, been painful.

What’s the problem?

I suspect much of this loss of investor confidence relates to the higher interest rate environment that we’ve experienced since the pandemic.

In common with most REITs, Supermarket Income uses debt to help finance the purchase of its properties. Higher borrowing costs are bad for its bottom line.

At 31 March, its net debt was 8.2 times its EBITDA (earnings before interest, tax, depreciation, and amortisation) compared to a ratio of 5.1 nine months earlier. The trust expects it to be within a range of 7-8 times by March 2027.

Importantly, the REIT currently has a loan-to-value ratio of 43%, which is comfortably below the 60% limit specified by its debt covenants.

Higher interest rates also mean that investors with some spare cash may see an opportunity to earn a better return elsewhere, such as through less risky government bonds or deposit accounts.

My view

But I remain a fan of the REIT, particularly its dividend.

Based on amounts paid over the past 12 months, a £10,000 investment (11,765 shares) could produce £730 in dividends during the year ahead. Of course, there can never be any guarantees when it comes to payouts.

However, there are a number of factors that suggest it could be increased in coming years.

Positively, the average unexpired term of its rental agreements is 12 years. It enjoys a 100% occupancy rate and a 100% rent collection record. It also claims to have the second-lowest cost-to-income ratio of the FTSE 350’s REITs.

For those wanting to boost their passive income, I think Supermarket Income REIT is well worth considering. In fact, I have it in my own portfolio. But I’m not expecting its share price to go gangbusters. Investors wanting something a bit more exciting should probably look elsewhere.

Should you invest £5,000 in Supermarket Income REIT Plc right now?

When investing expert Mark Rogers and his team have a stock tip, it can pay to listen. After all, the flagship Twelfth Magpie Share Advisor newsletter he has run for nearly a decade has provided thousands of paying members with top stock recommendations from the UK and US markets.

And right now, Mark thinks there are 6 standout stocks that investors should consider buying. Want to see if Supermarket Income REIT Plc made the list?

James Beard owns shares in Supermarket Income REIT.