Aston Martin (LSE:AML) shares have taken a bigger beating than James Bond in a Soviet basement. Over five years, they’ve crashed by a shocking 98%!

Can this FTSE 250 stock make a recovery like the famous spy always does? Or is a Hollywood ending now a pipedream? Here are my thoughts.

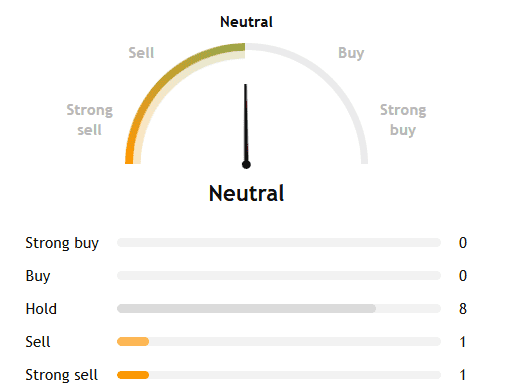

Here’s what the experts are saying

According to my data provider, there are 10 analysts following the stock. Of these, none rate it a Buy, while the overwhelming majority say Hold.

As for the average 12-month price target, however, it’s 46p. That’s 21.1% above where Aston Martin currently trades at.

Based on this then, a £5,000 investment made today could turn into just over £6,000 by June 2027 (ignoring trading commissions and trading spreads). A nice outcome, if achieved.

Naturally, it goes without saying that this is far from nailed on. There’s a reason the share price has nosedived 98%.

Why has Aston Martin crashed?

Unfortunately, Aston Martin’s time on the stock market has been marked by a recurring cycle of setting ambitious medium-term financial targets and subsequently not achieving them.

In 2020, the carmaker announced it was targeting around 10,000 vehicle sales, £2bn revenue, and £500m in adjusted EBITDA by 2024/25.

Then in 2023, the firm set a target for approximately £2.5bn in revenue and £800m in adjusted EBITDA, with a 30% margin, by 2027/28.

At the time, CEO Amedeo Felisa said: “We are on track to substantially achieve our 2024/25 financial targets in 2024 and, with continued strong momentum, are likely to exceed them in 2025.”

But last year, the company delivered 5,448 units (not 10,000), £1.26bn in revenue and adjusted EBITDA of £108m (not £2bn and £500m). To call that disappointing would be an understatement.

Looking ahead, there’s now a chance the original 2024/25 target won’t even be achieved by 2027/28.

Where are we now?

This is why I’m cautious about saying Aston Martin has turned a corner, despite encouraging signs in Q1. And there were some for sure, with 102 Valhalla deliveries helping push the gross margin into the mid-30s, from 27.9% the year before.

The pre-tax loss improved from £79.6m to £65.5m. And with the firm on track to deliver 500 Valhalla supercars for the full year, CEO Adrian Hallmark — the third chief executive inside five years! — is confident of “material financial improvement” in 2026.

Now, I’m a big fan of the supercar Valhalla, which has attracted rave reviews. But with production capped at 999 units, and more than 500 expected in the hands of buyers by the end of 2026, is the ‘sugar hit’ to revenue and margins sustainable?

What if the next exclusive high-priced model is a flop? And what if ultra-rich buyers in the Middle East reign in spending on new playthings due to the dodgy geopolitical backdrop?

Then there’s Aston Martin’s balance sheet, weighed down by £1.46bn in net debt. This obviously adds significant uncertainty and risk moving forward.

If the company’s Q1 momentum extended into Q2 (results due late July), the stock could get a quick shot in the arm. But the James Bond carmaker is far too risky for me, and I fear there will be no Hollywood ending here.

Should you invest £5,000 in Aston Martin Lagonda Global Plc right now?

When investing expert Mark Rogers and his team have a stock tip, it can pay to listen. After all, the flagship Twelfth Magpie Share Advisor newsletter he has run for nearly a decade has provided thousands of paying members with top stock recommendations from the UK and US markets.

And right now, Mark thinks there are 6 standout stocks that investors should consider buying. Want to see if Aston Martin Lagonda Global Plc made the list?

Ben McPoland has no position in any of the companies mentioned.