I think now might be the time to consider buying Netflix (NASDAQ: NFLX) shares. The stock’s fallen from a split-adjusted high of $133.91 to around $77.

That’s a decline of around 43%. But by almost every operating metric, the underlying business is doing pretty well.

What’s been going wrong?

The sell-off has several ingredients. One is the firm’s Q2 earnings report – specifically, the forward guidance.

Netflix guided for $12.57bn in revenue, which was below the anticipated $12.63bn. And co-founder Reed Hastings announced his intention to stand down in June.

Neither development’s trivial, but neither’s catastrophic. The revenue miss is small and Hastings is leaving to pursue philanthropy – not because the business is broken.

Analysts at Bank of America downgraded the stock to Hold earlier this month. Jefferies also cut its price target to $110 from $128, adding to the negative sentiment. As a result, the stock’s been trading lower.

But it was expensive before, so has it reached bargain territory?

Valuation reset

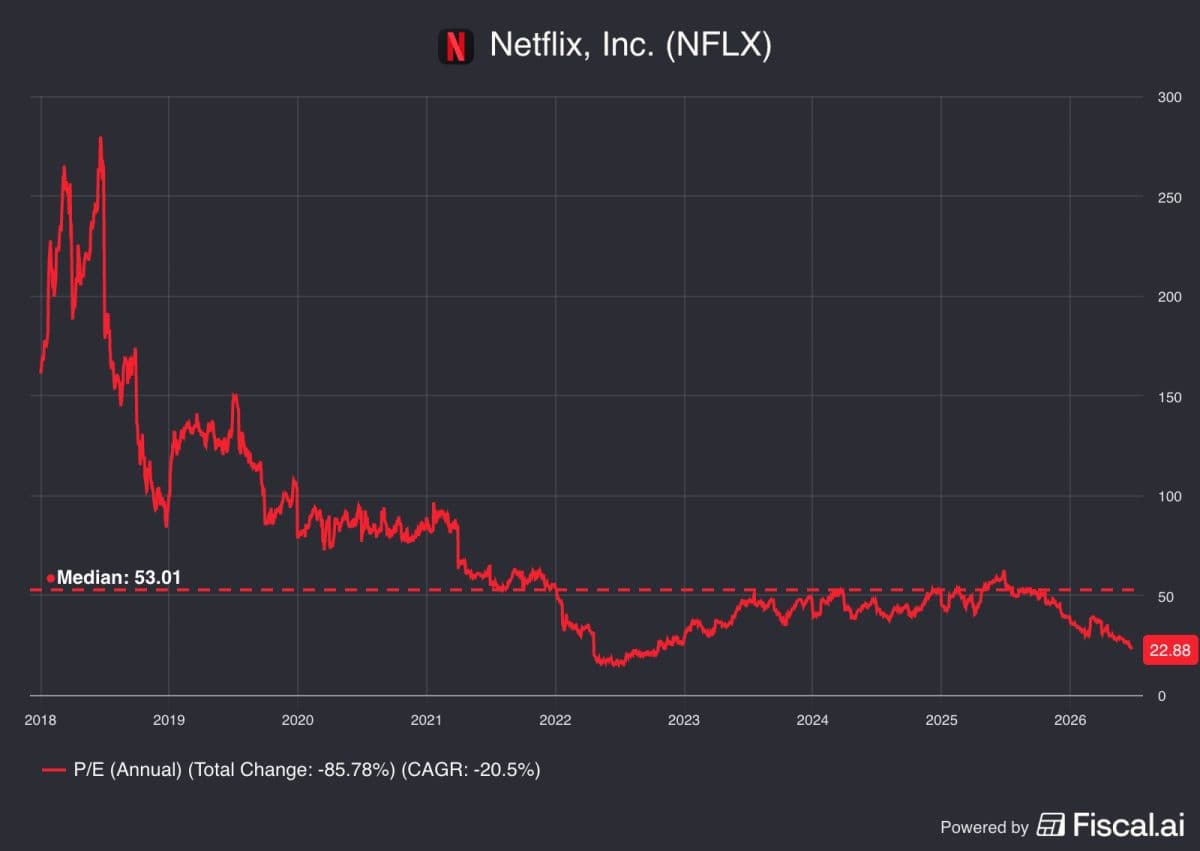

Here’s what diligent investors should actually be paying attention to. Netflix’s trailing price-to-earnings (P/E) ratio’s around 23. The 10-year average is closer to 41.

Source: Fiscal.ai

In 2022 – when markets wrote the stock off as subscriber numbers faltered – the multiple only reached 15. It’s not quite at that level, but 23 is nearer 15 than 41.

The outlook for growth’s also pretty positive. Analysts at Morgan Stanley expect earnings and free cash flows to grow at around 20% a year.

That puts the price/earnings-to-growth PEG ratio at close to 1, which isn’t particularly high for any business. And it’s definitely not high in the case of Netflix.

The company still has some unique strengths that identify it as a high-quality operation. That’s why I think the stock’s worth checking out at today’s prices.

Advertising

The big challenge for Netflix is competition. It isn’t just up against cable subscriptions these days – it has the likes of Amazon and Apple for company. These operations obviously have deep pockets and huge capacity to invest. And that’s a real danger for a firm that isn’t backed by a tech giant.

Importantly, Netflix’s advertising business is arriving faster than investors seem to think. It now reaches 250m monthly viewers and advertiser numbers are up 70% in a year. Management expects advertising revenue to reach $3bn in 2026. And this is expected to push free cash flows to $12.5bn.

It’s a tough industry. But Netflix is finding a way to support $30bn in share buybacks and I think that’s clearly a sign of long-term strength.

Worth considering

Netflix isn’t a washed-out stock. The possibility of more selling after the firm’s Q2 results next month is real, as is the governance transition.

At today’s price however, investors are paying a mature-media multiple for a business that’s still generating 16% revenue growth. That seems like a deal worth considering.

Should you invest £5,000 in Netflix right now?

When investing expert Mark Rogers and his team have a stock tip, it can pay to listen. After all, the flagship Twelfth Magpie Share Advisor newsletter he has run for nearly a decade has provided thousands of paying members with top stock recommendations from the UK and US markets.

And right now, Mark thinks there are 6 standout stocks that investors should consider buying. Want to see if Netflix made the list?

Stephen Wright owns shares in Amazon, Apple, and Netflix.