The collapse in the Lloyds (LSE:LLOY) share price this year is unwarranted in my view. I believe this partially because the fall engendered by the Silicon Valley Bank fiasco was overplayed, but also because the worst-case scenario was never that likely.

Here’s why I’m expecting the stock to push back towards 60p.

Downside scary but unlikely

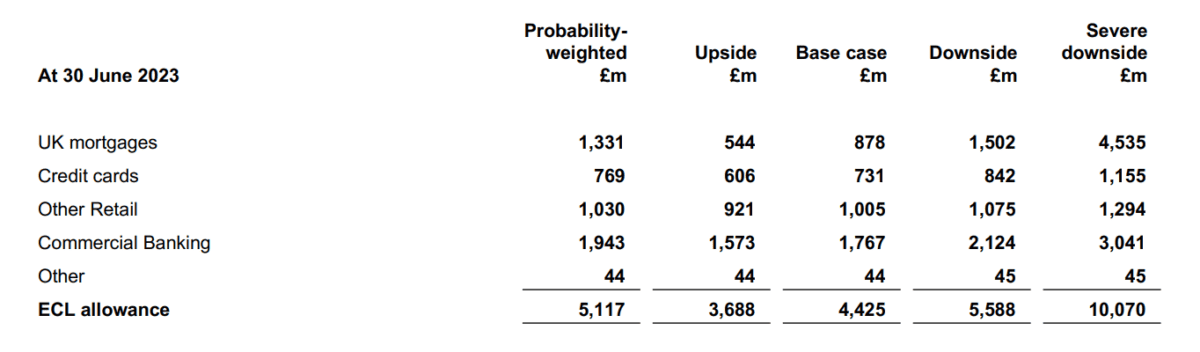

If we scroll to page 101 of the Lloyds H1 report, we’ll find the bank’s forecasts for expected credit losses (ECLs). The first thing that becomes clear is that there is a huge discrepancy between the best and worst-case scenarios.

As we can see, under its severe downside scenario, the bank anticipates that ECL would amount to £10.1bn. That’s a huge figure, amounting to around 35% of Lloyds’s current market cap.

As of 30 June, the severe downside scenario was likely to be twice as destructive as the probability-weighted (most likely at the time) scenario. Interestingly, the probability-weighted scenario was already weighted to the negative side of the base case, with the bank expecting further pain.

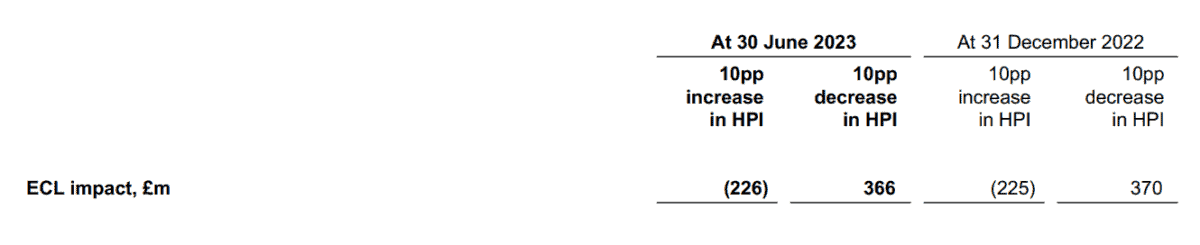

At the end of the quarter, 30 June, interest rates stood at 5%. This figure is already considered far above the optimal level for banks, as higher interest rates could engender a slew of defaults.

At the time, Lloyds highlighted that a further 10 basis point hike would result in a £226m increase in ECL. Meanwhile a reduction by 10 basis points would likely see ECL increase by £366m.

This happens because higher interest rates increase borrowing costs for borrowers, potentially leading to more loan defaults and credit losses.

Moreover, higher interest rates raise the discount rate used to estimate the present value of expected future cash flows from loans and financial assets, reducing their current value and potentially inflating ECL calculations.

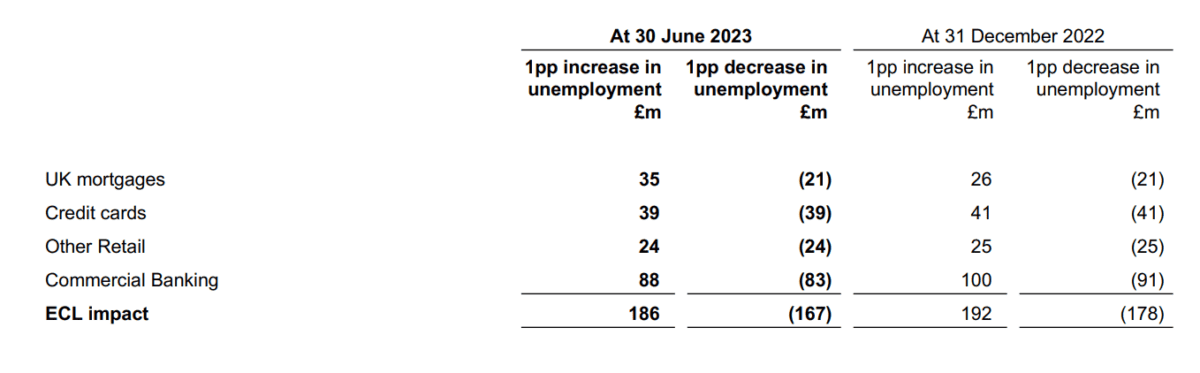

It’s also worth highlighting that Lloyds sees a tighter labour marketing adding to ECL issues.

Outlook full of positives

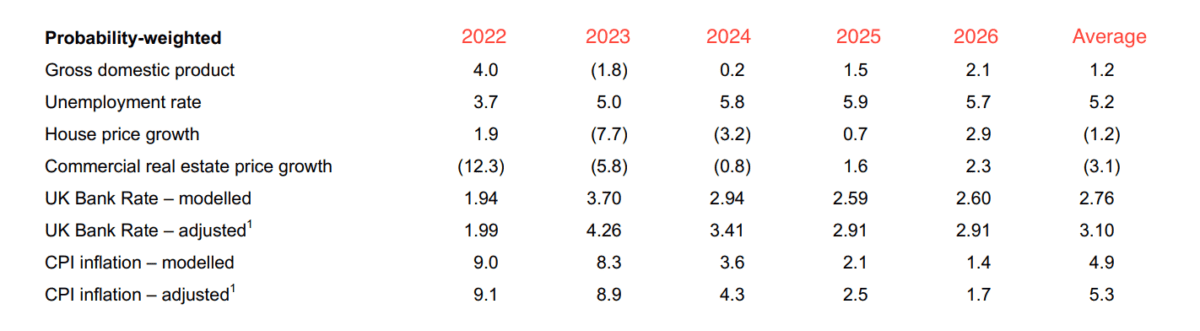

While the severe downside scenario was only an outside risk, it now appears even less likely. This is because inflation is continuing to fall. In fact, on 20 September, inflation came in even lower than expected, raising expectations for the Bank of England to slow or stop its monetary tightening.

Under the bank’s own probability-weighted scenario, we can see inflation and interest rates falling throughout the medium term. Interest rates may bottom out around 2.59%, according to the bank’s analysts.

To me, with the exception of the slow GDP growth, this forecast looks highly positive. Because when interest rates are between 2% and 3%, it’s optimal for banks. In this zone, impairment charges will likely fall from where they are today while net interest margins will remain elevated.

Moreover, because of its lack of an investment arm, and increased interest rate sensitivity, Lloyds should benefit more clearly from falling interest rates than its peers.

So, trading at just 0.7 times book value and 5.9 times earnings, Lloyds looks like a real steal. That’s why I’ve been topping up my position.