Rolls-Royce (LSE:RR) shares have been the FTSE 100 comeback story of the last five years. But what will the next 12 months bring?

It feels like a lot is going the company’s way at the moment. Analysts, however, are still pretty bullish about the share price.

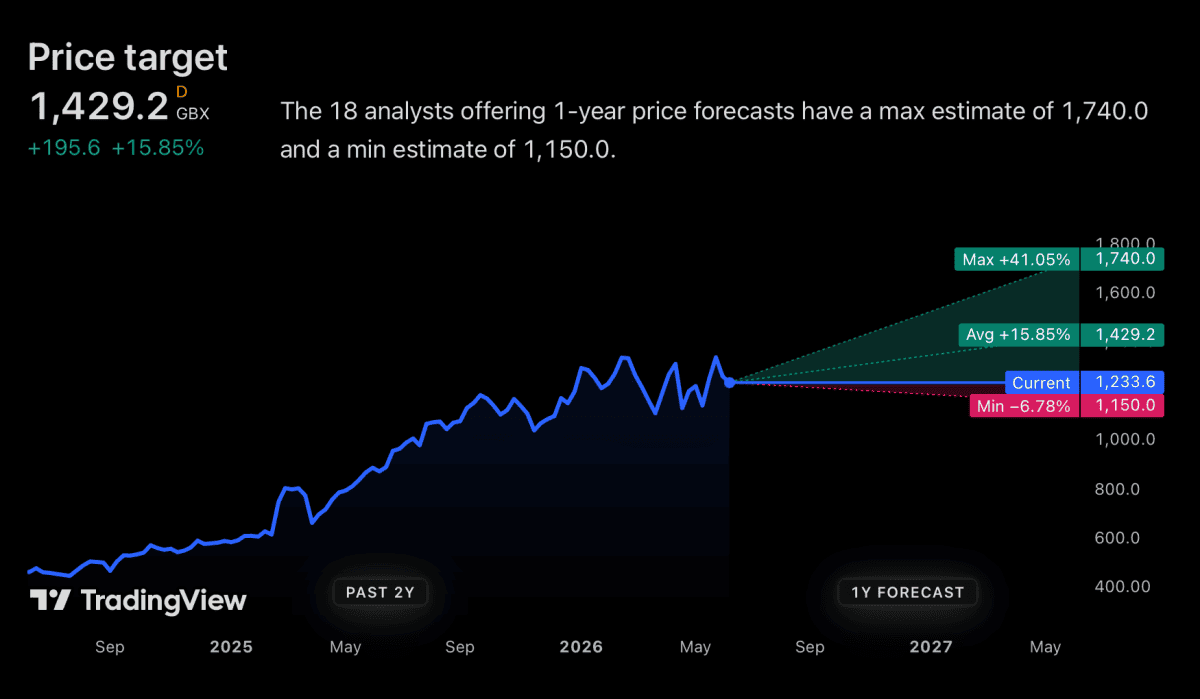

What are analysts saying?

The current consensus among analysts points to a median target price of 1,429p. That’s 15.85% above the current 1,233p share price.

Source: TradingView

The low estimate is 1,150p and the high target is 1,740p. In other words, the institutional community is pretty positive about the stock.

This isn’t entirely baseless. There are a lot of reasons to be positive about the outlook for Rolls-Royce, including the following:

- Large Engine Flying Hours (EFHs) — the metric that dictates Rolls-Royce’s lucrative long-term service contracts — have fully recovered to pre-pandemic levels.

- Defence contracts — including the AUKUS submarine programme — are creating significant revenue backlogs.

- Data centres are exploring local power generation possibilities, including small modular reactors (SMRs).

All of these are significant considerations. But how far are they already reflected in the current share price?

What could go wrong?

The stock trades at a price-to-earnings (P/E) ratio of 35.5 based on next year’s estimates. By FTSE 100 standards, that isn’t cheap.

The danger with this is that it doesn’t leave a lot of room for anything to go wrong. And there are real risks to pay attention to.

The biggest risk is technical. A systematic engine recall can result in billions in lost revenues and compensation costs.

That’s happened to Pratt & Whitney recently. But Rolls-Royce itself had problems with its Trent 1000 engines just before Covid-19.

For investors, it’s worth noting that the share price doesn’t leave much margin for error.

Could they be too pessimistic?

Rolls-Royce shares are up 1,012% in the last five years. But that doesn’t mean they can’t go further if things go the company’s way.

Commercial aviation is facing aircraft shortages. That means more use of existing fleets – and more servicing revenues for engine manufacturers.

Sadly, ongoing military conflicts also boost the firm’s defence division. What happens next is anyone’s guess, but continued tension is hard to rule out.

There’s a real possibility of higher SMR demand from data centres. Power is a big constraint and local generation might be the answer.

All of these could push the stock up from its current levels. If things go right, I think it could even go above 1,740p by this time next year.

Buy, sell, or hold?

At a P/E ratio of 35.5, buying Rolls-Royce today is no longer about a distressed recovery. It’s a bet on long-term operational excellence.

That’s not out of the question, by any means. The business is in its best shape in a decade and analysts are still bullish.

Things, however, can turn around quickly in this industry. And I’m not convinced today’s share price offers much protection if they do.

Rolls-Royce shares might continue to outperform. But I’m focusing on opportunities that I think offer a better risk-reward profile.

Should you invest £5,000 in Rolls-Royce Plc right now?

When investing expert Mark Rogers and his team have a stock tip, it can pay to listen. After all, the flagship Twelfth Magpie Share Advisor newsletter he has run for nearly a decade has provided thousands of paying members with top stock recommendations from the UK and US markets.

And right now, Mark thinks there are 6 standout stocks that investors should consider buying. Want to see if Rolls-Royce Plc made the list?

Stephen Wright does not own shares in any of the companies mentioned.