The wait is over. SpaceX (NASDAQ:SPCX) stock begins trading on the Nasdaq today (12 June) in probably the most hotly anticipated IPO ever.

Even if you’re tired of the hype, the numbers involved are hard to ignore. Around $75bn has been raised by the rocket and satellite company at a colossal valuation of $1.77trn.

For context, that’s more than the combined market value of HSBC, AstraZeneca, Shell, Rolls-Royce, Unilever, BP, BAE Systems, NatWest, Diageo, Tesco, Vodafone, and BT. And you’d still have space to cram in another couple of Rolls-Royces!

Thinking about buying SpaceX shares? Here’s what you should know first.

Starlink is the breadwinner

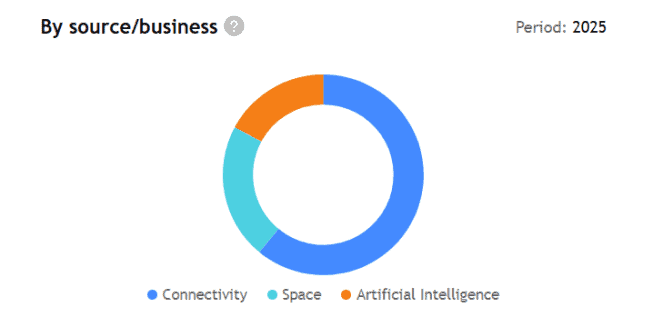

SpaceX started off as a maker of rockets. And while they naturally attract most of the media coverage — especially when they explode spectacularly — it’s Starlink that has stealthily become the group’s main breadwinner.

This is the communications network with nearly 10,000 satellites in orbit. Last year, this division (called Connectivity) was the only profitable one (of three), generating a $4.4bn operating profit on revenue of $11.4bn.

That accounted for around 61% of total group revenue.

Starlink recently surpassed 12m active users, up from 9m last year, and is operating in more than 160 countries and territories. SpaceX generates around 20% of revenue from the US government.

Via its own rockets (including potentially the gigantic Starship), the firm intends to put over 100,000 satellites into orbit. These will be next-generation V3 versions, which are 10 to 20 times more powerful than existing satellites.

Reported losses are ongoing

In 2025, the firm’s revenue jumped 33% to $18.7bn. However, its AI unit (formerly xAI) is spending aggressively to build out computing infrastructure, resulting in a $4.9bn net loss last year.

That said, if you strip out the AI bit, SpaceX has been generating positive cash flow for a decade or so. But it’s important to know that analysts aren’t expecting the firm to turn profitable again for at least another couple of years due to heavy AI spend.

Longer term, these investments could pay off big time in the shape of data centres in space (where electricity and cooling are theoretically both free). But there are a lot of technical challenges that make this outcome uncertain.

The valuation is astronomical

Perhaps the most important thing to bear in mind is the company’s implied valuation. Based on last year’s revenue, the price to-sales (P/S) ratio will be around 94. Potentially well over 120 if the stock pops later!

Given that anything above 10 is usually considered pricey, this adds a lot of valuation risk. If SpaceX can’t live up to lofty growth expectations, then the share price will probably end up tanking.

How fast do analysts expect the firm to grow revenue? Rapidly, as we can see by the declining forward-looking multiples below.

| Enterprise value-to-sales ratio | |

| 2026 | 51.9 |

| 2027 | 26.5 |

Weighing everything up though, I think the risks outweigh the rewards at a $1.77trn valuation. So I’m just keeping SpaceX on my watchlist for now.

Should you invest £5,000 in Space Exploration Technologies Corp. - Class A right now?

When investing expert Mark Rogers and his team have a stock tip, it can pay to listen. After all, the flagship Twelfth Magpie Share Advisor newsletter he has run for nearly a decade has provided thousands of paying members with top stock recommendations from the UK and US markets.

And right now, Mark thinks there are 6 standout stocks that investors should consider buying. Want to see if Space Exploration Technologies Corp. - Class A made the list?

Ben McPoland owns shares in AstraZeneca, BAE Systems, Diageo, HSBC, and Rolls-Royce.