Scottish Mortgage Investment Trust (LSE:SMT) has done fantastically well in the FTSE 100 over the past couple of years. Since late 2023, the growth trust’s share price has more than doubled.

Much of this has been driven by the incredible success of Space Exploration Technologies, which it first invested in back in 2018. That stake has ballooned in value.

However, Scottish Mortgage is currently in a strange period. While it’s sitting on massive unrealised profits, it can’t offload any SpaceX shares until the rocket/satellite firm reports its Q2 results, sometime in August.

At that point, only 20% can be sold, rising to 30% if SpaceX stock is 30% above its IPO price. But that’s not guranteed because it’s currently only just above its IPO price of $135.

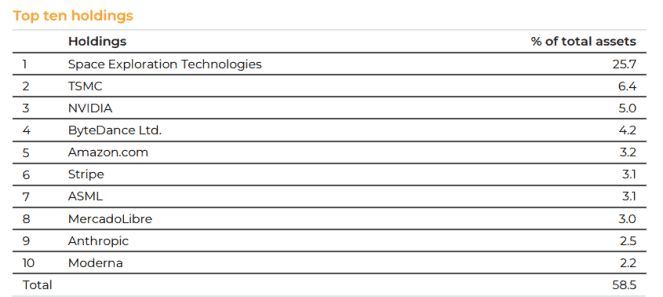

For better or worse then, Scottish Mortgage’s day-to-day share price performance is currently tied to what happens with SpaceX. And at the end of June, Elon Musk’s firm made up a whopping 25.7% of assets!

Should Scottish Mortgage investors be worried?

Holding at scale

For me, the answer depends on how large a weighting SpaceX is by mid-December. Then, the investment trust will be able to sell the entire position if it chooses to.

However, reading manager Tom Slater’s latest commentary on SpaceX’s monopolistic position and commercial opportunities makes it clear that SpaceX will likely remain a top holding.

SpaceX is…a dual monopoly in launch and global connectivity, with Starlink building highly profitable, recurring revenue that the best software businesses aspire to, except that its assets are in orbit and extraordinarily difficult to replicate…If Starship achieves full reusability, the economics of placing AI infrastructure in orbit become compelling. And that’s why we hold it at scale.

Tom Slater, July 2026.

Fair enough. But surely holding SpaceX “at scale” won’t involve it being over 20% of total assets, though?

If so, then I think there’s a lot of concentration risk because SpaceX’s valuation looks too high to me. At a market cap of $1.8trn, it’s trading at around 47 times this year’s forecast sales. No profits are expected until 2028 due to heavy AI capex.

Speaking as a Scottish Mortgage shareholder, I would like to see SpaceX reduced to 4%–8% of the portfolio (in line with TSMC and Nvidia). At this type of weighting, it can still drive meaningful returns if successful, while the damage is limited if its valuation fails to live up to expectations.

Beyond SpaceX

While SpaceX hogs all the headlines, it’s important to remember that the rest of the portfolio’s progressing well. Holdings MercadoLibre, Nu, Revolut, and Stripe are growing rapidly as they build the infrastructure of digital finance.

Anthropic’s annualised revenue run rate has gone from $1bn at the start of 2025 to more than $47bn today. And TSMC, SK Hynix, Nvidia and ASML are all at the very epicentre of the AI infrastructure buildout.

Meanwhile, Cloudflare is helping websites identify and charge AI agents for access to their content. In Q1, CEO Matthew Prince said that AI is “shaping up to be the biggest tailwind we’ve ever seen in Cloudflare’s history“.

Scottish Mortgage is trading at a 7% discount to net asset value. If the stock keep falling, I think it’s worth considering on the dip, then holding long term.

Should you invest £5,000 in Scottish Mortgage Investment Trust Plc right now?

When investing expert Mark Rogers and his team have a stock tip, it can pay to listen. After all, the flagship Twelfth Magpie Share Advisor newsletter he has run for nearly a decade has provided thousands of paying members with top stock recommendations from the UK and US markets.

And right now, Mark thinks there are 6 standout stocks that investors should consider buying. Want to see if Scottish Mortgage Investment Trust Plc made the list?

Ben McPoland owns shares in Cloudflare, MercadoLibre, Nu Holdings, Nvidia, Scottish Mortgage, and TSMC.