Using a Self-Invested Personal Pension (SIPP) is one of the most powerful ways to build wealth for retirement. Investments can grow faster, free from the eroding effect of capital gains and dividend taxes. What’s more, every contribution you make benefits from tax relief, giving your pension pot a cash boost.

So let’s say you’re targeting a £3,000 retirement income from your SIPP to combine with the State Pension. How much do you need to invest?

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice. Readers are responsible for carrying out their own due diligence and for obtaining professional advice before making any investment decisions.

Building a SIPP strategy

There’s a number of ways to turn a retirement portfolio into a steady income. One is to draw down a set percentage each year (typically 4%). Another is to use all or part of your savings to purchase an income-generating annuity policy.

My plan — and the one we’ll be using in this example — is to invest my SIPP pot into dividend-paying shares. The reason? Well there are several, including:

- Regular income without needing to sell shares.

- The potential for income growth as companies raise dividends.

- An opportunity for further capital growth alongside passive income.

There are some key rules to follow with this strategy, however. Dividends are never guaranteed. So I’ll need a large and diverse selection of income-paying stocks for a reliable cash stream. I’ll also need a decent number of high-yielding stocks, while making sure to avoid classic ‘traps’ whose yields are unsustainable over time.

Investing £197 a month

With our strategy sorted, we can now ask: how large must my SIPP be for a £3,000 monthly income?

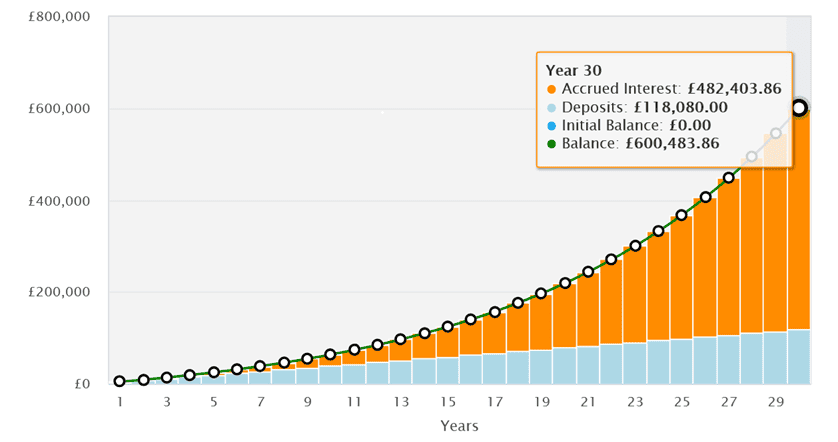

If I invest in 6%-yielding dividend shares, I’ll need a nest egg of £600,000. That’s a big number. But it’s one that everyday investors can realistically aim for with patience and commitment.

Let’s say you’re a higher-rate taxpayer, and enjoy 40% tax relief on any SIPP investments. That would bump a £197 individual contribution each month up to £328. With this, you could reach that magic target after 30 years, based on an average 9% annual stock market return.

Is 30 years too long?

But what about if you want to retire earlier, or don’t have 30 years until your planned retirement date? One way of accelerating SIPP wealth creation is to identify companies capable of outperforming the wider market.

Take Softcat (LSE:SCT) as an example to consider. Its shares have rocketed 552% in value over the last decade. With dividends combined, the total average annual return for the period is 21.7%.

At this rate, a total £328 contribution each month (including tax relief) would build a £600,000 SIPP after just 15 years and 4 months.

Softcat is a UK tech star providing cybersecurity, cloud computing, and other IT services. Its shares have surged in value as businesses steadily digitalise their operations. Can it continue thriving, though, as companies turn more to artificial intelligence? I think it can, helped by its own investments in AI (latest half-year financials showed sales and operating profit up 54% and 16% year on year).

I actually hold Softcat shares in my own SIPP. It’s one of many top UK shares investors today can target for long-term wealth.

Should you invest £5,000 in Softcat Plc right now?

When investing expert Mark Rogers and his team have a stock tip, it can pay to listen. After all, the flagship Twelfth Magpie Share Advisor newsletter he has run for nearly a decade has provided thousands of paying members with top stock recommendations from the UK and US markets.

And right now, Mark thinks there are 6 standout stocks that investors should consider buying. Want to see if Softcat Plc made the list?

Royston Wild owns shares in Softcat.