Greggs’ (LSE: GRG) shares have been stuck below 1,800p for over a year now. That’s left many investors, including me, wondering if there’s any hope of recovery. Should we keep holding on – or is it time to sell and chase better opportunities elsewhere?

To answer that question, I need to figure out if this is a temporary hiccup or a more fundamental problem. So I’ve been digging into the latest results and analyst views to get a clearer picture.

Let’s see if we can identify where exactly things went wrong for one of the UK’s most beloved bakers.

What’s behind the weak performance?

The most simple way to look at this is that Greggs is feeling the squeeze from the cost-of-living crisis. Households have been tightening their belts, which has hurt like‑for‑like sales growth and product mix.

Even though total sales grew 6.8% to £2.15bn in 2025, pretax profit fell 18% to £167.4m, with underlying operating margins dropping from 9.7% to 8.7%.

Rising wages, energy and input costs have compounded the problem, narrowing margins even as sales have grown. As profit growth slowed and then turned negative, the valuation premium that Greggs once enjoyed collapsed. The shares now trade close to five‑year lows.

What’s more, Greggs has become one of the most shorted UK stocks, reflecting deep scepticism about a near‑term earnings recovery. Management has said any profit improvement in 2026 is “contingent on a recovery in the consumer backdrop“, tying the stock’s fate closely to the wider UK economy.

But if the economy does turn, could Greggs bounce back strongly?

The (tentative) bull case

There are some encouraging signs. Early 2026 trading showed better like‑for‑like sales versus the prior year, and full‑year guidance was maintained rather than cut.

Capital expenditure is expected to fall from £287.5m in 2025 to about £200m in 2026, and then £150m-£170m from 2027, freeing up cash for further store expansion. Plus, the 4.3% yield adds income appeal.

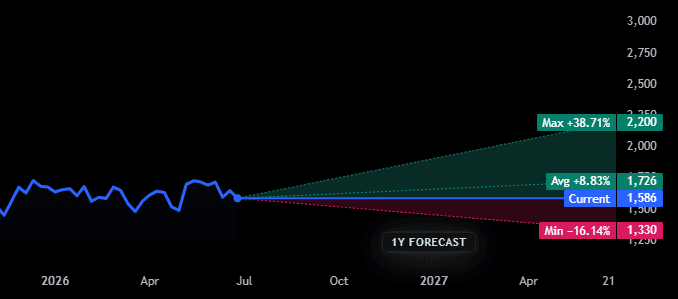

The shares also look cheap on paper. They trade on roughly 13 times forward earnings for 2026, well below Greggs’ 10‑year average. Analyst price targets average around 1,850p, with a range from 1,330p-2,200p, implying moderate growth potential if the recovery takes hold.

But here’s the catch: any recovery remains tightly linked to the UK consumer. If the cost‑of‑living crisis persists, it’s unlikely we’ll see meaningful improvement in Greggs’ short-term earnings.

So is this a stock to hold or fold?

My take

For patient shareholders like me, there’s a chance of positive returns over the next 3-4 years if consumer confidence recovers. The struggling high street baker might still surprise us all, but the bull case is weakening by the day.

Realistically, it’s becoming harder to see a compelling opportunity for new investors in the current environment. The risks look elevated, and the growth story is no longer what it once was.

The real question is, how much longer are you willing to wait for Greggs to enact a meaningful turnaround?

For those chasing shorter‑term growth, I think the capital could be used to target better returns elsewhere. But for patient value investors happy with moderate income, it’s still worth a look.

What income stock do we like better than Greggs Plc right now?

One of our Share Advisor analysts has just released a brand new stock report that we think is a must-read for any investor looking to try and generate potential income.

And the best bit is that you can see if for yourself, right now, absolutely free of charge!

No jargon. No hard sell. Just a clear look at an income share we think is worth your time.

Mark Hartley owns shares in Greggs.