When hunting for shares to buy, the moment everyone else loses interest is usually the time to start paying attention. And that’s definitely the case with oil stocks.

The Kushner-Witkoff talks in Qatar have reopened the Strait of Hormuz, put Iranian barrels back on the water, and knocked 20% off BP’s share price. So is it time to take a look?

Is the oil chart telling us to be bullish?

Some analysts now see Brent heading for $55. But Jeff Currie — who made his name calling commodity supercycles at Goldman Sachs and is now at The Carlyle Group — takes the opposite view.

Currie argues we’re in the early stages of a supercycle that could run another decade. The main cause is chronic underinvestment in production colliding with the buildout of power-intensive AI infrastructure.

He calls energy “the biggest asymmetric trade in modern finance”, noting oil majors generate free cash flow yields around 15.5% while the hyperscalers spending hundreds of billions generate none. And he has a point.

The data centre angle matters more than most realise. AI infrastructure’s brutally power-intensive — it needs gas, grid capacity, and cooling, all areas where integrated majors like BP are already embedded.

In Currie’s words, the electrification story is “far stronger than we ever dreamed of in 2020”. If he’s right, the direction for oil prices over time might be higher, not lower.

A FTSE 100 oil stock

BP (LSE:BP) has had an unimpressive record in recent years. But Meg O’Neill took over as CEO on 1 April, arriving from Woodside Energy, which she built into Australia’s largest listed energy company.

Her playbook there — ruthless focus on core upstream competences, LNG strength, and capital discipline — is exactly what BP needs after years of strategic wandering. Despite this, the stock’s some way off its highs.

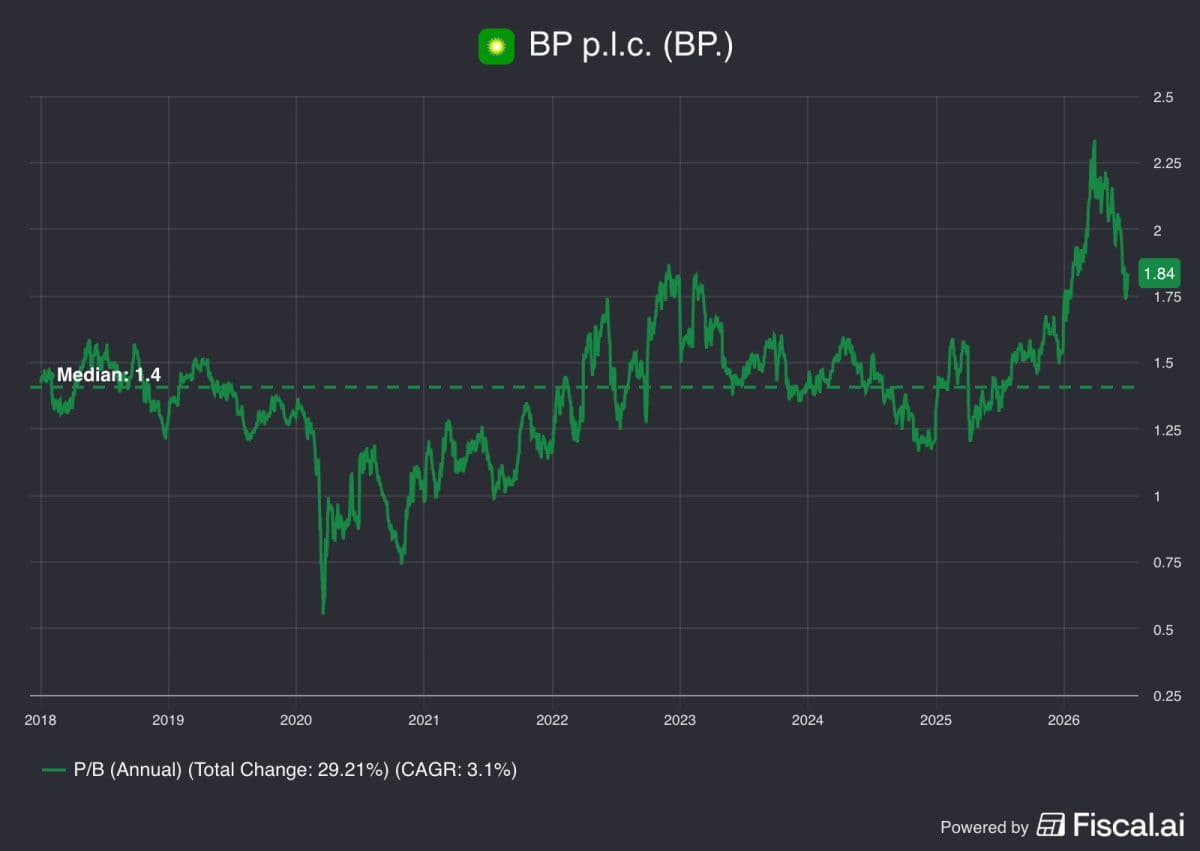

The price-to-book (P/B) ratio of roughly 1.8 is slightly above the 10-year average of 1.4. So the stock isn’t exactly in deep value territory.

Source: Fiscal.ai

It is however, a far less demanding multiple than April’s 2.3. And the trailing 5.4% dividend yield makes it one of the highest in the FTSE 100.

In short, the company has a potential opportunity ahead, the right long-term strategy, and a valuation that looks reasonable, if not depressed. I think that means it’s worth a look.

What could go wrong?

Iranian supply could yet push crude oil prices lower and that makes a real difference for BP. The firm reckons a $1 shift in Brent prices translates into a $340m movement in pre-tax operating profits.

Windfall taxes are another potential issue. Westminster might be in transition, but that uncertainty shouldn’t be confused with a sign that trading conditions are about to get easier.

Nonetheless, BP has a credible CEO, structural demand from data centres, and Currie’s supercycle thesis in the background. As a result, I think BP shares look attractive to consider today with Brent at $71 than they did at $124.

For long-term investors, the time to think about buying stocks is when others lose interest. At least with oil companies, there are very obvious signs when this happens.

Should you invest £5,000 in Bp P.l.c. right now?

When investing expert Mark Rogers and his team have a stock tip, it can pay to listen. After all, the flagship Twelfth Magpie Share Advisor newsletter he has run for nearly a decade has provided thousands of paying members with top stock recommendations from the UK and US markets.

And right now, Mark thinks there are 6 standout stocks that investors should consider buying. Want to see if Bp P.l.c. made the list?

Stephen Wright does not own shares in any of the companies mentioned.