Having fallen 30% since June 2025, Taylor Wimpey (LSE:TW.) shares are now (1 July) offering one of the highest yields on the FTSE 250.

Could this be an amazing opportunity, or a bit of a value trap? Let’s explore.

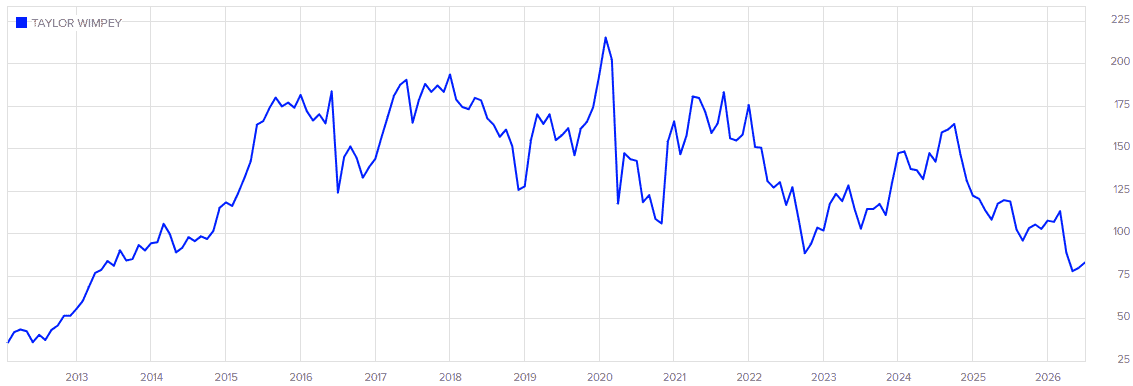

Buyer beware

The first thing to note is that high yields are often a warning sign of potential trouble. Investors sometimes demand a premium for holding the stock of a company that, they believe, is likely to face a difficult period ahead. And if their fears are realised, its payout could be cut.

That’s probably why Taylor Wimpey’s offered an above-average yield since the pandemic. Higher interest rates and rising construction costs have impacted the demand for mortgages and squeezed the group’s margin. This double whammy has made investors cautious and badly affected the group’s share price.

As the chart of month-end share prices shows, it was last regularly trading below 80p over 12 years ago.

Despite these woes, the group’s maintained a generous dividend for the past five financial years:

- 2021 – 8.58p

- 2022 – 9.40p

- 2023 – 9.58p

- 2024 – 9.46p

- 2025 – 7.62p

What’s happening now?

However, to prove my point about high yields being a possible warning indicator, the group’s payout was cut by 19.5% in 2025. Even so, the stock’s still yielding 9.3%, putting it in the top 10 of FTSE 250 dividend payers.

The fact that the stock’s yield remains high could be a sign that investors are anticipating another cut. Of course, this can’t be ruled out. Indeed, a look at the company’s new distribution policy commits to returning 5% of net assets to shareholders each year by way of dividend, with a further 2.5% through another payout or share buybacks.

The group’s December 2025 balance sheet shows net assets of £4.187bn. Based on the current number of shares in issue, it means the 2026 dividend could be 6p-9p a share (5%-7.5% of net assets).

Management teams tend to prefer share buybacks as their bonuses are often paid on the basis of increasing earnings per share. However, in theory, shareholders should benefit whichever policy is followed.

Even if the dividend was cut to 6p, the stock would still yield 7.3%. There are only 21 on the FTSE 250 offering more.

So does this mean Taylor Wimpey’s shares are dirt cheap?

My view

I wouldn’t go that far. There are still plenty of challenges for the housebuilder to overcome. We don’t know how the Iran war is going to affect inflation in the medium-term. Also, the domestic economy – and housing market — is a little shaky at the moment.

But although I don’t consider it to be dirt-cheap, I still think Taylor Wimpey’s a stock to consider, and not just because of its dividend. The UK housing shortage means the demand for new properties should pick up when consumer confidence returns. And the government’s planning reforms should make it easier to build.

At the moment, the group has plenty of land (76,000 plots) on its books. And it has an order book worth £2.23bn (7,689 homes). Encouragingly, there’s very little debt on its balance sheet.

I already have exposure to the sector through a shareholding in Persimmon. If I didn’t, I would seriously think about Taylor Wimpey as an alternative.

Should you invest £5,000 in Taylor Wimpey Plc right now?

When investing expert Mark Rogers and his team have a stock tip, it can pay to listen. After all, the flagship Twelfth Magpie Share Advisor newsletter he has run for nearly a decade has provided thousands of paying members with top stock recommendations from the UK and US markets.

And right now, Mark thinks there are 6 standout stocks that investors should consider buying. Want to see if Taylor Wimpey Plc made the list?

James Beard owns shares in Persimmon plc.