BP (LSE:BP.) shares are now changing hands for around 20% less than their 52-week high. With the Strait of Hormuz reopening following an agreed ceasefire, talks between the US and Iran ongoing, and the price of oil sinking, this shouldn’t come as a surprise.

But does this now present an amazing buying opportunity to consider? Let’s see.

Confession time

I acknowledge that investing in the sector might not appeal to everyone, but I used to own BP shares. In fact, I sold them midway through the Iran war. Now, I’d like to claim that I got rid of them when the group’s share price was close to its 12-month peak, but I didn’t. However, I was content with my profit, having bought them for 362p a year earlier.

But readers of The Twelfth Magpie know that we always talk about the benefits of long-term investing. Timing the market’s a mug’s game. In light of this, selling my shares after only 12 months opens me up to the charge of hypocrisy. However, in my defence, I thought the war was about to end and that the oil price was close to its peak. The shares were last changing hands for more than 600p just before the Deepwater Horizon disaster in 2010.

However, if BP shares are so sensitive to the oil price, it begs the question: what’s the point of them? It’s impossible to predict future energy prices with any accuracy, therefore what’s the investment case for owning part of the oil and gas giant?

I can think of two reasons…

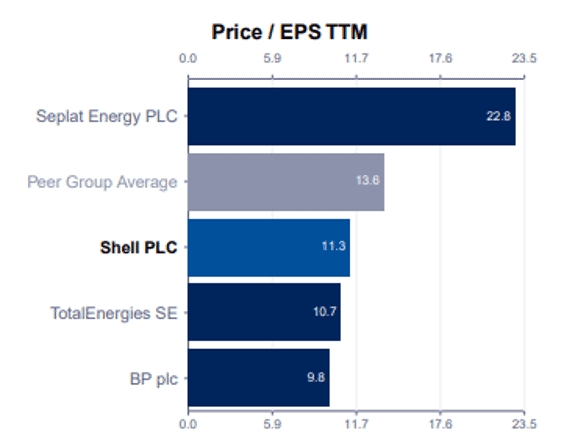

The bull case

Firstly, there’s its dividend. Based on amounts paid over the past 12 months, the stock’s currently (1 July) yielding 5.4%. This puts it in the top 13 of FTSE 100 dividend payers.

Of course, payouts are never guaranteed. In fact, the group’s dividend was cut after the tragic events of 2010, and by 50% during the pandemic. However, post-Covid, it’s been steadily increased once more. In dollar terms, the group’s most recently quarterly payment was 79% of its pre-cut level.

Secondly, compared to others in the sector, the stock’s trading at a lower earnings multiple. For example, if it was valued the same as Shell, BP’s share price would be 15% higher.

My view

So do I want to own BP shares once again? To be honest, not at the moment.

One of the unexpected consequences of the war is the lifting of sanctions that had prevented the export of Iranian oil. This decision might be reversed at a later date but, for now, it could be significant because the country’s believed to have the third-highest level of reserves.

Flooding the market with Iranian oil could have a big impact, especially when there’s already expected to be an over-supply when shipping movements in the Gulf return to normal. Some analysts are expecting Brent crude to fall to $55 a barrel. It was last at this level in early 2021, when the BP share price was around 250p.

At the moment, I think there’s more uncertainty than usual surrounding the oil price. On this basis, I think there are better opportunities to consider elsewhere, despite the obvious attraction of BP’s dividend.

Should you invest £5,000 in Bp P.l.c. right now?

When investing expert Mark Rogers and his team have a stock tip, it can pay to listen. After all, the flagship Twelfth Magpie Share Advisor newsletter he has run for nearly a decade has provided thousands of paying members with top stock recommendations from the UK and US markets.

And right now, Mark thinks there are 6 standout stocks that investors should consider buying. Want to see if Bp P.l.c. made the list?

James Beard does not hold any positions in the companies mentioned.