Earlier this week, I added two companies to my Stocks and Shares ISA. Both were new buys for me. And here’s why I’m bullish on this pair moving forward.

Dirt cheap UK small-cap

The first stock was Hostelworld (LSE:HSW), the leading platform for booking hostels around the globe. At 110p per share, it currently has a £137m market-cap, meaning it’s not currently a large company.

Now, this isn’t a stock I ever thought I would take a small stake in because growth hasn’t exactly been stellar over the past few years. Indeed, it fell off a cliff during the pandemic when international travel came to a shuddering halt.

This forced the Dublin-based company to issue shares and rely on debt to survive. So the lesson here is that another major travel-disrupting event is a key risk for Hostelworld shareholders.

Anyway, why have I changed my mind? Well, whereas the company once relied almost exclusively on commissions from hostel bookings, it now has four revenue drivers.

- Core bookings, which have been enhanced through Elevate (a tool allowing for dynamic commission rates).

- Social Passes (a subscription-based revenue stream).

- Massive inventory expansion, including guesthouses and budget hotels.

- Events and experiences following the acquisition of OccasionGenius.

Of these, Social Passes could be a gamechanger. Launched in November, these allow paying customers temporary access to Hostelworld’s social features without being a customer, allowing travellers to arrange meet-ups, attend events, and meet new people in 3,000+ cities.

It’s worth noting that this revenue should be high-margin. In other words, every euro generated from a Social Pass sale should eventually be very profitable (beyond the initial marketing costs to drive awareness).

Additionally, the company benefits because these new users create more data, improving its AI-driven event recommendations. Last year, messaging between people on the platform surged 81%.

For me though, the icing on the cake is the valuation. Profits are expected to grow substantially over the next two years, putting the stock on a forward-looking price-to-earnings (P/E) ratio of just 7.4 for 2027.

Add in a well-covered forward yield of 3.3%, and the stock looks great value to me.

Bringing AI to the physical world

The second stock I bought was Samsara (NYSE:IOT), which currently has a $17bn market-cap.

This is an Internet of Things firm whose platform helps businesses track and manage their physical assets, including lorries, garbage trucks, school buses, trailers, and heavy equipment such as cranes.

Q1 revenue surged 31% to $478m, and Samsara achieved its third straight profitable quarter. Recent customer wins include Hertz, Sainsbury’s, and one of the world’s largest pizza firms.

Admittedly, Samsara is a software/platform company, and many of these are theoretically at risk from rapid AI advances. This is something I’ll keep monitoring moving forward.

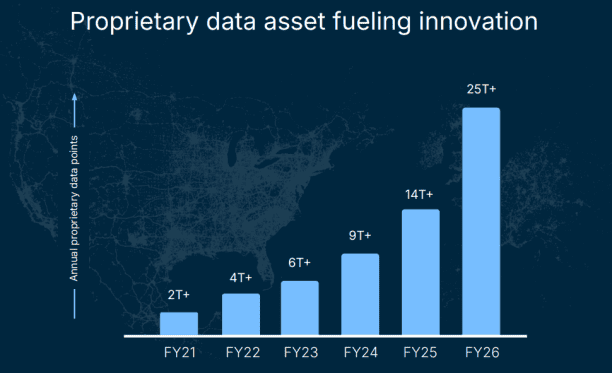

However, to my mind, the firm does have a defensible business. In 2025 alone, it captured over 25trn real-world data points from the connected vehicles, equipment, worksites, and operations across its network.

Crucially, this is a real-time dataset, meaning it can’t be easily replicated.

Powered by this data, Samsara’s rolling out lots of AI-powered features, including AI agents automating tasks like managing paperwork and communicating with drivers.

Down 35% since December, I reckon Samsara’s a dip-buying opportunity worth exploring further at $29 per share.

Should you invest £5,000 in Samsara right now?

When investing expert Mark Rogers and his team have a stock tip, it can pay to listen. After all, the flagship Twelfth Magpie Share Advisor newsletter he has run for nearly a decade has provided thousands of paying members with top stock recommendations from the UK and US markets.

And right now, Mark thinks there are 6 standout stocks that investors should consider buying. Want to see if Samsara made the list?

Ben McPoland owns shares in Hostelworld and Samsara.