Stocks and Shares ISAs have proven excellent ways to create wealth down the years. The data is in to prove it. So why do so many more Britons prefer to leave their money locked up in low-yield Cash ISAs?

A total of £69.5bn was saved in these cash-based products in the 2023/2024 tax year, latest data shows. That’s more than double the £31.1bn invested in the stocks-based equivalent.

But here’s the thing: total holdings in stocks ISAs is £511bn, compared to £360bn in the Cash ISA. Why? Over time, investment in the stock market delivers significantly greater returns than simply saving.

Crunching the numbers

Over the past decade, Stocks and Shares ISA users have enjoyed an average annual return of 9.6%. That’s according to Moneyfacts data. By comparison, the Cash ISA’s return sits way back at 1.2%.

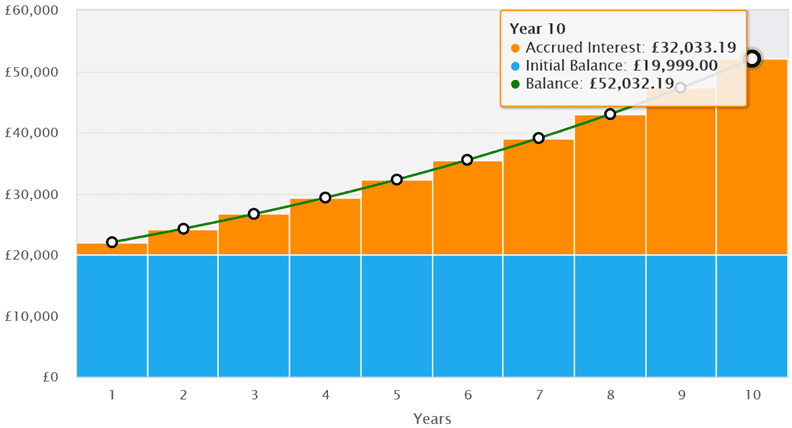

Past performance isn’t always a reliable guide to the future. But if these trends continue, a cash saver with £19,999 on account will make just £22,547 by 2036.

How would this stack up compared to the shares ISA? The difference is enormous, with this product delivering a £52,032 total return.

Sprinkle in some regular investments over the period and the gap becomes even wider. This is because each contribution made in a Stocks and Shares ISA has the opportunity to compound at that much higher rate.

If someone added an extra £500 a month on top of their initial £19,000i investment, they’d have:

- £152,141 after 10 years in a Stocks and Shares ISA.

- Or £86,262 over the same period in a Cash ISA.

So what’s the catch?

If this is the case, why don’t more of us in the UK invest in the stock market? The problem is perception compared to other countries such as the US, Canada and Australia, and especially when it comes to risk.

With a Cash ISA, it’s not possible to lose money, unless in the unlikely event your account provider goes bust. Cash products also protect individuals from market volatility. Stocks ISAs don’t offer either of those things.

Yet. as that Moneyfacts data shows, over the long term, volatility has a chance to even out and deliver stunning returns. HSBC (LSE:HSBA) is one example of the huge profits that can be made with a patient approach.

A 10.7% opportunity?

There have been some ups and downs for the bank over the last decade. For instance, HSBC’s share price — like the broader FTSE 100 — fell sharply when Covid-19 hit in 2020. Yet through a combination of capital gains and dividends, it’s provided an average annual return of 10.7%.

The reason is chiefly the bank’s rising focus on fast-growing Asian markets. It’s a strategy that’s tipped to keep delivering, even though market competition from digital banks is a growing threat. Asia Pacific’s retail banking sector is expected to swell 6%-8% a year on average between now and the mid-2030s. And areas including wealth management, where HSBC is doubling down, are tipped to rise even more strongly.

There are plenty of top stocks for investors like me to consider in an ISA and this is just one of them. It’s why I’ll never leave money stagnating in a poor-returning cash account.

Should you invest £5,000 in HSBC Holdings right now?

When investing expert Mark Rogers and his team have a stock tip, it can pay to listen. After all, the flagship Twelfth Magpie Share Advisor newsletter he has run for nearly a decade has provided thousands of paying members with top stock recommendations from the UK and US markets.

And right now, Mark thinks there are 6 standout stocks that investors should consider buying. Want to see if HSBC Holdings made the list?

Royston Wild owns shares in HSBC.