Rolls-Royce shares have powered 14% higher in just two weeks, taking the one-year return to around 55%. Looking at analysts’ one-year price targets, however, the average is just 3.5% above today’s price.

In other words, there could be far juicier wealth-building opportunities elsewhere. Here’s a FTSE 100 stock tipped to generate much higher returns than Rolls-Royce by mid-2027.

Defence powerhouse

Staying in the FTSE 100, I want to highlight BAE Systems (LSE:BA.). Shares of the defence powerhouse have slumped 23% since March and, as I write, currently sit just under 1,800p.

Yet the average 12-month price target is 2,353p, implying a 31% potential gain. And the minimum estimate among analysts covering BAE is 2,050p, which is 14.5% higher.

The most bullish, Morgan Stanley, sees a road to 2,662p — almost 50% more!

None of these targets may be realised, of course, but the stock does look better value than it has done for a while. It’s trading on a forward price-to-earnings (P/E) ratio of 20.5, which is significantly lower than Rolls-Royce (34.5).

Why’s the stock down?

Some of BAE’s decline probably relates to reports that Moscow might (finally) be ready to end the dreadful war in Ukraine. This would presumably reduce the need for continuous munitions replenishment.

However, I don’t think this welcome development would change the long-term investment case for BAE. It’s largest market is the US, where Donald Trump has called for a colossal $1.5trn defence budget.

Meanwhile, the US is reducing its military presence in Europe. According to Der Spiegel, Washington is also cutting assets it would commit to the NATO alliance in crisis scenarios, including fighter jets, submarines, warships, and bomber aircraft.

Given this backdrop, it’s very likely that Europe will continue re-arming. And reports say that Andy Burnham, the UK’s ‘Prime Minister-in-waiting’, will boost defence spending above what Keir Starmer had planned.

Finally, oil-rich Gulf states are raising military spending in the wake of the Iran war. Saudi Arabia, which accounts for around 10% of BAE’s revenue, hiked defence spending by 26% in the first quarter after Iran launched strikes around the Gulf.

Therefore, while a stabilisation of the geopolitical environment is a risk, all evidence points towards elevated defence budgets over the medium term.

Around the world, security threats continue to grow, leading governments to increase defence spending…[This] provides a supportive backdrop for growth over the medium term. We expect significant opportunities across our business, including space systems, missile and air defence systems, drones and counter drone technology, electronic warfare, combat aircraft, combat vehicles, frigates and submarines.

BAE Systems, May 2026.

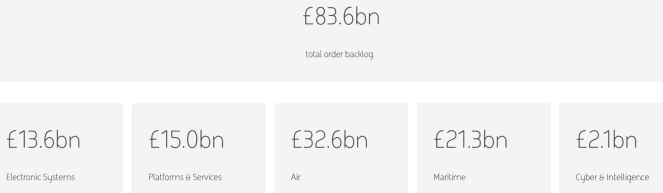

Massive backlog

BAE’s order backlog has swelled to £83.6bn across its operating segments. Due to the nature of these multi-year (often multi-decade) programmes, the company enjoys strong earnings visibility.

In 2026, management sees underlying profits rising as much as 11%. And it expects free cash flow to be above £6bn between 2026 and 2028, which will support 9%–12% dividend growth, according to forecasts.

BAE has increased its payout for 22 straight years. Right now, the stock is offering a well-covered 2.3% forward yield.

Adding all this up, I think BAE is worth considering buying on this dip. I expect it to be trading higher in a couple of years’ time, so plan to keep holding my shares.

Should you invest £5,000 in BAE Systems right now?

When investing expert Mark Rogers and his team have a stock tip, it can pay to listen. After all, the flagship Twelfth Magpie Share Advisor newsletter he has run for nearly a decade has provided thousands of paying members with top stock recommendations from the UK and US markets.

And right now, Mark thinks there are 6 standout stocks that investors should consider buying. Want to see if BAE Systems made the list?

Ben McPoland owns shares in BAE Systems and Rolls-Royce.