Space Exploration Technologies (NASDAQ:SPCX) stock has followed the same trajectory as one of SpaceX’s rockets since its debut a couple of weeks ago.

Once the IPO countdown ended, it blasted off the launchpad and quickly reached $225, cheered on by enthusiastic crowds of retail investors. Then the stock started falling back to Earth.

Yesterday (22 June), it plummeted 16.4% to $154, bringing the decline to roughly 24% in just three days.

But is this simply my chance to invest in a once-in-a-generation company at a marked-down price to aim for riches?

Beating the rest of the world combined

Let me start with a confession: I’m a bit narked off with SpaceX’s mega-IPO. That’s because I’ve been following the company for over a decade now. I was one of those geeks watching Elon Musk’s early presentations on reusable rockets and plans for a Mars colony.

However, because Musk was able to use his entrepreneurial skills to raise ample capital privately, SpaceX didn’t need to IPO earlier on. So I wasn’t able to invest in the high-risk, high-reward space exploration firm.

Beyond the stellar vision, what I liked was that the company was bringing a modern software and iterative development to rocket engineering. And by manufacturing most of its components in-house, the firm eventually bypassed the high-cost supply chain of the aerospace industry, thereby massively lowering costs and speeding up innovation.

The facts speak for themselves. last year, SpaceX’s Falcon 9 rocket did an incredible 165 missions, up from 26 in 2020.

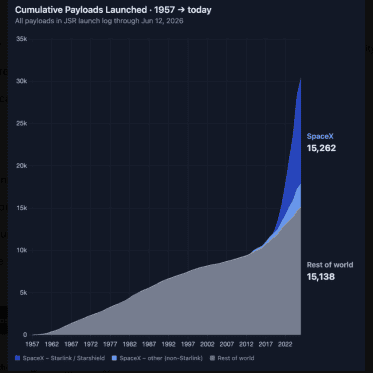

And according to space industry veteran Christian Keil, it has now launched more satellites than the rest of humanity combined — despite the latter having a 61-year head start!

Starlink is the star

Of course, today’s SpaceX isn’t just a rocket launch provider. It’s also the operator of Starlink, the satellite network that provides reliable, high-speed internet across the globe.

Last year, this division racked up revenue of $11.4bn, approximatively 50% year-on-year growth, and a $4.4bn operating profit. Starlink recently surpassed 12m active subscribers.

But this figure is set to grow enormously because SpaceX owns the launch capacity. So it can deploy its own satellites at a speed and cost that is impossible for competitors to match.

As such, the company has possibly the strongest competitive advantage I’ve ever seen. I mean, the barriers to entry in space are simply enormous, both in terms of capital and high technological complexity. Then there are myriad regulatory hurdles.

By the time a rival matches Starlink’s near-10,000 satellite mega-constellation, SpaceX could have its gigantic Starship system up and running. And this would be large enough to carry massive payloads, including potentially space-based data centres and cargo to the Moon.

Is SpaceX a millionaire-maker?

As exciting as this is, I’m put off by SpaceX’s $2trn market cap. At this size, most of the future growth potential already looks priced in, considering that the firm’s revenue was $18.7bn last year. It’s also currently loss-making, which adds risk.

Therefore, unlike an early Tesla or Nvidia, it’s very unlikely SpaceX will turn £10k into £1m from here. The starting valuation is just too large.

That said, if the stock keeps losing altitude and drifts under $100, I’ll become much more interested. After all, this remains a unique company with incredible growth potential.

Should you invest £5,000 in Space Exploration Technologies Corp. - Class A right now?

When investing expert Mark Rogers and his team have a stock tip, it can pay to listen. After all, the flagship Twelfth Magpie Share Advisor newsletter he has run for nearly a decade has provided thousands of paying members with top stock recommendations from the UK and US markets.

And right now, Mark thinks there are 6 standout stocks that investors should consider buying. Want to see if Space Exploration Technologies Corp. - Class A made the list?

Ben McPoland owns shares in Nvidia.