A change in UK Prime Minister probably matters more for the FTSE 250 than the FTSE 100. And that’s suddenly become hugely relevant.

Keir Starmer has resigned and Andy Burnham is the current favourite to take over. But what could that mean for the FTSE 250 stocks in my portfolio?

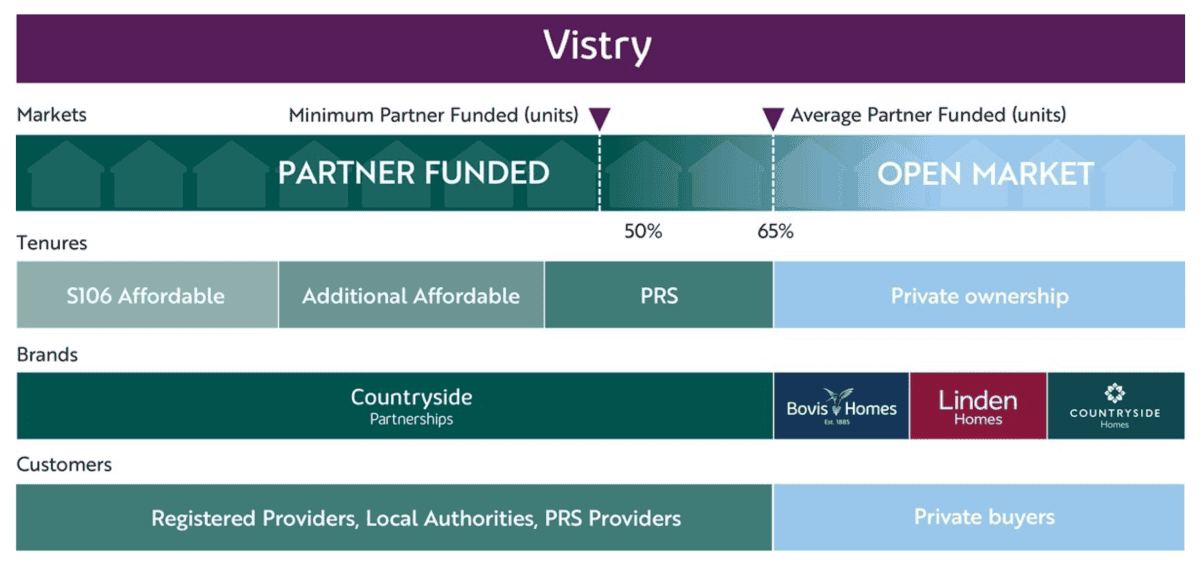

Vistry: same model, different tenants

Vistry (LSE:VTY) has been a horrendous stock recently. The debt on the firm’s balance sheet means it’s been struggling more than other UK housebuilders.

The big positive is the £39bn Social and Affordable Homes Programme (SAHP), which runs until 2036. The firm’s existing partnerships put it in a strong position.

Source: Company Website

There’s speculation that a Burnham government might tilt the SAHP away from the private sector and towards traditional social housing. Does that matter for Vistry?

I think it’s neutral at worst. The group has Strategic Partner-Plus status with Homes England through its Hestia joint venture.

No other listed UK builder has that central role. And with a forward order book of around £4bn, Vistry is well placed to play a major role in a revised SAHP.

A shift in the tenancies doesn’t change who holds the shovel. Whether it’s the private sector or housing associations, I think the FTSE 250 company is still in a strong position.

JD Wetherspoon: careful what you wish for

A Burnham government pledging to ease employer costs might look like good news for JD Wetherspoon (LSE:JDW) shareholders. And I think the stock market might see it as such.

The company says October’s National Insurance rise is set to cost around £60m a year. But I’m not convinced relief would be unambiguously good.

It’s definitely tough in the hospitality industry. But JD Wetherspoon has consistently outperformed the field (at least, according to the CGA RSM Hospitality Business Tracker).

That’s mostly because its pints are typically around 33% cheaper than elsewhere. And the scale benefits that support this are a durable competitive strength.

Lower employer NI would reduce pressure on rivals that have been raising prices or closing entirely. And I think that would probably level the playing field.

In the short term, it might mean better margins. But I’m not convinced that more competition where JD Wetherspoon has been winning is what its shareholders should be hoping for.

The shared risk worth naming

Both Vistry and JD Wetherspoon face a scenario investors should keep in mind. It’s the downside of more employment and higher wages.

These are good for housing demand and pub traffic. But they also push up input costs.

Vistry has already flagged inflationary pressures. And JD Wetherspoon runs tighter margins than most of its rivals.

A more stimulative government that reignites wage inflation would be tough for both. So there’s a lot to think about.

My view

Whether it’s Burnham or anyone else, I want to own shares in businesses with enduring strengths. And nothing on that front has changed my mind this week.

Changes in government policy could have an impact on Vistry and JD Wetherspoon. But the smart investor backs long-term quality over short-term noise.

I think both Vistry and JD Wetherspoon have enduring competitive strengths. And that’s why I’m likely to keep buying both, regardless of who’s running the country.