Lloyds Banking Group (LSE:LLOY) shares are up 29.77% in the last 12 months. But what will the next year bring?

Analysts are pretty optimistic about the stock. There are, however, some warning signs to pay attention to.

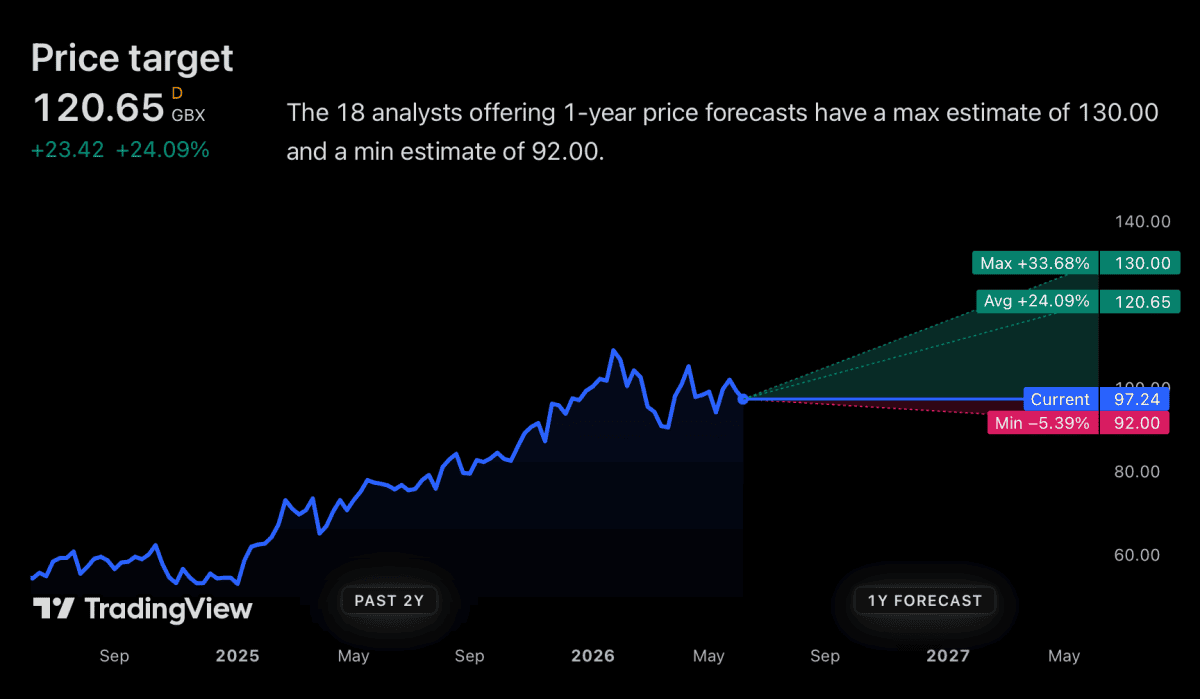

What are analysts saying?

Lloyds stock might be on the up, but analysts think there’s more to come. The average price target is 24.07% above the current level:

Source: TradingView

There are definitely reasons for positivity. One of these is the Bank of England’s decision to relax capital requirements for UK banks.

Lloyds – like most banks – sets internal targets well above the minimum level. But lower requirements mean more available cash.

There are lots of opportunities, including dividends and share buybacks. And these undoubtedly make the stock more attractive.

Regulatory change is one reason analysts are positive about the stock. But it’s not the only one.

Reasons for optimism

Returns on tangible equity are a key measure of bank profitability. And Lloyds is aiming for around 16% in the year ahead.

That’s unusually high. Over the last 10 years, that figure has tended to be somewhere between 10% and 11%.

There’s also good news in the form of less bad news. One of the issues hanging over the Lloyds share price had been potential motor loan liabilities.

A favourable ruling means the extent of the damage is likely to be limited. And that’s another reason for optimism.

The stock might be close to five-year highs, but there’s no rule saying it can’t go even higher. So, is it one to consider buying?

Time to buy?

Banking is a cyclical business. And that means there are natural ups and downs in things like profits and returns on equity.

This is no secret. But it’s the kind of thing that the stock market as a whole is notoriously bad at paying attention to.

There’s a reason Lloyds hasn’t managed to sustain 16% returns on tangible equity before. It’s because lending is competitive.

Interest rates have been coming down steadily since August 2024. And that puts pressure on margins for loan originators.

Given this, buying the stock at a 70% premium to its tangible book value looks risky to me. Especially for the long term.

Warren Buffett

Analysts are bullish on the next 12 months for Lloyds. But from a long-term perspective, I’m wary about cyclical pressures at current valuations.

Something Warren Buffett says about buying stocks stands out to me in this context: “If you aren’t willing to own a stock for 10 years, don’t even think about owning it for 10 minutes.”

The next 12 months look very positive for Lloyds. But I’m wary about the idea that this might be representative of the next 10 years.

It may well be that analysts are right and the stock hasn’t yet peaked. My concern, however, is that it’s nearer the high point of the cycle than the low point.

The paradox of the analyst

Analysts are pretty optimistic about Lloyds at the moment. But – somewhat paradoxically – that makes me more wary.

In my view, investing well is about finding opportunities when others are wary. And that’s especially true of cyclicals.

That’s definitely not the case with Lloyds right now. So I’m going to bide my time on this one and focus on other opportunities.

Should you invest £5,000 in Lloyds Banking Group Plc right now?

When investing expert Mark Rogers and his team have a stock tip, it can pay to listen. After all, the flagship Twelfth Magpie Share Advisor newsletter he has run for nearly a decade has provided thousands of paying members with top stock recommendations from the UK and US markets.

And right now, Mark thinks there are 6 standout stocks that investors should consider buying. Want to see if Lloyds Banking Group Plc made the list?

Stephen Wright does not own shares in any of the companies mentioned.