Insurance stocks often stand out to income investors. And big dividend yields mean it’s easy to see why. I own shares in a FTSE 100 insurer, but my top pick isn’t the most obvious from a passive income perspective.

Dividend yields

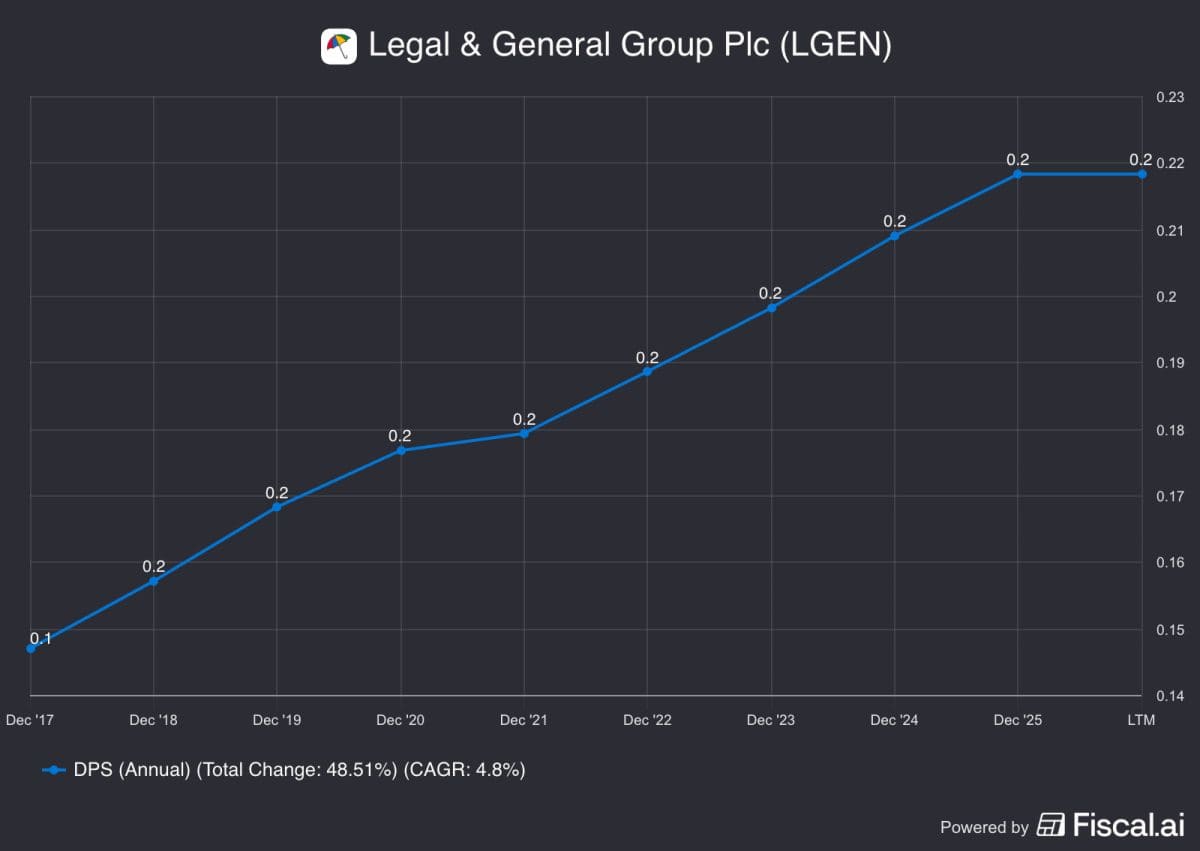

High dividend yields can be a sign of risk. But the likes of Legal & General have been pretty consistent when it comes to paying out.

Source: Fiscal.ai

So what are investors worried about? I think a lot of the time, the answer is that they don’t really know.

Insurance companies are complicated. And that brings uncertainty. Solvency ratios and accounting conventions can be hugely complicated. Even for industry specialists. This, understandably, makes investors wary. And the high dividend yields are essentially compensation for the unknown risks.

My top picks

I’m not claiming to be able to understand insurance accounting better than the specialists. But I do own shares in three insurance companies:

- Berkshire Hathaway

- Molina Healthcare

- Admiral (LSE:ADM)

In dividend terms, these are unusual. Two don’t pay one at all and the third has just lowered its distribution.

The reason I own all of these is the same. I think there’s something unique about each that puts them ahead of the competition. Berkshire has a powerful balance sheet and Molina has the lowest costs in its industry. But with Admiral, it’s something else entirely.

Why Admiral?

Ultimately, insurance is about taking in more money in premiums than you pay out in claims. And Admiral is the UK’s best at doing this. Its underwriting margins consistently lead the industry and that’s no accident. It’s due to the firm having better data than its rivals.

Could artificial intelligence (AI) close this gap? The honest answer is I’m not entirely sure and that creates a risk for the company. The issue isn’t that other insurers will have better data – I don’t think that’s likely. It’s that they might be able to do more with less.

Even if this happens, I still think better data should give Admiral an advantage. That’s why I own the stock, but I’m watching the AI threat closely.

Passive income

The latest dividend from Admiral is set to hit my account tomorrow (5 June). And it’s going to be lower than in previous years. That might look like a sign of weakness, but it isn’t. The firm isn’t making less money, it’s just changing how it uses it.

It’s going to start channelling cash towards share buybacks to fund its employee compensation scheme. And I’m in favour of that move.

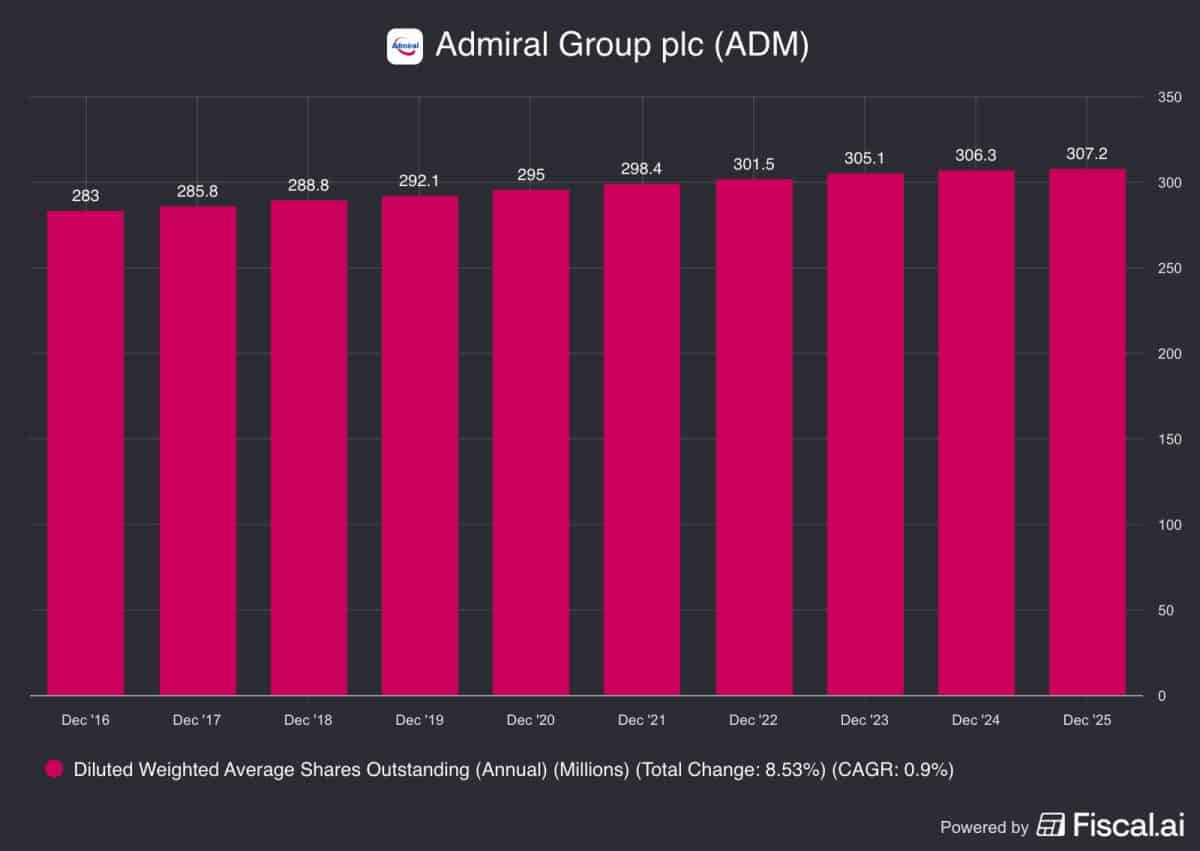

Source: Fiscal.ai

Admiral’s share count has been increasing by just under 1% a year. That somewhat offsets the value of the cash returned via dividends.

Even with the lower dividend, the yield is still above the FTSE 100 average. So it’s still my top choice of the UK insurers.

Being a good investor

Billionaire investor Warren Buffett says that risk comes from not knowing what you’re doing. I think that’s especially true of insurance stocks. It can be tempting to take a high dividend yield in exchange for risks that are hard to quantify. But I think that’s a dangerous strategy.

Far better, in my view, to focus on companies with a clear competitive advantage. That’s why Admiral’s the stock on my to-buy list.

Should you invest £5,000 in Admiral Group Plc right now?

When investing expert Mark Rogers and his team have a stock tip, it can pay to listen. After all, the flagship Twelfth Magpie Share Advisor newsletter he has run for nearly a decade has provided thousands of paying members with top stock recommendations from the UK and US markets.

And right now, Mark thinks there are 6 standout stocks that investors should consider buying. Want to see if Admiral Group Plc made the list?

Stephen Wright owns shares in Admiral, Berkshire Hathaway, and Molina Healthcare.