A Stocks and Shares ISA is often promoted as a route to generating a sizeable passive income. But while return assumptions matter, the bigger influence is often how consistently investors keep putting money to work over time.

Some contribute steadily through market cycles. Others pause, delay, or invest more heavily later in life. Those differences can have a surprisingly large impact on how quickly an income target is reached.

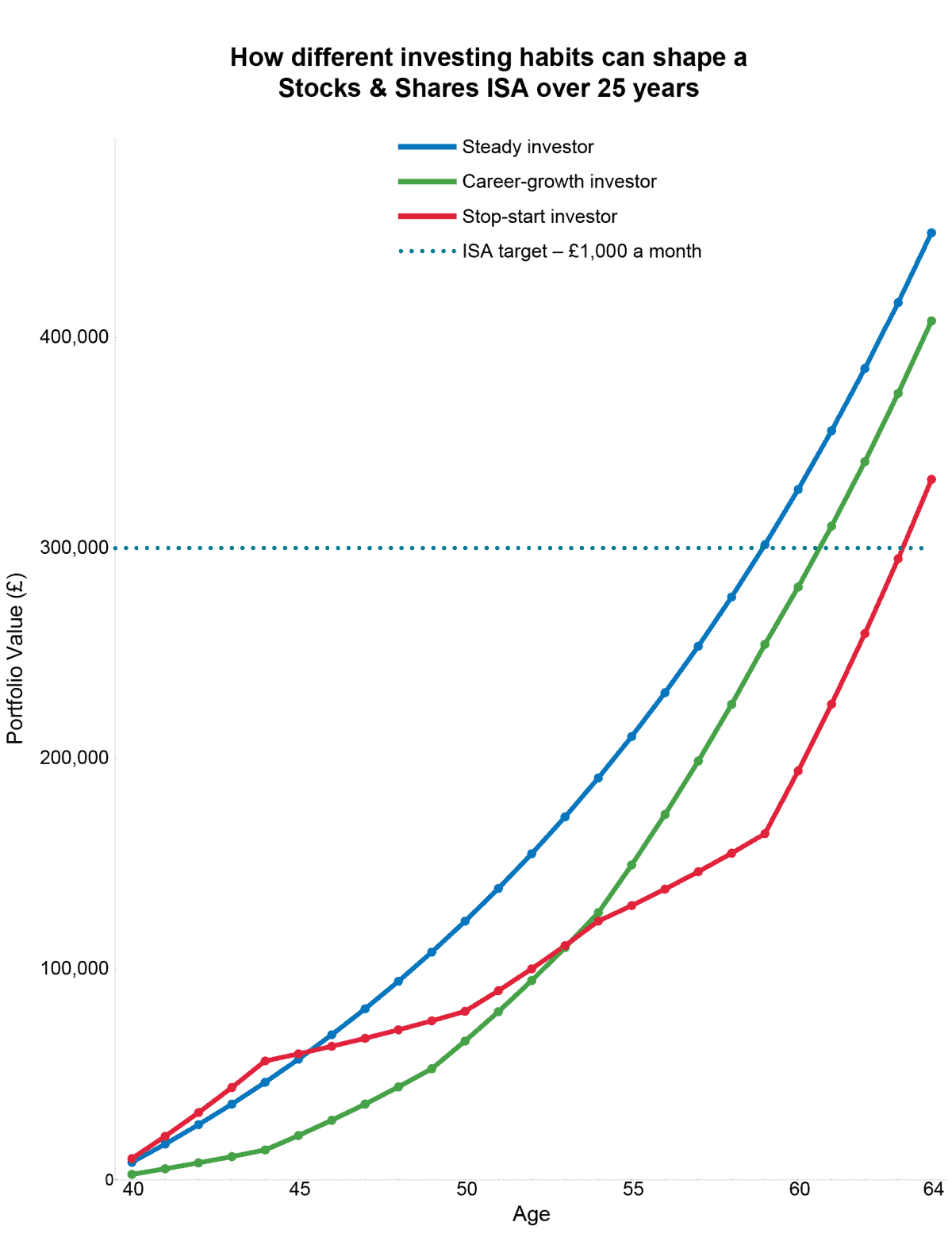

Consistency matters

The challenge with long-term ISA planning is that life rarely follows the spreadsheet. Contributions tend to rise, pause, or fluctuate as circumstances change.

Income, career progression, and market volatility all influence how people invest in practice. Some steadily increase contributions as earnings grow, while others move in and out of the market depending on confidence or financial pressures.

The chart below shows how those different behaviours can lead to very different outcomes over a 25-year period. While all three hypothetical investors ultimately build sizeable portfolios, the speed at which they reach a meaningful financial milestone varies significantly.

That difference matters. Long-term results are shaped not just by assumed returns (here modelled at 6%), but by how continuously capital is put to work and allowed to compound.

Chart generated by author

Quality compounder

A chart can illustrate how investor behaviour shapes long-term outcomes. But stock selection matters too. Companies capable of steadily growing earnings and reinvesting capital effectively can reduce the pressure on future contributions and help smooth the journey towards a second income.

One business I think deserves consideration is Diploma (LSE: DPLM). The FTSE 100 distributor has built a long track record of what management calls “sustainable quality compounding”, combining organic growth with disciplined acquisitions.

Its largest division, Controls, has enjoyed a strong start to 2026, delivering organic growth of 26%. End markets such as aerospace, defence, data centres, and energy continue to provide strong momentum.

Acquisitions remain central to the investment case, but what matters is not simply the number of deals completed — it’s where capital is being deployed.

Over the last 12 months, the group completed 15 acquisitions worth roughly £310m. Rather than pursuing large mergers, the company targets smaller specialist businesses operating in technical niche markets.

The proposed acquisition of CDM illustrates this strategy clearly. The US interconnect business supplies custom cable and connector solutions to defence and industrial applications. This expands exposure to markets where technical expertise and customer relationships create barriers to entry.

Importantly, this expansion has not stretched the balance sheet. Leverage remains modest at just 0.8 times EBITDA (earnings before interest, tax, depreciation, and amortisation).

What could go wrong?

No acquisition-led growth strategy is risk free.

Controls has benefited from exceptionally favourable conditions and that pace may not continue indefinitely. Defence, energy, and data centre spending can fluctuate, while weaker industrial demand could weigh on parts of the portfolio.

There is also execution risk. Its valuation increasingly assumes management can continue integrating acquisitions successfully while maintaining disciplined pricing. If deal quality deteriorates or growth slows materially, the premium rating may come under pressure.

That said, for investors building long-term wealth inside an ISA, Diploma still looks like the type of business worth close attention. Its two-decade record of disciplined growth, strong returns, and exposure to structural growth markets helps explain why the shares command a premium valuation — and why the long-term compounding story may not be over yet.

Should you invest £5,000 in Diploma Plc right now?

When investing expert Mark Rogers and his team have a stock tip, it can pay to listen. After all, the flagship Twelfth Magpie Share Advisor newsletter he has run for nearly a decade has provided thousands of paying members with top stock recommendations from the UK and US markets.

And right now, Mark thinks there are 6 standout stocks that investors should consider buying. Want to see if Diploma Plc made the list?

Andrew Mackie owns shares in Diploma.