As data centre stocks come under pressure, where should investors look for potential buying opportunities in July? I have a few ideas on my own stocks to buy list that I think are worth checking out.

Croda International: watch for the recovery

Croda International (LSE: CRDA) has endured a rough few years. The pandemic-era lipid boom unwound sharply, leaving the stock nursing a painful hangover.

The numbers, however, are genuinely turning. Sales and profits have been recovering over the last nine months and there are encouraging signs ahead.

Management has guided for organic sales growth of 3%-6% in 2026, with further margin expansion. And the next update is due at the end of July.

The key risk is that Life Sciences – especially Crop Protection – remains susceptible to inventory channel cycles. And that’s hard to avoid.

Long-term investors, however, can look to ride the waves a bit with this one. The company’s key competitive strengths are still firmly intact.

Source: Fiscal.ai

The stock isn’t far from its 52-week highs, but it’s near a 10-year low in terms of valuation multiples. So I think it’s definitely worth a look at today’s prices.

Renew Holdings: UK infrastructure

Andy Burnham is widely expected to become Britain’s next Prime Minister. And the Makerfield MP is focused on infrastructure.

I think that could be a huge boost for Renew Holdings (LSE:RNWH). The stock market, however, doesn’t seem to be hugely positive.

Renew is Network Rail’s largest infrastructure services supplier (think HS2 expansion). And it’s also heavily involved in the water business (another key priority).

The point isn’t just that spending is set to increase. It’s that infrastructure investments should bring long-term maintenance contracts, which is where Renew specialises.

Operating margins are only around 5.3%, so delays to projects can have a disproportionate effect on profits. Unironically, investors have seen plenty of those recently.

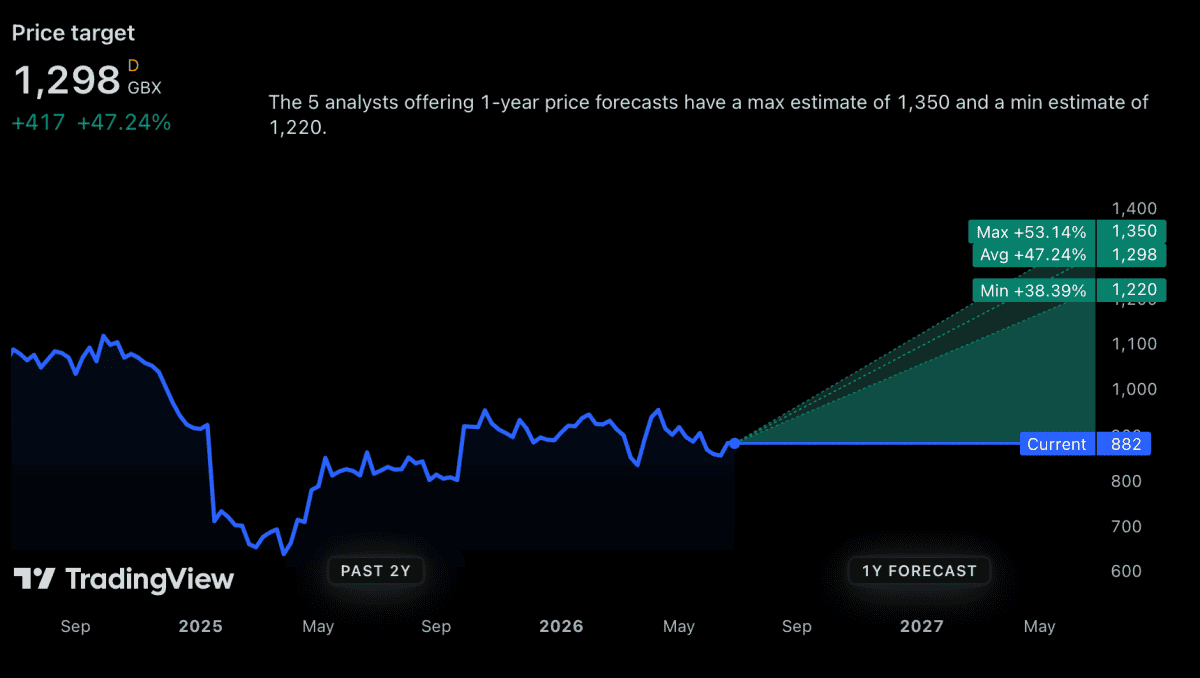

Source: TradingView

The stock, however, is trading at a significant discount to analyst price targets. And I agree that it’s worth checking out in July.

MercadoLibre: Latin American fortress

MercadoLibre (NASDAQ: MELI) isn’t a traditional retailer. It’s the leading e-commerce marketplace, the largest digital payments network, and a growing logistics operator across Latin America.

Foreign exchange rates are often a risk. But anyone who thinks it’s the same for all businesses hasn’t been paying attention to Argentina in the last few years.

Behind a fluctuating currency, the company has been making huge progress. The stock market, however, seems to be ignoring this.

MercadoLibre shares are down 37% over the last year and the big reason for this is margin compression. But I think that’s a feature, not a bug.

The firm’s infrastructure investments make it extremely hard to compete with. And shipping costs in Brazil fell 17% compared to the previous year.

In other words, the network is getting cheaper to run as it continues to clock 49% net revenue growth. That’s a powerful combination that I think deserves attention.

What I’m doing

It’s always possible that something dramatic happens in the stock market. And that could force other names onto my buying radar in July.

As it stands, however, Croda International, Renew Holdings and MercadoLibre are all on my buy list. And I’m optimistic about all three over the long term.

Should you invest £5,000 in Croda International Plc right now?

When investing expert Mark Rogers and his team have a stock tip, it can pay to listen. After all, the flagship Twelfth Magpie Share Advisor newsletter he has run for nearly a decade has provided thousands of paying members with top stock recommendations from the UK and US markets.

And right now, Mark thinks there are 6 standout stocks that investors should consider buying. Want to see if Croda International Plc made the list?

Stephen Wright owns shares in Croda International.