I’ve got my eye on a S&P 500 stock that hasn’t traded at a price-to-earnings (P/E) ratio below 20 in the last 10 years. Until now.

I think it’s one of the highest-quality businesses I’ve seen. But it’s down 34.72% in the last 12 months – and I’m interested.

What’s the company?

The stock in question is Broadridge Financial Solutions (NYSE:BR). The company does two things.

The first is managing things like proxy votes for companies. In this context, it connects businesses with brokers and shareholders.

The second is providing the software that facilitates securities trading. This connects banks that want to make trades.

In both cases, the company acts as an intermediary. But bypassing the firm is much easier said than done. Broadridge the easiest way for firms to comply with SEC and FINRA regulations. And its scale means it’s also the cheapest.

A quality business

I think Broadridge is one of the best businesses I’ve looked at as an investor. One reason for this is the firm’s economic properties.

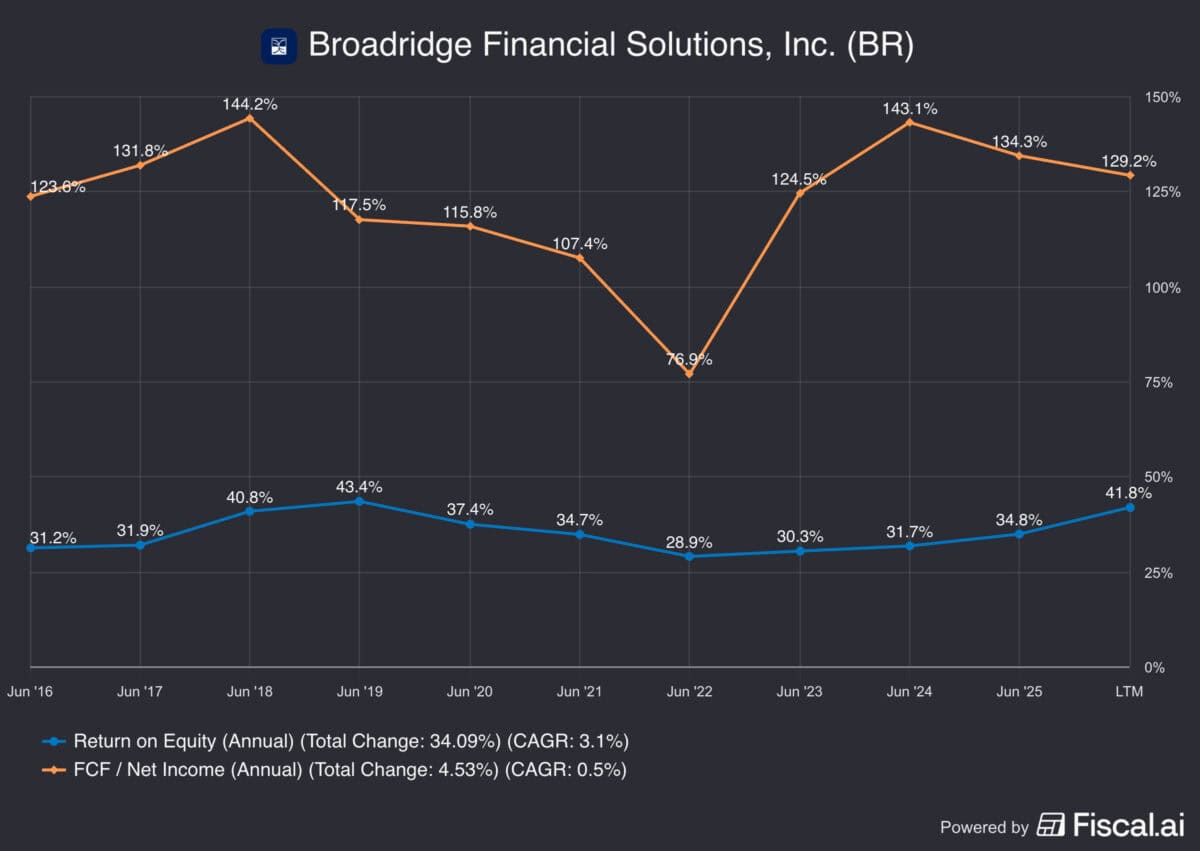

Its average return on equity over the last 10 years has been 38.69%. More importantly, over 100% of its net income becomes free cash flow.

Source: Fiscal.ai

The key to this is the firm’s competitive position. As well as value and convenience, it has other important advantages. Both parts of the company are protected by high switching costs. And that leads to retention rates of around 98%.

This is incredibly impressive. So the obvious question is why is the stock currently trading at decade-low multiples?

Why is the stock falling?

It’s hard to pin down a single reason why the stock is down 41.41% from its highs. But there are a few related factors.

One is the company’s recent infrastructure investments. And another is a 27% decline in event-driven revenues.

These aren’t existential threats. But both are ongoing challenges that investors will need to keep an eye on in the future.

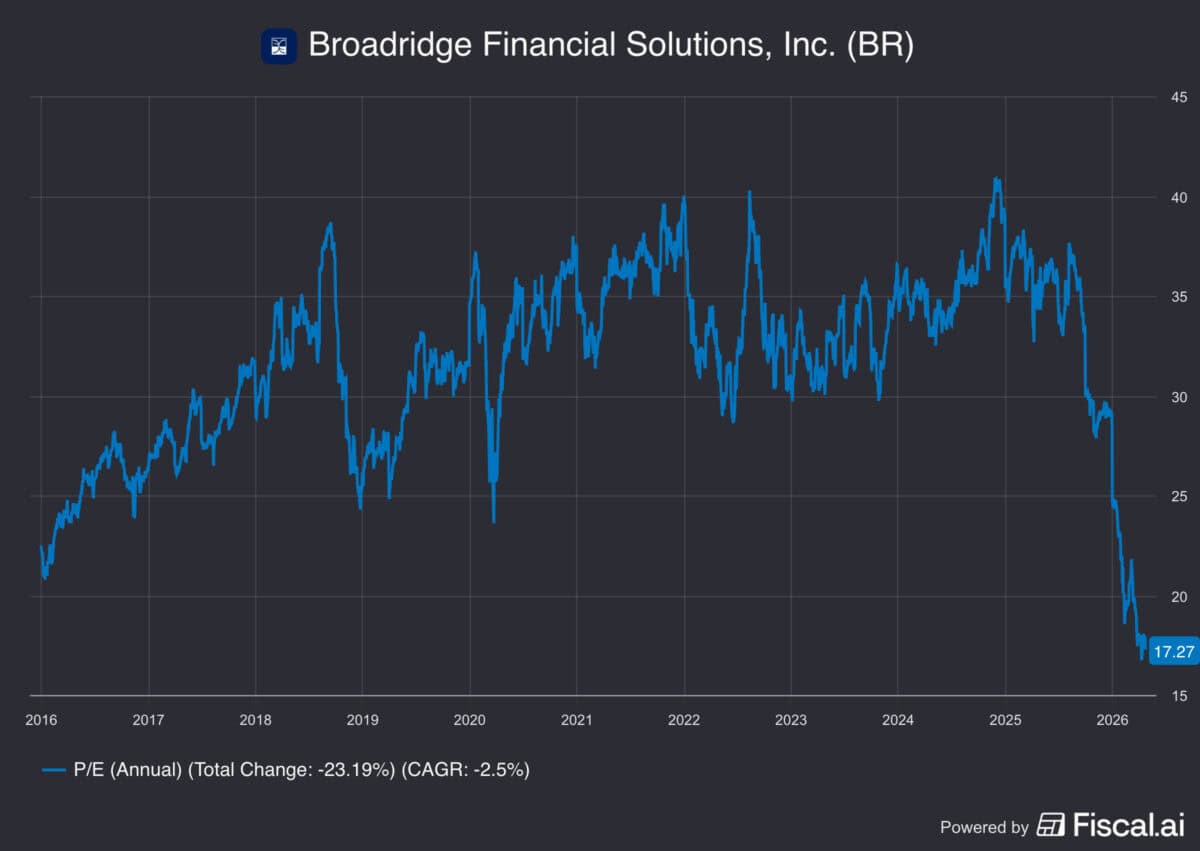

They’re the kind of issues that can have a big impact on a stock trading at a P/E ratio of 36. That’s where Broadridge was a year ago. At today’s levels, however, I think it’s a different story. And that’s why I’m looking at what could be a rare buying opportunity.

A once-in-a-decade opportunity

I’ve had my eye on Broadridge for some time. But I’ve never been willing to buy the stock at the prices it’s been trading at.

I haven’t, however, had the chance to buy it at a P/E ratio of 17. And I think it might well be too cheap for me to pass up.

Source: Fiscal.ai

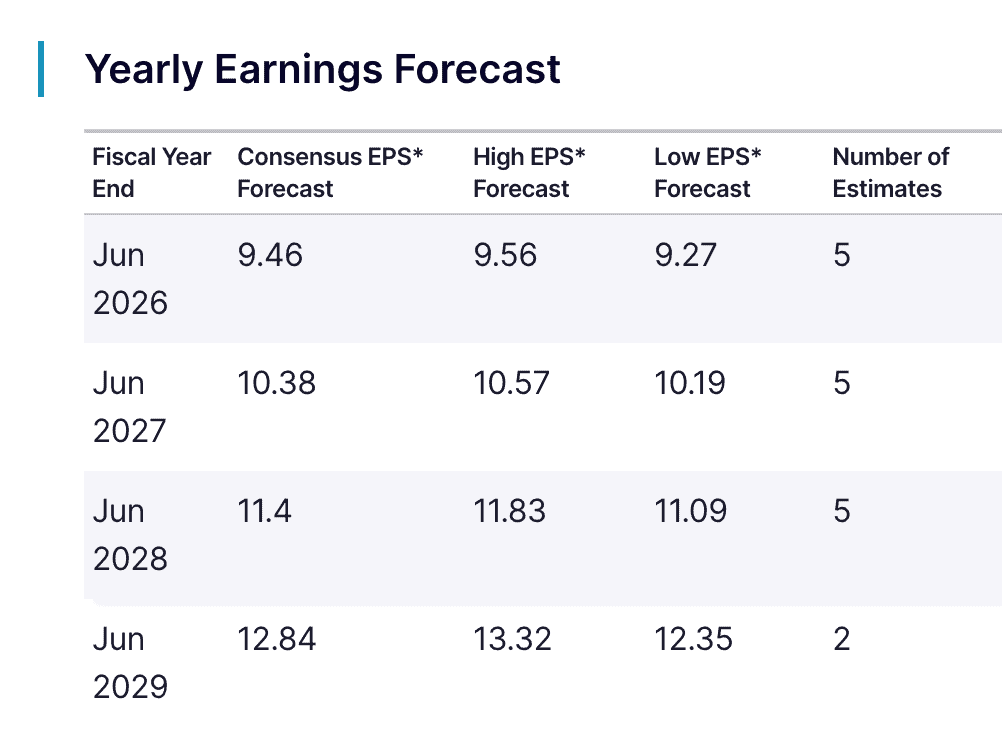

At today’s prices, the implied long-term growth rate for a 9% annual return is 2.81%. That’s well below analyst forecasts.

Earnings per share are expected to grow by at least 9.63% a year until 2029. If that’s even close, there’s a margin of safety for investors.

Source: Nasdaq.com

Can the stock fall further? Absolutely, but at today’s prices, I think the potential opportunity looks pretty compelling.

Buying the dip

A lot of S&P 500 stocks have been falling, especially in the tech sector. But Broadridge isn’t about the threat of AI. I think it’s a quality business that’s dealing with some short-term pressure. But at a P/E multiple of 17, I’m looking to buy.