A recovery stock is typically defined as one that’s experienced a significant share price fall but has a good chance of regaining all of its former value. And there’s one beaten-down stock that’s suffering more than most from the current conflict in the Middle East.

Does this mean it could rebound strongly when the war is over? Or could there be lasting damage? Let’s see.

Who?

Just knowing the name of the company – Gulf Marine Services (LSE:GMS) – is probably enough to understand why it’s share price has fallen 26% in 14 days.

The group owns and operates 15 self-propelled self-elevating support vessels (SESV), which are used by its blue-chip customers primarily in the oil, gas, and renewable energy sectors. A typical use is the refurbishment and maintenance of offshore platforms. SSEVs are self-propelled which means they don’t require other vessels to relocate. This makes them cheaper to hire.

Is it a bargain?

Despite the recent pullback in the group’s share price, I wouldn’t say the stock’s cheap by historical standards.

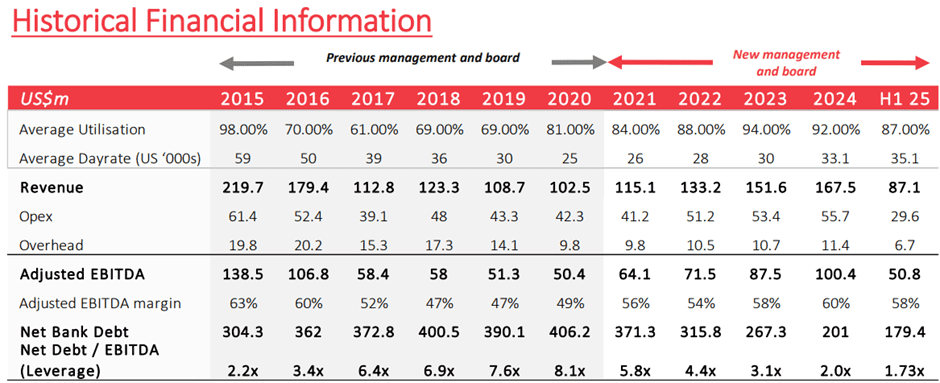

During the 12 months to 30 June 2025, the group reported earnings per share of 3.1 cents (2.33p at current exchange rates). This means its shares are currently trading on 7.5 times earnings. At the end of 2024, its P/E ratio was 5.6. A year earlier, it was 4.7.

But since March 2021, the group’s share price has risen over 350%.

This coincides with a new management team taking over. Since then, the group’s managed to increase revenue, reduce its debt, and improve utilisation rates.

Significantly, the group — which was established in 1977 — has a relatively young fleet with an average age of 13 years. Typically, an SESV will have an operational life of 40 years or more. This means there’s unlikely to be a need for significant capital expenditure any time soon.

Other than geopolitical risks to its operations, other challenges include its large debt pile, which makes it vulnerable to interest rate increases. Although significant progress has been made in reducing borrowings, its 30 June 2025 balance sheet disclosed $189m (£142m) of loans. For context, the group’s current market cap is around £200m.

Despite this, the group has ambitious plans to grow. It wants to double EBITDA (earnings before interest, tax, depreciation, and amortisation) within five years. And it plans to start returning 20%-30% of adjusted net income to shareholders via share buybacks and/or dividends.

My view

Hopefully, the war in the Middle East will end soon. And when it does, I reckon Gulf Marine Services will be able to quickly resume normal operations. At 1 September 2025, it disclosed that it had an order backlog of $474m, equivalent to nearly three years of revenue. This is unlikely to have been materially affected by anything that’s happened in recent days.

And when things do get back to normal, I reckon it’s a stock to consider. Until then, the shares could become cheaper still. Timing the bottom of the market is a mug’s game but with a company so heavily exposed to the region, it’s obvious what it’s going to take to get its share price moving in the right direction again. In the meantime, there are plenty of other UK shares that I’m keeping an eye on too.