The best dividend stocks offer cash returns to investors that can grow over time. And one of the UK’s finest is Renew Holdings (LSE:RNWH).

Investors might not be familiar with the company, but it’s been a very reliable investment. Importantly – especially in today’s stock market – its future prospects look good as well.

Infrastructure

Renew is a specialist in infrastructure maintenance. It’s a firm that operators hire to do things like maintain railway tracks, repair water facilities, and upgrade electricity transmission lines.

There are a lot of good things about this industry. One is that investments are mandated by regulators, so companies don’t have much choice about cutting back on their spending.

Likewise, a focus on ongoing repairs means the business doesn’t depend on infrastructure expansion projects. The existing stuff needs to be maintained, regardless of expansion plans.

Barriers to entry are also reasonably high. Water infrastructure repairs aren’t the kind of thing that a local plumber can do – it requires specialist knowledge and expertise.

Durable growth

As a result, Renew is a resilient company that tends to benefit from relatively reliable demand. And that translates into good things from an investment perspective.

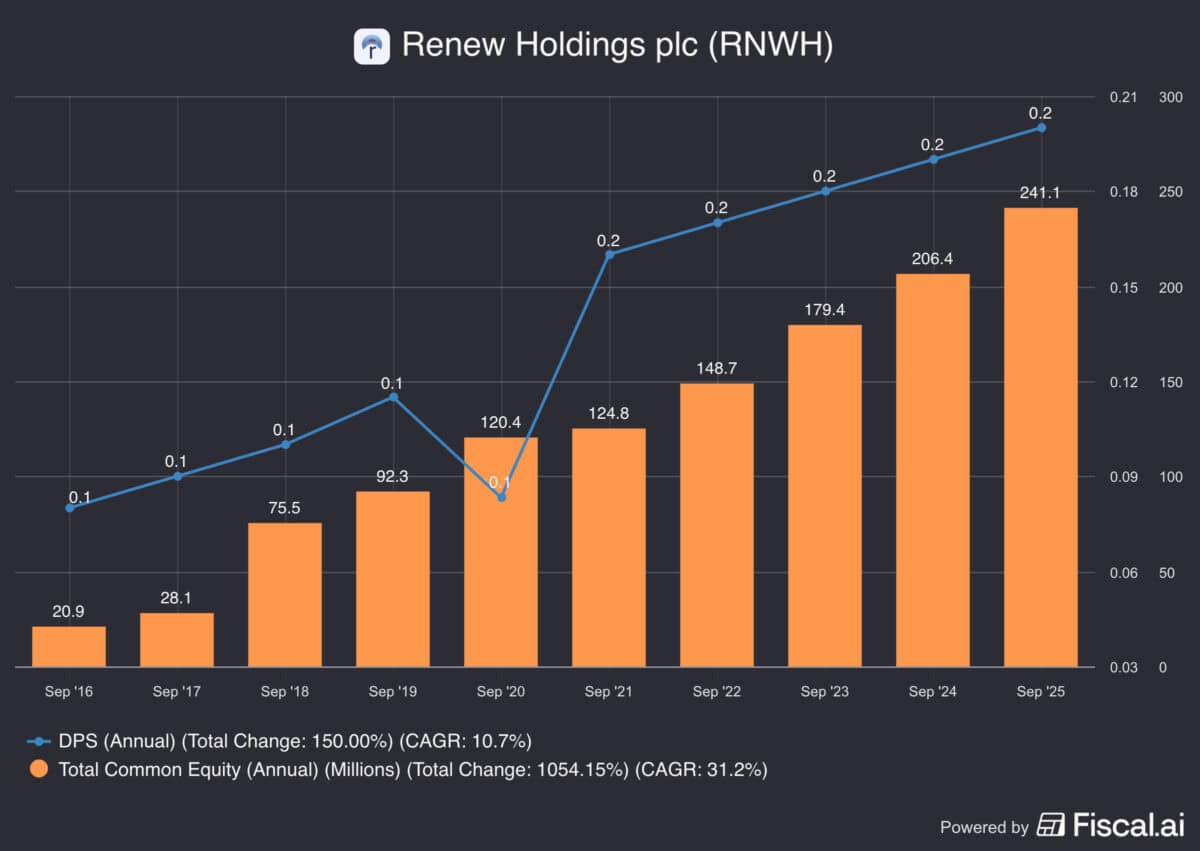

Aside from 2020 – and we all know what happened then – the firm has increased its dividend per share each year over the last decade. And these are not just token increases — they’re 10% a year.

There’s something else though, that’s equally important. That dividend growth hasn’t stopped the underlying business from making investments that have significantly increased its value.

Source: Fiscal.ai

Renew’s dividend has accounted for less than 10% of its free cash flows. And it’s been putting the cash it has retained to good use.

A series of acquisitions has both strengthened the company’s competitive position and increased its book value. Over the last 10 years, shareholder equity has climbed more than tenfold.

So shareholders who bought the stock a decade ago have not only owned a business that’s distributed cash. It’s also grown impressively.

Outlook

Renew’s resilience is impressive. And that’s valuable in a stock market that’s trying to work out which companies are going to be the casualties in the rise of artificial intelligence (AI).

No company however, is risk-free. There’s a lot about the business that isn’t under the firm’s control and delays to things like rail investments can result in profit warnings.

That’s why the stock fell sharply at the start of 2025. And while it’s recovered a fair bit, I still think it looks like good value at a price-to-earnings (P/E) ratio of 16.

Ultimately, my view is that this is one of the UK’s most durable businesses. As a result, share price volatility might be an opportunity that’s worth considering.

Under-the-radar

At first sight, Renew looks like a steady operation, but not a spectacular one. But the company’s acquisition strategy means investors shouldn’t overlook its growth credentials.

The stock’s on my list of businesses I’m paying attention to. And while I haven’t bought it yet, I’m giving it some serious consideration at the moment.