Edinburgh Worldwide Investment Trust (LSE:EWI) is one of the most exciting small-cap growth trusts in the FTSE 250. Yet long-term performance has been disappointing — so much so that the largest shareholder wants to replace the trust’s entire board.

That investor is Boaz Weinstein, whose activist hedge fund Saba Capital owns around 30% of the trust’s shares. He wrote a scathing open letter to Edinburgh Worldwide’s board on 27 November.

Let’s unpack this drama to see if there might be a potential buying opportunity to consider.

Dispruptive growth trust

Edinburgh Worldwide is a £715m investment trust managed by Baillie Gifford. It aims to discover “the next generation of disruptive growth companies…and hold them as they scale, capturing transformational growth opportunities“. These can be public or private businesses.

Now, this makes it higher risk because these “next-generation” companies are by definition less established. Half my own portfolio contains such stocks and I know how unpredictable and volatile they can be. It’s the nature of the beast.

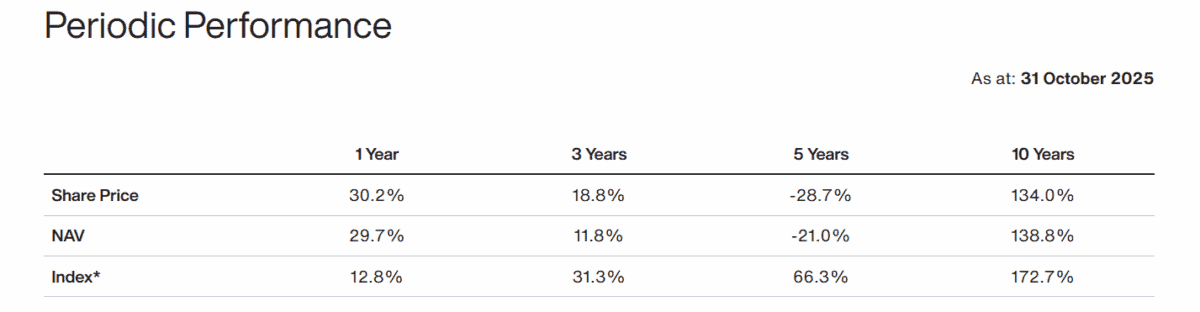

Over time though, the strategy should work, as there’s no shortage of transformational growth opportunities out there. But this is where the problem lies, as the trust has underperformed its benchmark (the S&P Global Small Cap index) over three, five and 10 years.

The share price is down 50% since February 2021.

Back-and-forth drama

Saba Capital wrote that the trust has “massively underperformed its self-selected benchmark, the FTSE All-Share Index (+71.4%), by more than 100 percentage points! The magnitude of this value destruction is unprecedented among peer UK equity investment trusts over this [five-year] period“.

Elsewhere, Weinstein criticised the “inadequate” share buyback activity to close the ongoing discount to net asset value (NAV). In other words, the shares continue to trade for less than the trust’s underlying NAV.

Responding to the letter, Edinburgh Worldwide’s chair Jonathan Simpson-Dent pointed out three things. First, the benchmark isn’t the FTSE All-Share index, as it “makes little sense to judge a global small-cap trust against a UK all-cap benchmark“.

Second, the NAV discount’s currently 5.6%, which is significantly narrower than the peer group weighted average discount of 10.9%.

Finally, performance has been very strong over the past year, easily outperforming the index.

While we are open to discuss Board composition with Saba, we would strongly reject any proposal to replace the entire Board and the ambiguity that would follow. Edinburgh Worldwide.

A change in approach

In the second half of 2024, the trust tweaked its approach. Two new co-managers were appointed alongside the existing lead manager. And it reduced the number of holdings, while bringing in the flexibility to hold larger, more stable growth companies.

This change seems to be working, as the share price is up 40% since mid-2024. And looking at the top of the portfolio, I see some names that I like long term, particularly SpaceX (the largest holding by far), Axon Enterprise, and Alnylam Pharmaceuticals (a biotech focused on RNA-interference therapeutics).

Unlisted quantum computing start-up Psiquantum is also intriguing, though still unproven.

Of course, the hedge fund’s attempt to replace the board adds uncertainty here. But for investors with a tolerance for risk, and who want oversized exposure to SpaceX’s incredible growth, then Edinburgh Worldwide is worth a look at 206p.