Penny stocks are the ultimate high-risk, high-reward investments. These small-cap shares can experience extreme price volatility, and their fortunes can hinge on a single contract, product launch, or slight change in industry conditions. But over time, many of these young companies can (and have) delivered stunning growth that has, in turn, sent their share prices soaring.

Today, I’m on the lookout for the best penny shares to buy. And I’ve come across three that City analysts expect to surge in value over the next 12 months.

Here’s why they’re worth serious consideration right now.

Watkin Jones

Watkin Jones (LSE:WJG) is a construction company specialising in build-to-rent homes, affordable housing, and student accommodation. Given the enormous (and growing) shortages in these property segments, the pricing outlook for the company remains highly favourable.

That’s not to say things are totally comfortable right now. Weakness in the UK economy and higher-than-usual interest rates have impacted trading recently. However, the likelihood of sustained rate cuts means sales volumes are tipped to pick up.

Watkin Jones has a strong balance sheet and a decent pipeline to capture these market improvements, too. It had net cash of £80m as of September.

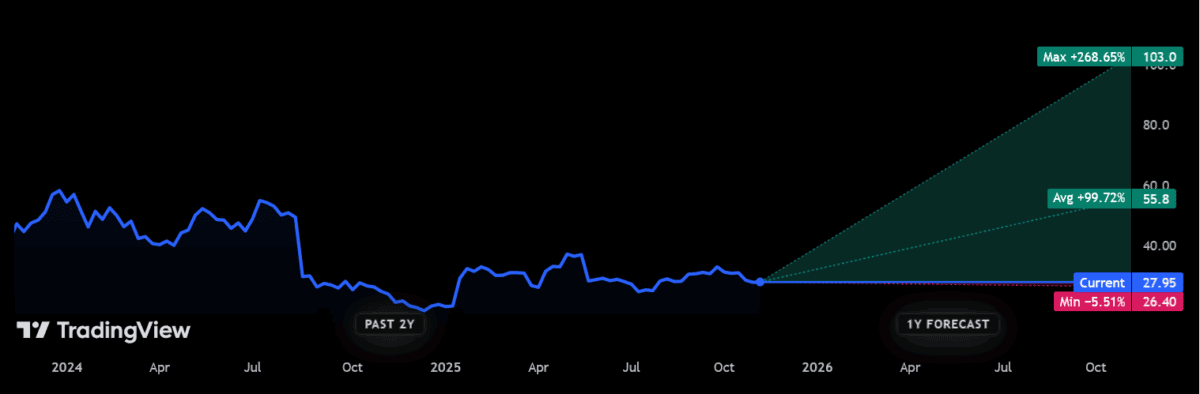

The consensus among City analysts is the builder’s share price will almost double from current levels over the next 12 months, to 55.8p per share.

Premier Miton

Asset manager Premier Miton (LSE:PMI) is also vulnerable in this era of higher interest rates. It’s also a tiny player compared to some of the industry’s other firms, with less financial and brand clout.

Yet, like Watkin Jones, average share price forecasts for the next year are highly encouraging. A 33% rise to 74.2p per share is currently predicted, supported by expected interest rate reductions.

Premier Miton is embarking on widescale cost-cutting to support earnings and offset current market weakness, too. Last month it announced plans for £2m more worth of savings. It’s already achieved roughly £3m worth.

I think this penny stock could thrive over the long term as demographic changes drive investment services demand.

Michelmersh Brick

Michelmersh Brick (LSE:MBH) is highly exposed to interest rate changes and their effect on the housing market. Yet, the broad resilience of homes demand — and the possibility of a pick up when the Bank of England cuts rates — suggests things could be looking up for the building materials supplier.

City analysts broadly agree its share price should surge over the next year. A 59% rise, to 136.5p per share, is predicted. This would clearly take the company firmly out of penny share territory.

The UK’s growing population means a new housebuilding boom looks about to kick off. The government is planning 300,000 new homes each year until 2029.

Michelmersh has financial scope to raise capacity and make acquisitions to better seize this opportunity.