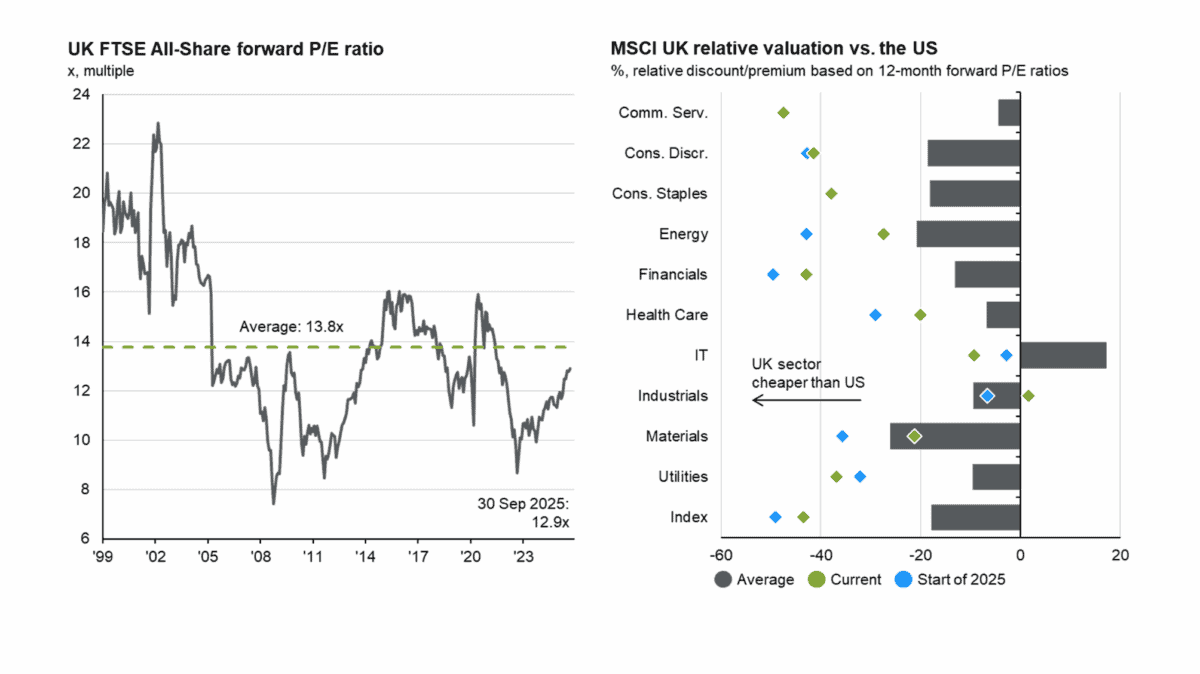

Nearly everyone knows that UK stocks trade at a discount to their US counterparts. That’s true whether we look at the FTSE 100 compared to the S&P 500 or even at valuations in different sectors.

Source: JP Morgan Guide to the Markets UK Q4 2025

Until recently, that hasn’t been much use to investors – UK shares have been relatively cheap, but there hasn’t been any sign that the gap might be set to close. That, however, might be changing.

Growth

By themselves, valuations generally aren’t what cause share prices to move. It’s a cliché that the stock market can stay irrational for longer than investors can stay solvent – but it is true.

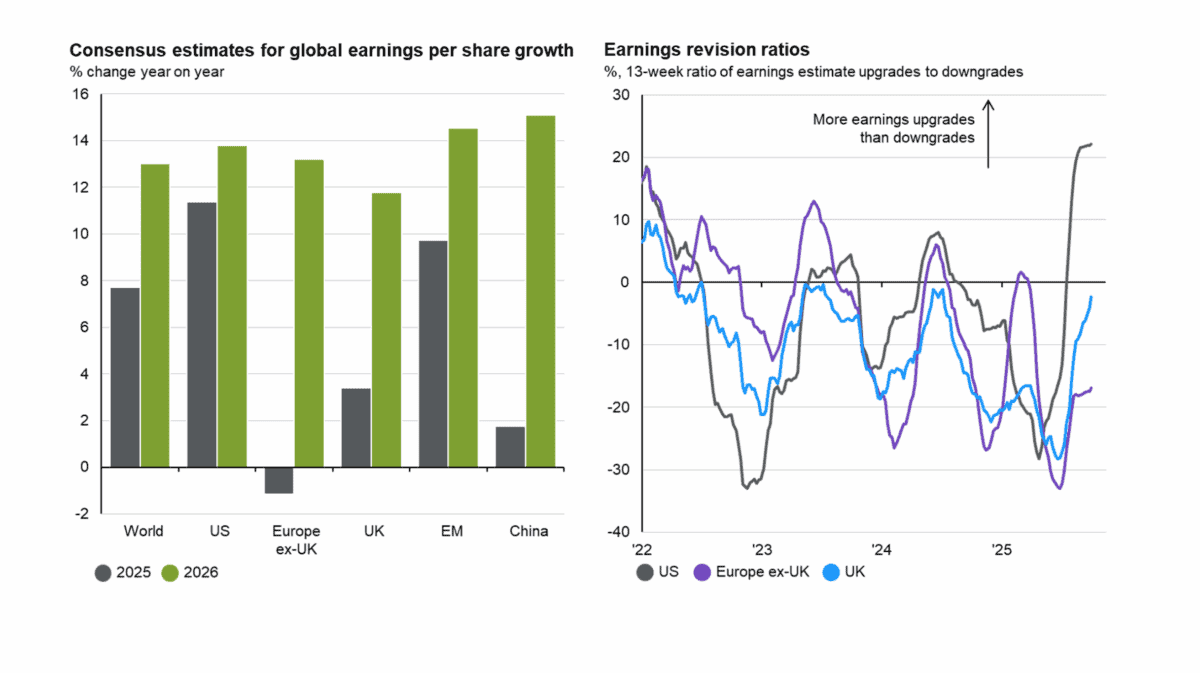

In general, investors need something to bring their attention to cases where equities are trading below where they should be. And earnings growth is often a good candidate for that role.

Source: JP Morgan Guide to the Markets UK Q4 2025

Given this, I think there’s cause for optimism about the outlook for UK shares. According to data from JP Morgan, analysts are expecting UK companies to grow earnings substantially in 2026.

In fact, despite a significant gap in valuations, there isn’t much difference in growth expectations on either side of the Atlantic. And I think that’s a big reason to be bullish on UK stocks.

Packaging

One company that could use an earnings boost is Macfarlane Group (LSE:MACF). The firm both manufactures and distributes packaging to companies.

Earnings have been falling this year, especially on the distribution side of the company. There are a few reasons profits are down, including increased costs and a tough environment for businesses.

A big part of this is energy costs, which are an ongoing concern. The UK’s high electricity prices can weigh on demand for products – and the packages they’re shipped in.

Macfarlane isn’t in a position to do anything about this directly. But it can focus on building a strong competitive position for the long term and it’s been doing a good job of this recently.

Opportunity

I think the most interesting part of Macfarlane’s business is its manufacturing division. This focuses on packaging for items that are difficult to ship and have high replacement costs.

The firm benefits from strong technical expertise and close customer relationships and this creates a barrier to entry for competitors. And this is a key long-term advantage.

At a price-to-earnings (P/E) ratio of 14, the current share price doesn’t really reflect much in the way of growth. So if things pick up in the UK, I think the stock could do very well.

In the meantime, the 4% dividend yield is well-covered by free cash flows. And the company is actively using its excess capital to reduce its share count through buybacks.

Outlook

UK stocks have underperformed their US counterparts for some time. The main reason for this is that earnings growth has been stronger across the Atlantic, but this might be about to change.

Analysts are forecasting a significant lift in UK growth in 2026. And if this happens, I think the current low valuations means there’s a decent chance share prices might follow.

At today’s prices, I think Macfarlane is worth a look. It trades at a relatively low P/E multiple and if earnings pick up across the board, I expect the company to be in the action.