If you’ve held Rightmove (LSE:RMV) since 2009 then you’re probably pretty happy as you are sat on a gain of over 2,500%. However what surprises me most about the rise of the UK’s leading property website is the lack of volatility, the share price has never fallen much below 20% of its new highs in that time. This is highly unusual for a growth stock.

This relative lack of volatility is unusual for growth stocks and I think the fact that the P/E ratio has always hovered around 30 is significant. This ratio is used by a lot of investors, including myself, as the primary valuation tool of a stock. The importance of this ratio is not as a buy or sell signal but as a quick evaluation tool about what you can expect from a stock. My rule of thumb is that 15 or below is a value stock with no, or low growth, 15-30 is a growth stock and 30 or above is a premium reserved for very high growth companies.

What happens if it stops growing?

Rightmove has been sitting where I would expect a quality growth stock to be, and this relates to its consistent earnings growth. However, growth will not last forever and when it slows, I am expecting a revision in the share price as investors move to new opportunities. If the P/E were to fall to around 15, at the bottom end of the growth range, this would be a fall of around 40% from its current P/E of 24.

Why would growth stop?

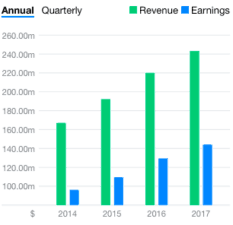

One of the main reasons Rightmove has been so consistent is because market conditions have changed little. The housing market has been strong and the firm has had little competition. You can see from the chart how consistently revenue and earnings have grown, boosted by its near-monopoly on the sector so it could raise its prices without competition.

However in December’s RICS survey on the housing market it describes deteriorating market sentiment and a reduction in sales expectations. Stock levels for estate agents are now sitting near record lows and are reducing further. This suggests we may need to brace for some problems appearing in its results on March 1. The company has embarked on a share buyback programme, generally seen as a sign of management confidence, but seeming confident and being confident are not always the same thing.

Increased competition

More generally I am concerned about how long Rightmove can keep up its astronomically high margins and return on capital. This is normally a good thing, but if they are too high, then it gives competitors a good chance to undercut them. Purplebricks looks like it is struggling to reinvent the property market, but others like Onthemarket are coming after Rightmove’s market share. Onthemarket’s model is centred around getting estate agents on board by undercutting prices and is working as Rightmove’s fees are unpopular among estate agents. The challenger looks unspectacular to me, but if it can gain market share by charging less than the bigger player’s 74% operating margin, it could work.

With virtually every UK estate agent using Rightmove, and new competition that they like more, I think it may be nearing the end of its remarkable growth. There are also unfavourable market conditions that would make me very concerned if I was a shareholder.