A Top Income Share From The Twelfth Magpie

LondonMetric Property

Meet The Quiet Compounding Machine Paying A Growing 6.7% Yield

Last updated: 16/06/2026 | By Zaven Boyrazian, CFA

For the last few years, almost nobody wanted to own commercial property. Rising interest rates, half-empty offices, and a wave of negative headlines turned the whole sector into something investors crossed the street to avoid.

As a consequence, Real Estate Investment Trusts, or REITs, are now treated like damaged goods. And yet, as every experienced investor knows, when sentiment turns sour, that’s when opportunity quietly opens up.

Today you can buy some of the best-run property businesses in Britain for less than the value of the bricks and mortar they own, while collecting a dividend yield that comfortably beats a savings account.

At A Glance:

Type: Cautious

Ticker: LMP

Market: LSE

HQ: London, UK

Industry: Real Estate

Market Cap: £4.35bn

Yield: 6.7%

Year End: 31 March

That gap between the gloomy mood and the underlying reality is exactly where patient income investors can make a lot of money.

So, it shouldn’t be a major surprise that one of our highest conviction income stocks to buy right now is LondonMetric Property (LSE:LMP).

This once niche warehouse operator has drastically evolved over the last few years, leveraging today’s nervous real estate market to buy up weaker rivals and securing more long-term growth at a discount.

The result?

It’s transformed itself into a FTSE 100 titan and one of the largest commercial landlords in the UK with a £7.6bn portfolio that now spans logistics hubs, supermarkets, petrol stations, hotels, hospitals, theme parks, even the AO Manchester Arena.

And for shareholders, it’s translated into 11 years of continuous dividend hikes that are forecast to continue growing. In other words, today’s 6.7% yield could be just the tip of the iceberg.

Why Income Investors Should Care About REITs In 2026

Here’s the simple idea behind every REIT: the company owns property, rents it out, and is legally required to hand most of the rental profit back to shareholders as dividends. In return, it pays little or no corporation tax.

That makes REITs one of the most natural homes for income seekers. You’re essentially becoming a landlord without the leaky taps and tenant phone calls.

So why is the sector so cheap?

The answer is interest rates.

When central banks pushed rates up sharply to fight inflation, two things happened.

- The property in REIT portfolios was revalued lower, because higher rates make future rents worth less today.

- ‘Boring’ assets like bonds and cash suddenly paid a half-decent income again. So, investors no longer needed property to get a yield.

The impact has been money flowing out, share prices falling, and wide discounts starting to materialise.

But step back, and the picture is far more encouraging than the headlines suggest. In fact, rents on the right kind of property like modern warehouses, supermarkets, and healthcare facilities have actually kept rising, often faster than inflation.

Of course, the flare-up of conflict in the Middle East has reminded everyone that energy prices and inflation can stay stubbornly high, which keeps interest rates higher for longer.

That’s uncomfortable for the wider market. But it’s exactly the environment in which a well-financed, inflation-linked landlord can keep growing its rent roll and, in turn, its dividend.

The result for LondonMetric is a rare combination: depressed share prices and rising income.

That’s why the yield is not only high but, crucially, still growing. And most importantly, it’s still covered by genuine cash profits.

Investment Thesis

1. An exceptional dividend track record

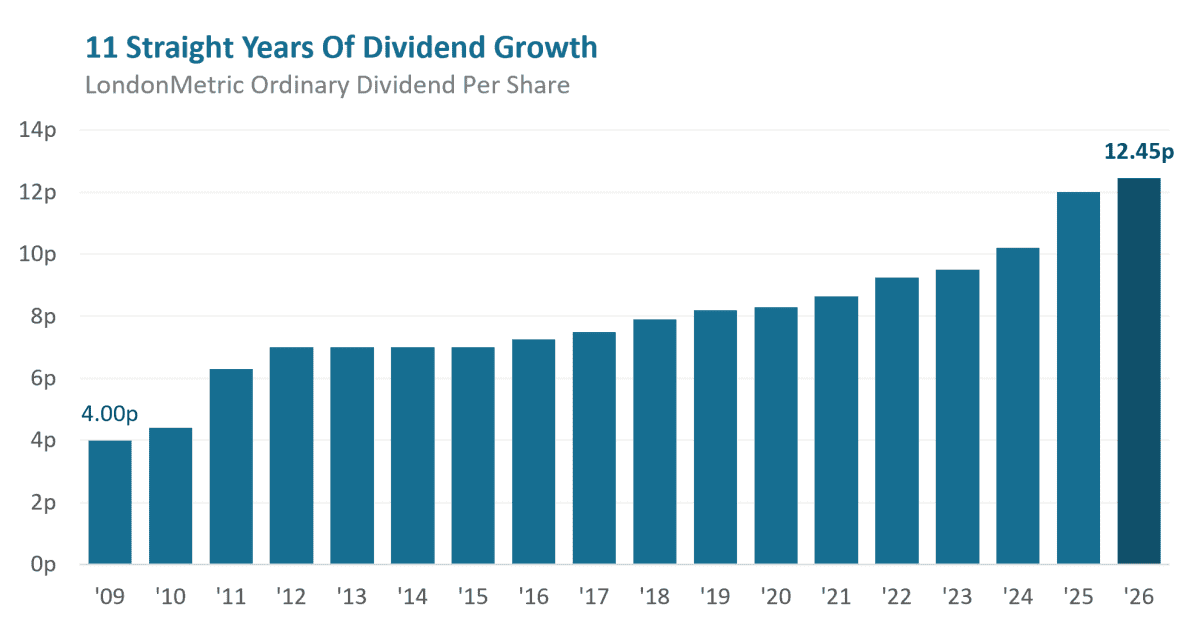

Let me show you the chart that first made us fall in love with this business.

LondonMetric has increased its ordinary dividend every single year for 11 years, lifting it from 4p a share in 2009 to 12.45p today.

Through Brexit, a pandemic, an energy crisis and the sharpest rate rises in a generation, the payout never once went backwards.

That kind of consistency is no accident. It comes from a portfolio designed to throw off reliable, rising rent, and from management’s refusal to promise more than the business can genuinely afford.

2. The ‘Triple Net Lease’ Superpower

Here is the part that really sets LondonMetric apart, and it’s worth understanding because it’s the engine behind everything else.

Most landlords sign leases where they are on the hook for the running costs of a building. That includes repairs, insurance, maintenance, and so on.

LondonMetric does the opposite. It overwhelmingly uses what the industry calls triple net leases, or NNN for short. And under an NNN agreement, the tenants are ultimately responsible for almost all running costs, including insurance, maintenance, repairs, and even property taxes.

For LondonMetric, that means almost all of the rent that’s collected drops straight through to profits, resulting in an industry-leading cost ratio of just 7.7%.

For reference, the wider sector average is closer to 23%. And it means that for every £1 received in rent, approximately 92.3p is pure profit.

It gets even better. Roughly seven in every 10 of those leases come with built-in rent increases either being linked to inflation or fixed annual uplifts.

So, when prices rise across the economy, LondonMetric’s rents rise too, automatically, without the landlord lifting a finger.

And since the average lease still has nearly 17 years to run, with an occupancy level sitting at 97.7%, that gives management exceptional long-term cash flow visibility to plan and expand dividends around.

3. Swallowing The Competition

A cheap sector is bad news if you’re a forced seller. But it’s wonderful news if you’re a strong, well-funded buyer. LondonMetric is firmly in the second camp, and it has become, in its own words, the most active consolidator in the sector.

In the past year alone, it spent around £1.5bn snapping up rivals and portfolios at attractive prices, including a £1.1bn warehousing business (Urban Logistics REIT) and a £48m healthcare-focused company (Highcroft), among others. And it’s not finished.

In June 2026, LondonMetric, alongside Schroder REIT, made an indicative all-share approach for another listed landlord, Picton Property Income, with LondonMetric set to take on a £320m slice of industrial-led assets.

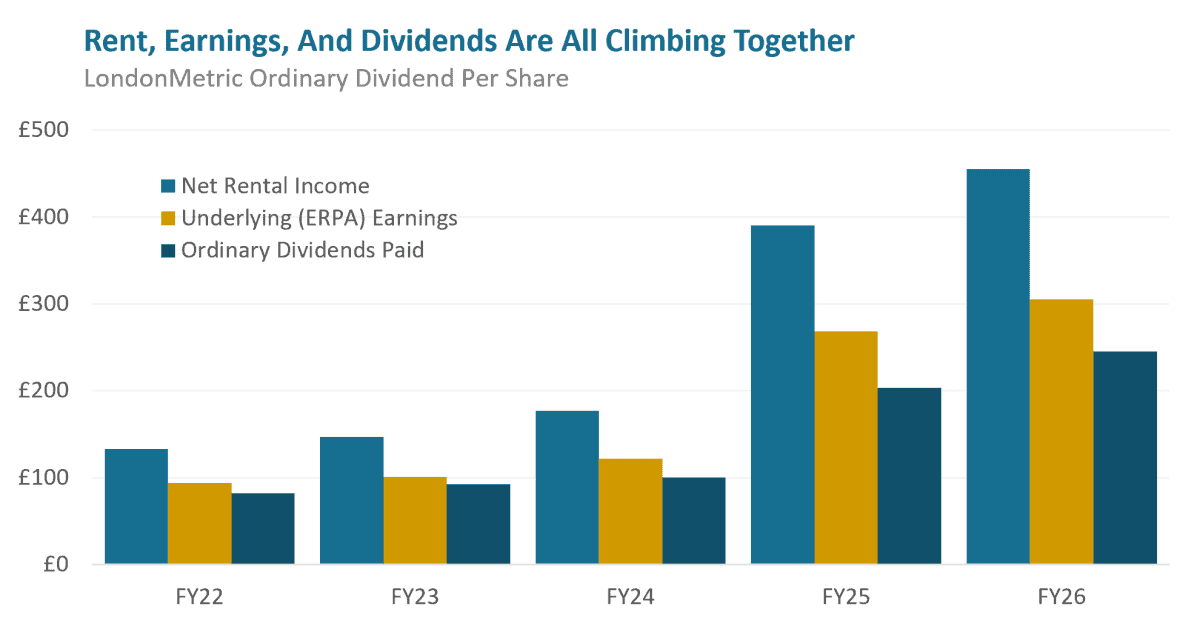

Each acquisition adds more rent, spreads the running costs over a bigger base and, thanks to that ultra-low cost ratio, feeds straight into earnings and dividends.

The chart below shows the flywheel in action: rent, underlying earnings and dividends are all climbing together.

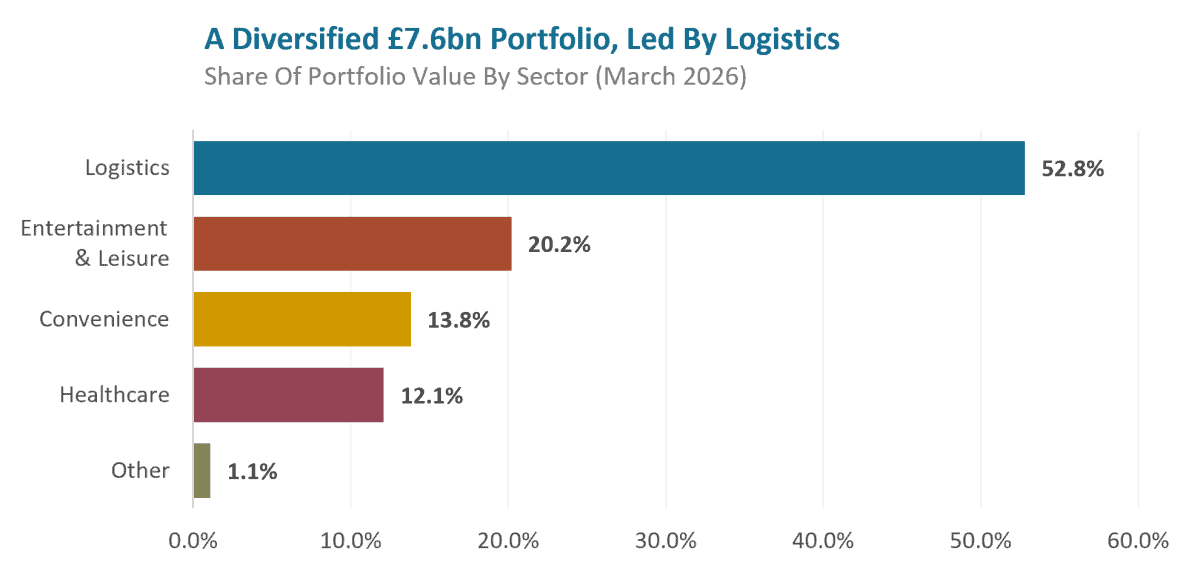

Underpinning all of this is a genuinely diversified portfolio.

Logistics warehouses do the heavy lifting at just over half the £7.6bn estate. But entertainment & leisure venues, convenience & grocery stores, and healthcare buildings provide a handy ballast as well as a roster of blue-chip tenants including the likes of Ramsay Health Care, Merlin Entertainments, Travelodge, Premier Inn, Tesco and Amazon.

Financials & Valuation

| £m (unless stated) | FY22 | FY23 | FY24 | FY25 | FY26 |

| Annual Net Contracted Rent | 143.3 | 145.2 | 339.7 | 340.4 | 432.1 |

| Net Rental Income | 133.1 | 146.8 | 177.1 | 390.6 | 455.3 |

| Underlying (EPRA) Earnings | 93.5 | 101.1 | 121.6 | 268.0 | 305.3 |

| Debt & Equivalents | 1,026 | 1,017 | 2,122 | 2,100 | 2,993 |

| Loan-to-value (LTV) | 28.8% | 32.8% | 33.2% | 32.7% | 36.7% |

| EPRA Earnings Per Share (p) | 10.0 | 10.3 | 10.9 | 13.1 | 13.5 |

| Dividends Per share (p) | 9.25 | 9.5 | 10.2 | 12.0 | 12.45 |

| Dividend Cover | 108.1% | 108.4% | 106.9% | 109.2% | 108.4% |

Over five years, the annual net contracted rent, or rent roll, has more than tripled, from £143m in March 2022 to just over £432m in March 2026, with an obvious step-change in FY24 as a result of a massive merger with LXi REIT.

Since then, rent roll has continued to grow on the back of further bolt-on acquisitions, with another 17% jump in the latest fiscal year, and another jump expected if management’s takeover of Picton Property Income proves successful.

Unsurprisingly, with more rental agreements being signed, the group’s Net Rental Income has followed in lockstep with some slight variations triggered by payment timings.

However, the most crucial number for income investors to watch is Underlying (EPRA) Earnings. This essentially represents the total profit LondonMetric generates from rent and explicitly excludes any non-cash gains or losses caused by fluctuations in property values.

Why does that matter? It reveals just how much income the company is generating from rent that’s available to pay dividends. And in the last five years, it’s surged 226.5% from £93.5m to £305.3m, with margins currently hovering near 67%.

But if LondonMetric’s NNN leasing strategy means it’s not responsible for most operating costs, where is the remaining 33% of its profit margins disappearing? That’s where we need to talk about debt.

Building a real estate empire isn’t a cheap endeavour. And with management being quite acquisitive in recent years to capitalise on discounted property prices, the group has ramped up its borrowing activity, resulting in an ever-increasing interest bill that needs to be paid.

As a consequence, rental profit margins have actually shrunk slightly from around 70% in March 2022. But we’re not too concerned by this.

Sacrificing a few percentage points of profits to deliver a massive expansion of its real estate portfolio seems like a small price to pay. And while the group’s leverage has increased, the Loan-to-Value ratio is still comfortably in manageable territory.

For reference, as a general rule of thumb, a Loan-to-Value ratio below 40% is considered healthy within the world of REITs.

And when looking at the structure of LondonMetric’s borrowings, 99.8% of its outstanding loans have already been hedged against a rise in interest rates.

In other words, if rates rise due to persistent inflation, rental profit margins will suffer a negligible impact.

However, there’s one honest wrinkle worth pointing out, though.

Earnings per share have been growing more slowly than the group’s total earnings. Digging a little deeper, this mismatch stems from LondonMetric issuing new shares as another source of funding for its acquisition spree.

Nevertheless, existing shareholders have still come out ahead, showing that while these acquisitions did cause some dilution, enough value has been created to offset this problem.

Now the bit that should make income investors sit up.

At 185p, LondonMetric Property shares are trading at a 7.8% discount to the group’s net asset value of 200.6p. That effectively translates into spending 92.2p for every £1 of real estate value.

And when looking at the FTSE 100 stock’s price-to-earnings ratio, the business sits at around 13.7 times earnings – a pretty undemanding price tag for a business that’s consistently growing its rent, earnings, and dividends.

This cheap valuation is also a leading reason why the yield is so high at 6.73% today. And with further rental uplifts on the horizon, the current consensus shows that dividends for its 2027 fiscal year are on track to climb even higher to 12.88p, and then 13.37p the following year.

That means, on a forward basis, LondonMetric’s yield is actually closer to 7%. And seeing a 7% yield that’s covered by cash on a stock trading below its asset value is quite a rare set-up.

The Risks & When To Sell

As impressive as we believe LondonMetric Property to be, no investment is ever without risk. And there are some key ones for investors to understand and monitor before considering putting any capital to work.

1. The 2029 Refinancing Wall

As previously mentioned, LondonMetric relies on both debt and equity financing to fund its acquisitions and build out new properties. In 2026, the company was rapidly approaching a debt cliff, where a large chunk of its older debts were maturing.

As a REIT, LondonMetric holds back only a tiny portion of earnings to store as cash on its balance sheet. That means when loans mature, there’s often little capital available to pay off these debts unless the firm commits to selling off assets.

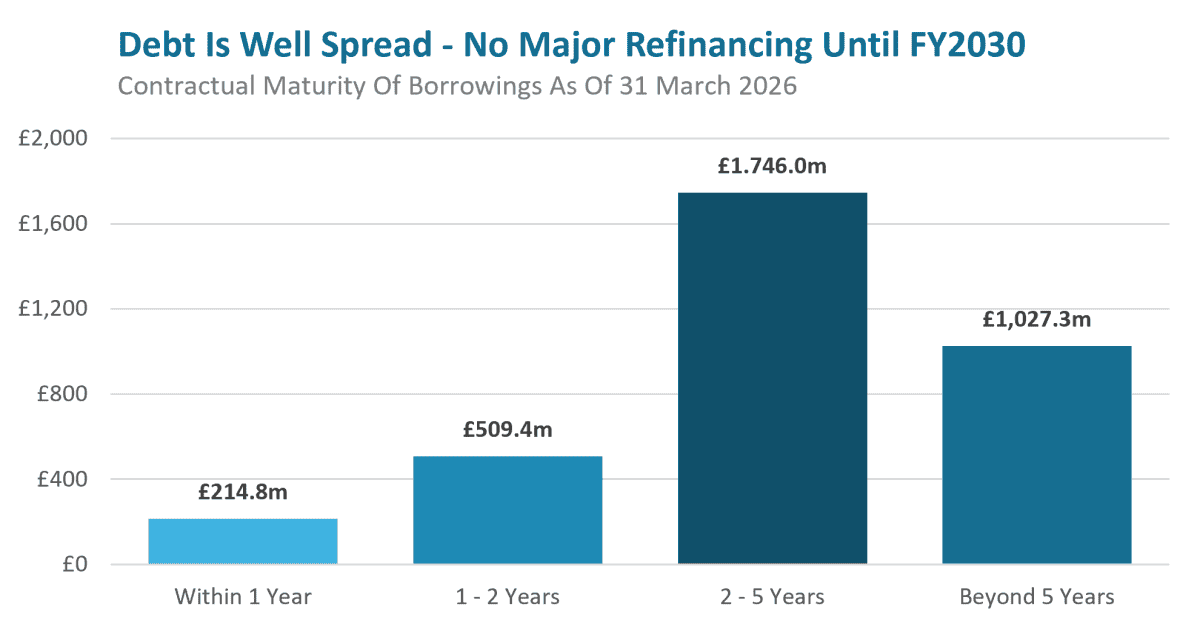

This is where refinancing comes into the picture. By refinancing its debts, management is able to delay debt maturity by several years, giving some valuable financial breathing room. And that’s exactly what the company did earlier this year.

Some £2.7bn of outstanding loans have been refinanced. And now the business doesn’t have to worry about any major debt maturities until as early as 2029.

However, refinancing isn’t a risk-free process. If interest rates are still high by the time another round of refinancing is needed, then the company could have to refinance at a more expensive rate, nudging up its current 4% average cost of debt and eating into the profit available for dividends.

2. Inflation & Energy Prices – A Double-Edged Sword

Inflation helps and hurts LondonMetric at the same time.

On the helpful side, as previously discussed, most of its leases have rent increases linked to inflation, so a hotter economy actually pushes its rents (and dividends) higher.

That triple net lease structure also means tenants, not LondonMetric, absorb rising energy and maintenance bills. And as such, the company is far better insulated than a typical landlord.

The less helpful side is indirect.

Ongoing tensions in the Middle East have pushed energy prices and inflation expectations back up, resulting in a ‘higher for longer’ interest rate environment.

And as we’ve just discussed, if that environment persists into 2029, it could translate into a higher cost of debt following the group’s next expected round of major refinancing.

However, higher rates also weigh on property valuations, which could actively destroy shareholder value if management is forced to make some disposals to raise additional capital.

There’s also a tenant angle: if energy and cost pressures squeeze businesses, expiring leases with LondonMetric may not be renewed, dragging down occupancy rates and, in turn, cash flow.

Given that LondonMetric’s occupancy currently stands at 97.7% and it typically leases predominantly to large-scale industry titans rather than small and medium-sized businesses, the company once again appears well insulated. But crucially, it’s not immune.

3. When To Sell

We recommended LondonMetric Property in Share Advisor for one primary reason: a growing, cash-covered dividend. And if that story starts to break, then that’s the signal to reconsider being a shareholder.

Some key things we’re watching out for are:

- Has dividend coverage fallen below 100%? This would signal that the business is no longer generating enough profit to maintain dividends and is an early warning sign of a potentially looming payout cut.

- Has the Loan-To-Value ratio jumped significantly above 40%? This suggests that management is being too aggressive with its borrowing activity and the resulting interest could apply significant pressure to profit margins.

- Is the company overpaying for growth? Bolt-on acquisitions are proving to be a powerful growth lever for this business. But if management starts to get greedy and begins overpaying to expand its real estate portfolio, this may trigger long-term shareholder value destruction rather than creation.

The Bottom Line

LondonMetric isn’t a get-rich-quick share. Instead, we believe it’s a get-rich-slowly machine for patient long-term investors.

Investors have the opportunity to buy a FTSE 100 landlord at a discount to the value of its property, with an 11-year record of dividend growth, an ultra-efficient business model, and a management team using a fearful market to buy out the competition.

The wider gloom around commercial property has handed patient investors a near-7% yield that’s still growing and comfortably covered by cash. And eventually sentiment will catch up with reality. But until it does, shareholders are getting paid handsomely to wait.

For long-term income investors, I think now is an exciting time to lock in that yield. And it’s not the only passive income opportunity we’ve discovered for our Share Advisor members.

If you’re keen to see all of them, then you can join our premium share-tipping service today with a 33% “welcome” discount off the regular list price.

Once you’re inside, feel free to have a good look around, and if you’re not convinced that we can help you, then just get in touch within your first 30 days and we’ll refund your subscription fee in full. No questions asked!

Happy Investing.

Zaven Boyrazian

Lead Investment Analyst

The Twelfth Magpie

Disclaimer: Zaven Boyrazian owns shares in LondonMetric Property.