Nvidia stock’s arguably better value than many investors realise. At $211, it trades at 23.5 times forward earnings, with that multiple falling to 13.1 times by fiscal 2029 and just 11.2 times by 2031. Advanced Micro Devices is pricier at 75 times this year’s forecast earnings, though that drops to 16.8 times by 2030.

These are the two names that dominate the market for AI accelerators — the chips doing the heavy lifting in the world’s data centres — arguably with the exception of Google‘s TPUs, which are mainly used in-house.

But there’s a third name I’ve been watching: Cerebras Systems (NASDAQ:CBRS).

The scary bit first

On today’s numbers, Cerebras looks wildly expensive. The company’s expected to lose $0.97 per share this year, and the stock trades at 56 times forecast sales. Nvidia, for reference, is on 13 times.

I appreciate figures like these can look scary. But projecting valuations years into the future — and buying before the market catches up — is how the best investors invest. It isn’t just a hunch, it’s about forecasting.

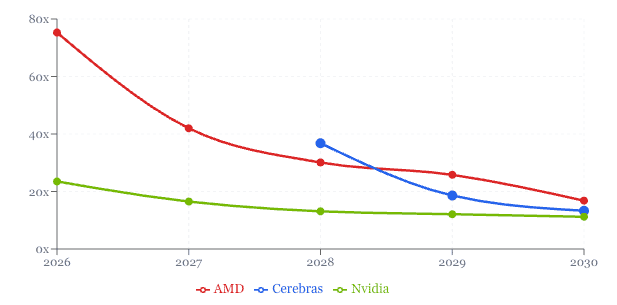

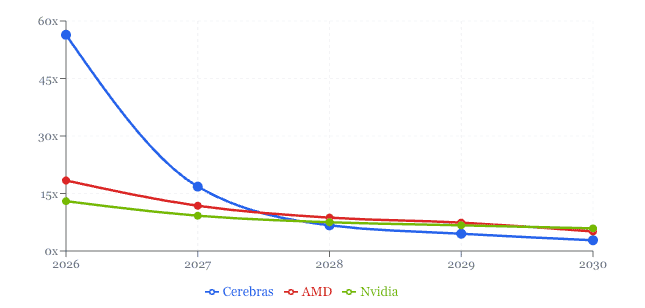

Analysts expect Cerebras’ earnings to explode: $5.84 per share in 2028, $11.54 in 2029, and $16.18 in 2030. At today’s $215 share price, that means the price-to-earnings (P/E) ratio falls from 36.8 times in 2028 to 18.6 times in 2029 and 13.3 times in 2030.

Compare that with AMD at 25.8 times 2029 earnings and 16.8 times 2030 earnings. On these forecasts, Cerebras becomes cheaper than AMD from 2029 — and by 2030 it’s within touching distance of Nvidia. This is just one metric, but it tells us a lot.

The price-to-sales picture is even more striking. Revenue’s forecast to surge from $863m this year to $17.5bn in 2030, dragging the multiple from 56 times down to just 2.8 times — below both Nvidia (5.9) and AMD (5.1) by the end of the decade.

Why I think it can deliver

There’s a narrative behind the numbers — there always is. Cerebras’ wafer-scale chips have carved out a genuine lead in AI inference — actually running models, rather than training them — routinely serving tokens many times faster than GPU-based rivals.

As AI spending shifts from building models to deploying them at scale, that inference lead is exactly where the growth is expected to come from.

The key risk

Here’s the catch, and it’s a big one: every one of those falling multiples is based on growth that hasn’t happened yet. Cerebras needs to grow revenue roughly 20-fold in four years, swing from losses to $16 in earnings per share, and execute flawlessly against two of the best-run companies in semiconductors.

What’s more, only a handful of analysts model beyond 2028, so the further out we look, the shakier the ground. If execution slips, the multiple never falls — and today’s 56 times sales would look very expensive indeed.

That said, I believe it’s a stock investors should consider. AI isn’t going away and I believe this hardware will be integral for decades to come.

Should you invest £5,000 in Cerebras Systems Inc - Class A right now?

When investing expert Mark Rogers and his team have a stock tip, it can pay to listen. After all, the flagship Twelfth Magpie Share Advisor newsletter he has run for nearly a decade has provided thousands of paying members with top stock recommendations from the UK and US markets.

And right now, Mark thinks there are 6 standout stocks that investors should consider buying. Want to see if Cerebras Systems Inc - Class A made the list?

James Fox has position in Alphabet, Cerebras Systems and Nvidia.