When looking for space stocks to buy, all roads seemingly lead to Space Exploration Technologies. Given its industry-leading position and all the attention it gets (including here), that’s hardly surprising.

But the global space economy is projected to reach between $850bn and $1.8trn inside a decade, according to various forecasts. So there is plenty of growth opportunities in this space (pardon the pun).

Here, I want to highlight two stocks that might be worth considering for an ISA portfolio. Each has sold off heavily recently.

Down 50%

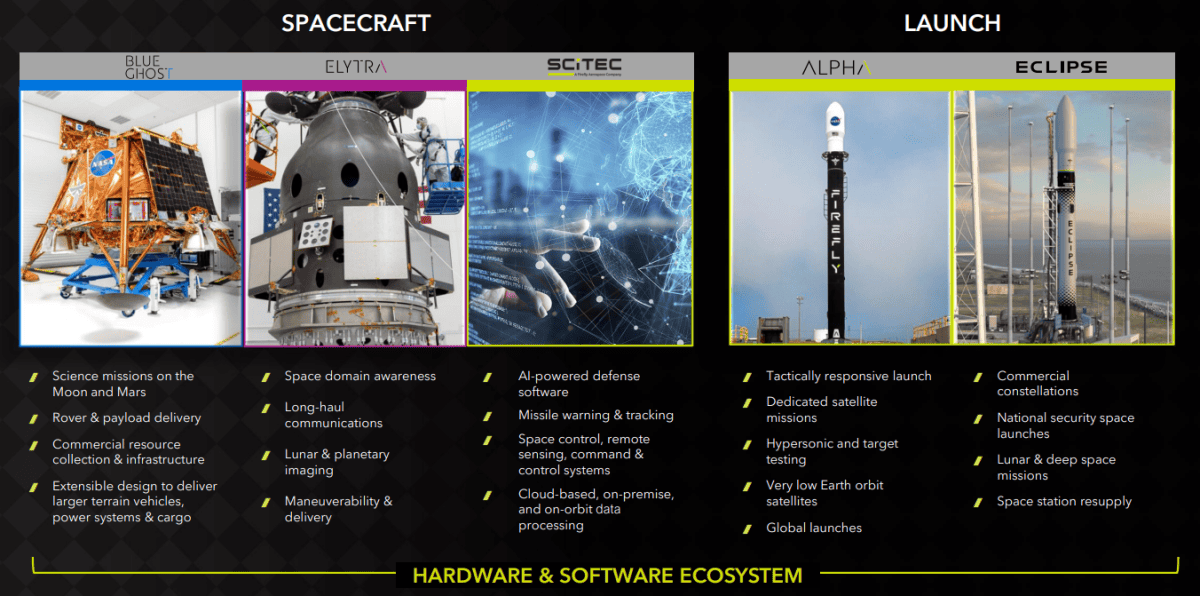

Firefly Aerospace (NASDAQ:FLY) builds rockets and lunar landers. Last year, it became the first commercial company to accomplish a soft landing on the Moon (landing the right way up, at least) with its Blue Ghost spacecraft.

NASA was so impressed that it awarded Firefly a $75m subcontract to deliver four drones to the Moon’s South Pole to support the agency’s Artemis Moon Base initiatives. In June, it got a larger $144m contract to deliver a rapid mission to the Moon.

The company’s Alpha rocket has done seven launches so far, to varying degrees of success (March’s was a success). Defence giant Lockheed Martin is an anchor customer, with up to 25 flights booked running through to 2029.

Firefly and Northrop Grumman are also co-developing Eclipse, a medium-lift launch vehicle capable of carrying much larger payloads. The first test flight is scheduled for 2027.

Turning to financials, revenue is expected to soar around 175% to $440m this year. And Wall Street analysts see revenue exceeding $1bn by 2028, indicating that this is a high-growth company.

However, loss-making Firefly is incinerating around $300m a year in cash as it scales up. So it might need to dilute investors to raise more capital in future (it ended Q1 with $551m in cash).

Indeed, the stock has slumped 50% since May, largely due to a capital raise of around $192m.

Still, from a modest market cap of just $4bn today, Firefly could generate strong returns over the next few years. But there’s a lot of execution risk with the rocket launches, making this a high-risk, high-reward stock.

Down 40%

HawkEye 360 (NYSE:HAWK) only went public in May, but it’s been a baptism of fire, with the stock falling around 40% since.

Partly this has been due to the sell-off in space-related stocks, which has taken SpaceX down almost 30% since mid-June.

HawkEye doesn’t build rockets or lunar landings. Instead, it operates a constellation of over 30 satellites that track and analyse radio frequency signals.

This has a number of uses for defence and intelligence customers:

- Detection of vessels engaged in smuggling or illegal fishing

- Track dark vessels

- Air defence monitoring

HawkEye’s products related to these areas are driving robust growth, with revenue expected to jump 82% to $213m this year. Analysts anticipate the top line growing to roughly $329m by 2028, with profits throughout.

A risk I see here is customer concentration, with a small handful of defence customers accounting for the majority of revenue. Delays in government contract awards is a possibility here.

However, the company appears to be in the sweet spot as the US and Europe prioritise electronic and drone warfare and space-based surveillance. HawkEye’s market cap is just $1.9bn.

Should you invest £5,000 in Firefly Aerospace right now?

When investing expert Mark Rogers and his team have a stock tip, it can pay to listen. After all, the flagship Twelfth Magpie Share Advisor newsletter he has run for nearly a decade has provided thousands of paying members with top stock recommendations from the UK and US markets.

And right now, Mark thinks there are 6 standout stocks that investors should consider buying. Want to see if Firefly Aerospace made the list?

Ben McPoland has no position in any of the companies mentioned.