South Korean memory chip powerhouse SK Hynix (NASDAQ: SKHY) is about to list on the Nasdaq. On 10 July, it will launch American Depositary Receipts (ADRs) on the US exchange.

Should I buy the stock for my ISA? Or are there better opportunities out there?

An introduction to SK Hynix

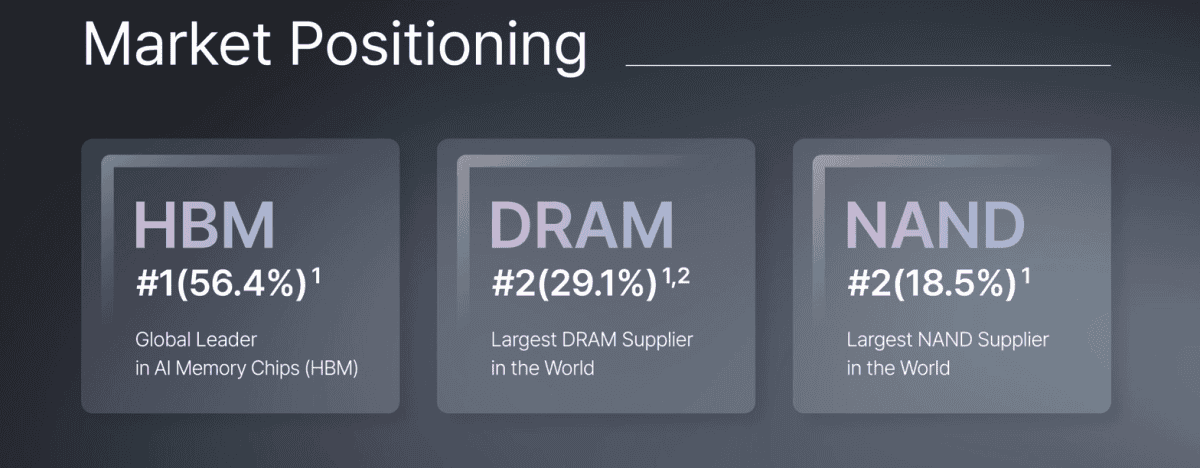

A manufacturer of DRAM and NAND products, SK Hynix is one of largest memory chip companies in the world. Along with Samsung and Micron, it’s part of the ‘Big Three’ that dominates global memory production.

Where it has an edge is High Bandwidth Memory (HBM), which is used in AI chips made by the likes of Nvidia. It made aggressive bets on HBM early on and as a result, it has a 55%-60% market share here today.

Huge growth

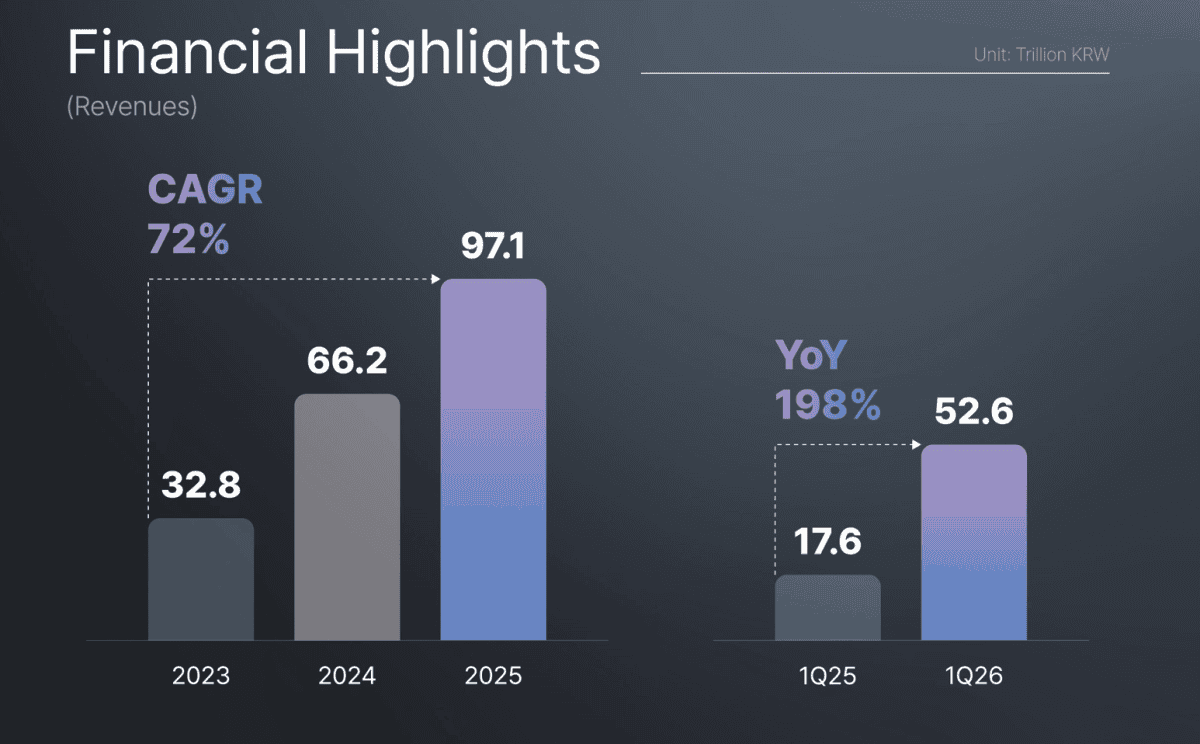

Given that demand for HBM’s sky-high right now, and the company has pricing power, it’s seeing strong growth. In Q1, revenue came in at KRW 52,576bn, up 198% year on year.

“As memory becomes increasingly critical in AI computing, demand for high-performance memory is surging while supply remains constrained, expect favourable pricing environment to continue for the time being”.

SK Hynix Q1 results

Growth isn’t the only thing to like about this business as it’s also very profitable. In Q1, net profit was up a whopping 398% to KRW 40,346bn.

In terms of valuation, it looks attractive. With analysts forecasting earnings per share of KRW 315,000 this year, the forward-looking price-to-earnings (P/E) ratio’s only about eight.

Up 800% in a year!

On the downside, the stock’s up about 800% over the last year. I’m not a big fan of buying after surges like this as there are often big pullbacks.

Another issue is that in the past, demand for memory has been extremely cyclical. Things could be changing here due to the AI boom and the fact that memory companies are signing longer-term contracts with buyers. But at this stage, we can’t rule out another memory slowdown in the years ahead.

It’s worth noting that if demand did slow, SK Hynix’s earnings could take a big hit. In this scenario, the stock obviously wouldn’t look so cheap.

A better chip stock?

Given the 800% gain in SK Hynix over the last year, I can’t help but feel there are better chip stocks to be buying for my portfolio at the moment. Broadcom’s (NASDAQ: AVGO) an example.

It’s also growing at a spectacular rate. Last quarter, AI revenue grew 143% year on year while total revenue was up 48%.

Meanwhile, it also has an attractive valuation. Looking at earnings forecasts for the financial year starting in November, the P/E ratio is under 20.

Unlike SK Hynix however, there’s not a lot of hype around the name. In fact, it’s a little out of favour (down about 20% from recent highs).

Over the last year, it’s ‘only’ up about 40%. I’m a lot more comfortable buying after that kind of rise versus buying after a 800% hyper-gain.

Of course, it faces some of the same risks as SK Hynix. If the AI boom stalls, demand for Broadcom’s chips could slow.

Overall though, I like the risk/reward skew. I’ve been building a position in this stock recently and will continue to buy while it’s down.

Should you invest £5,000 in Broadcom right now?

When investing expert Mark Rogers and his team have a stock tip, it can pay to listen. After all, the flagship Twelfth Magpie Share Advisor newsletter he has run for nearly a decade has provided thousands of paying members with top stock recommendations from the UK and US markets.

And right now, Mark thinks there are 6 standout stocks that investors should consider buying. Want to see if Broadcom made the list?

Edward Sheldon owns shares in Broadcom, Nvidia, and Nasdaq