Most people assume a pay rise is the best way to improve their finances. Earn more from work, and everything else takes care of itself.

But a growing number of investors are focusing on something different: building a second income.

The appeal is not necessarily about replacing a salary altogether. Instead, it’s about creating an additional source of cash that can supplement earnings and provide greater financial flexibility over time.

That raises an interesting question: could building a second income ultimately prove more valuable than chasing the next pay rise?

A second income doesn’t need to replace your salary

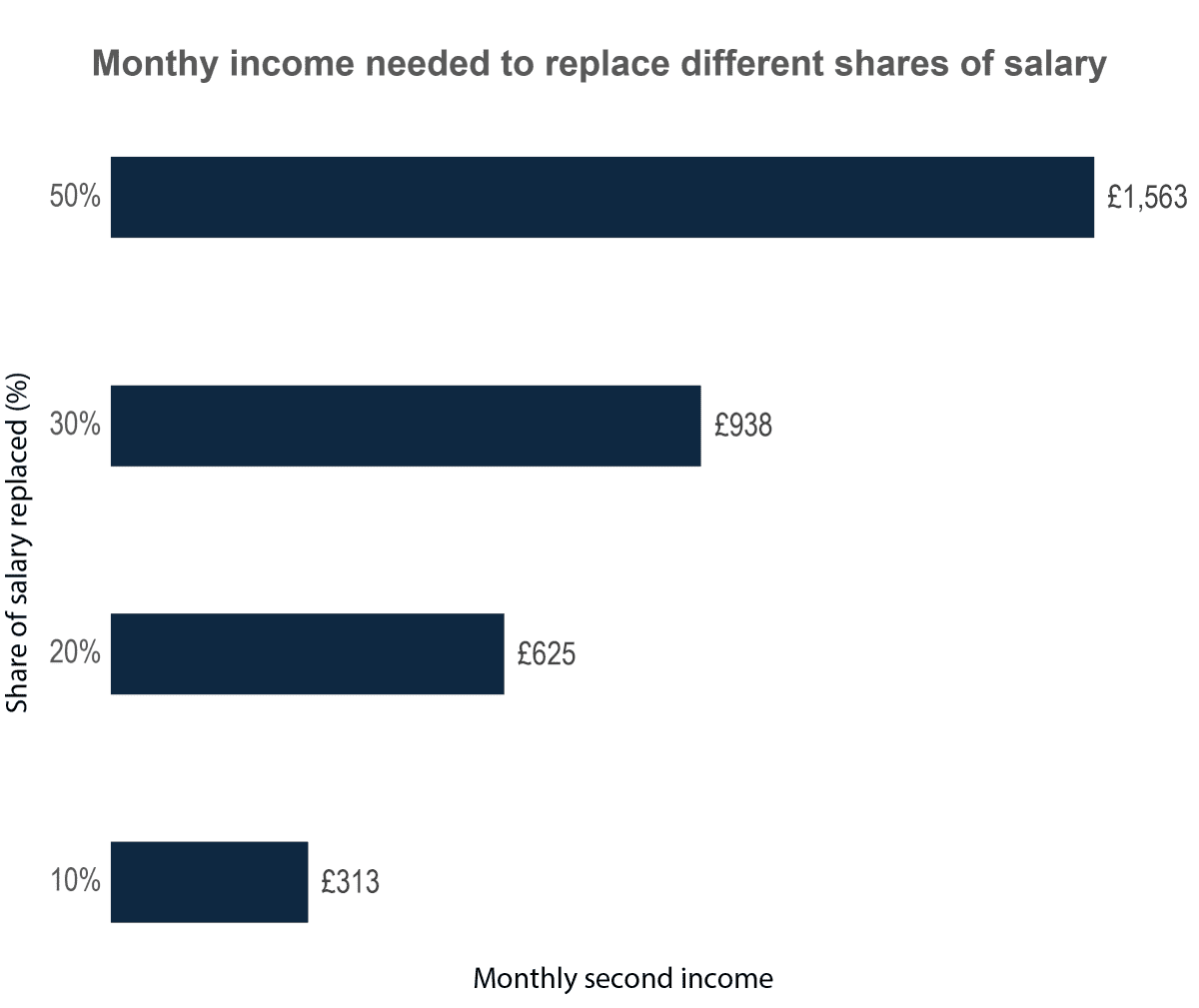

When people think about building a second income, they often imagine replacing their entire wage. That assumption can make the goal feel unrealistic.

The chart below tells a different story. Even replacing a relatively small proportion of earnings can create an additional stream of income that helps cover household bills, build savings, or provide a financial buffer during periods of uncertainty.

What stands out is how achievable the numbers appear. Replacing 10% of a £37,500 salary requires just over £300 a month. Doubling that to 20% requires around £625.

For many investors, that shifts the conversation. A second income does not need to be large enough to make work optional before it becomes valuable. Even a modest amount can increase financial flexibility and reduce the pressure that comes from relying entirely on a single source of earnings.

Chart generated by author

Compounding machine

RELX (LSE: REL) has long been viewed as one of the FTSE 100’s classic compounders. A steady business model, strong margins, and consistent earnings growth have helped build that reputation over time.

That’s reflected in the dividend profile. Rather than relying on a high starting yield, it has delivered steady dividend growth for years, supported by recurring revenue from subscriptions and data-driven services.

More recently, however, the share price has come under pressure as investors reassess the impact of artificial intelligence on its business model.

The concern is straightforward. If AI tools can increasingly summarise, search, and generate legal and scientific information, could they weaken pricing power or reduce the need for specialist data platforms?

At first glance, that looks like a credible risk. Law firms and corporate clients are already experimenting with AI tools that streamline parts of research and workflow processes.

But that argument tends to overlook how embedded RELX is in practice. Its customers typically use multiple systems at the same time, depending on jurisdiction, task, and regulatory need. In that environment, AI tools are more likely to sit alongside existing platforms rather than replace them.

The core value still comes from curated, verified, and continuously updated proprietary data. That isn’t easily replicated by general-purpose AI models, particularly in regulated industries.

For me, this looks less like a disruption story and more like a transition in how information is accessed rather than who owns it.

Bottom line

In that sense, RELX fits the idea of a second income stock quite well. It’s not about a high yield today, but about steady, compounding income growth over time.

On that basis, I think it remains one for long-term income investors to consider.

Should you invest £5,000 in RELX right now?

When investing expert Mark Rogers and his team have a stock tip, it can pay to listen. After all, the flagship Twelfth Magpie Share Advisor newsletter he has run for nearly a decade has provided thousands of paying members with top stock recommendations from the UK and US markets.

And right now, Mark thinks there are 6 standout stocks that investors should consider buying. Want to see if RELX made the list?

Andrew Mackie owns shares in Relx.