Most ISA investors assume more passive income is always better. But there may be a point where that approach starts to work against them.

The issue is that higher income often comes at a cost. To reach those levels, investors typically move further into concentrated high-yield stocks, which can reduce diversification and weaken overall ISA portfolio quality. Over time, that can make income less stable than it initially appears.

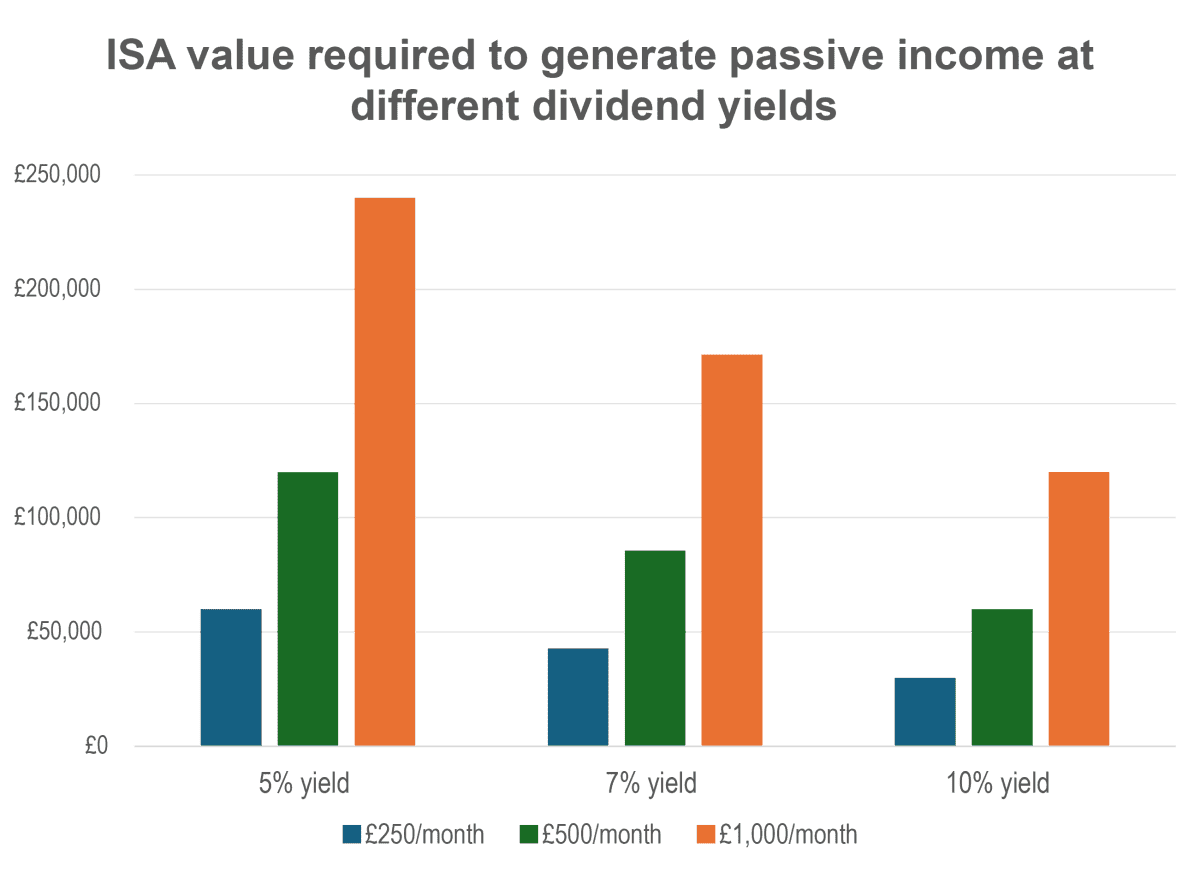

The hidden trade-off behind higher passive income

The chart below shows how much capital an ISA investor would need to generate different levels of monthly passive income, depending on the dividend yield achieved.

What stands out is not just the amount of capital required. It’s the trade-off embedded in the assumptions. Investors can either target higher levels of income or maintain a higher-quality, lower-yield portfolio. In practice, doing both is often difficult.

To generate more passive income from a smaller portfolio, investors typically need to move further up the yield spectrum. That can mean owning slower-growing businesses, accepting greater risk, or concentrating more heavily in a handful of sectors.

This is the point many ISA investors overlook. A focus on maximising monthly income can gradually reshape a portfolio in ways that are not immediately obvious. Higher yields may boost income today, but they can come at the expense of diversification and long-term growth.

Chart generated by author

Income without chasing yield

For investors seeking passive income, I think Aviva (LSE: AV.) is worth considering.

At first glance, a 6.1% trailing yield may not look especially exciting compared to some of the double-digit yields available elsewhere in the FTSE 350. But that is partly the point.

Rather than stretching for the highest possible payout, I prefer businesses that can steadily grow their distributions over time. In Aviva’s case, management recently increased its dividend target, aiming for mid-single-digit growth.

It also recently reintroduced share buybacks after they were suspended following the acquisition of Direct Line. This year it has launched a £350m buyback programme.

What gives me confidence is the cash generation underpinning these returns.

The insurer now expects to generate more than £7bn of cumulative cash remittances by 2028, providing substantial support for future dividends. Management has already delivered several medium-term targets ahead of schedule, suggesting the business has some financial flexibility.

Risks

There are risks, however. Insurance may be more defensive than many industries, but it remains a cyclical industry. During periods of weaker economic activity, demand can soften, investment returns can come under pressure, and claims costs can become more difficult to predict.

Investors should also remember that dividends are never guaranteed. Aviva cut its payout during the pandemic as management sought to strengthen the balance sheet and reset the business. While today’s company is arguably in much better shape, that episode highlights how even established income shares can disappoint when conditions deteriorate.

For me, though, the investment case remains compelling. The yield is attractive without being excessive, dividend growth is firmly embedded in management’s plans, and cash generation appears strong enough to support future shareholder returns. For investors seeking a balance between income today and income growth tomorrow, I think Aviva is one to consider.

Should you invest £5,000 in Aviva Plc right now?

When investing expert Mark Rogers and his team have a stock tip, it can pay to listen. After all, the flagship Twelfth Magpie Share Advisor newsletter he has run for nearly a decade has provided thousands of paying members with top stock recommendations from the UK and US markets.

And right now, Mark thinks there are 6 standout stocks that investors should consider buying. Want to see if Aviva Plc made the list?

Andrew Mackie owns shares in Aviva.