Dividend investors often avoid shares in pharmaceutical companies. And with good reason – they’re genuinely complicated businesses.

One of the biggest names in the industry however, currently comes with a 6.6% yield. So could the rewards be worth the risks?

Investing in drug companies

Pharmaceutical companies operate on a cycle:

- Invest in discovering and developing new medicines.

- Secure regulatory approval for the ones that work.

- Charge premium prices until patents expire.

- Repeat.

In rough terms, the average cost of bringing a drug to market is $1.3bn, less than 10% make it from Phase 1 testing to approval, and patent protection lasts around 20 years.

The difficulty for non-specialists is figuring out which drugs will succeed. It’s like predicting the winner of the World Cup (the poker one, not the football one).

None of this makes the industry uninvestable. But the rewards need to be big enough to justify the inherent risks that come with unpredictability.

A fallen giant

I sometimes ask my students what they think the most important development of the last 10 years was. A lot of them go for the Covid-19 vaccine.

Despite this, shares in Pfizer (NYSE:PFE) are more than 57% off their 2021 highs. And there are a few reasons for this.

One is that Covid-19 vaccine sales have dried up. Revenues from that product have gone from $100bn a year to a fraction of that today.

Another is that several patents are set to expire by 2028. Collectively, Eliquis (blood thinner), Ibrance (breast cancer), and Xeljanz (arthritis) make up a third of the current revenue base.

The third is a recent acquisition. Pfizer paid $43bn for Seagen – an oncology specialist – and that’s resulted in some high debt levels.

All of that means the dividend cover is getting pretty tight. But reports of this company’s death might have been greatly exaggerated.

A closer look

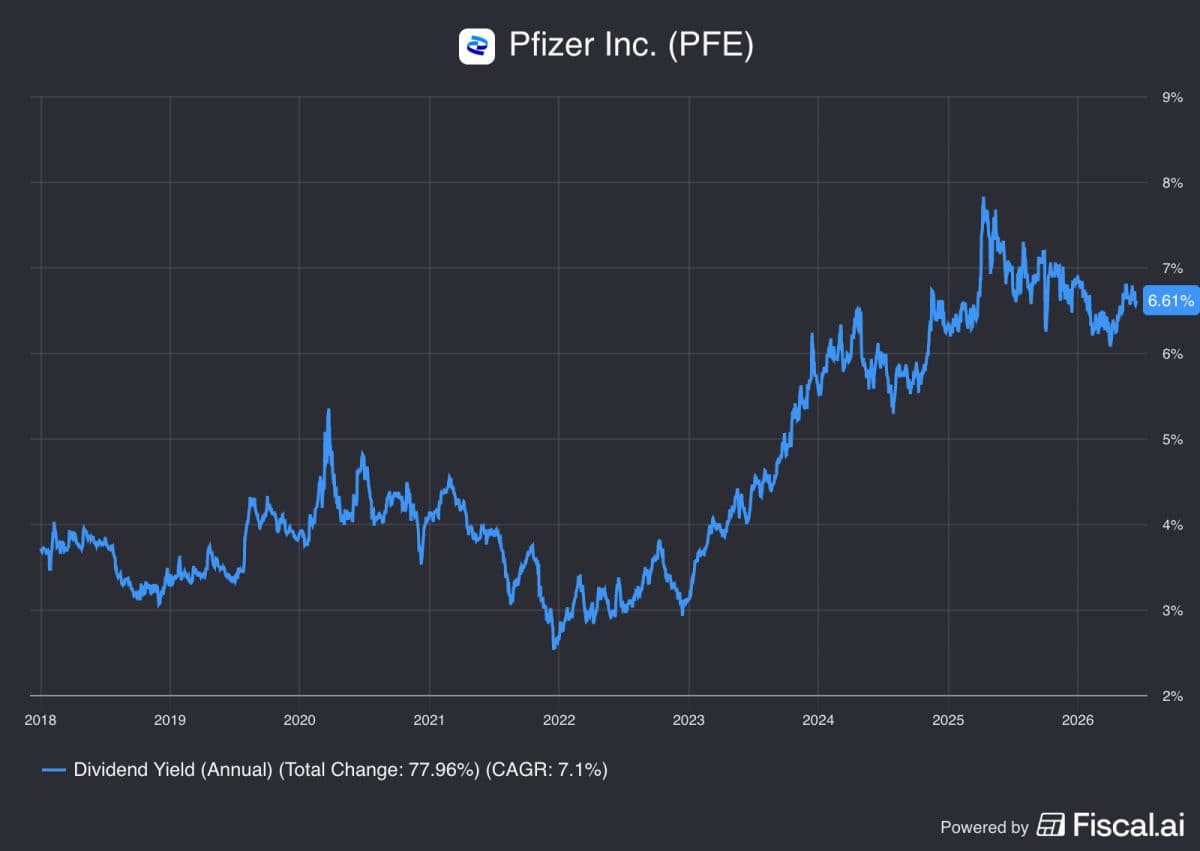

Looking at the numbers, Pfizer’s unusually cheap for a company of its quality. The 6.6% yield is strangely high and the firm has real structural advantages.

Source: Fiscal.ai

It has one of the industry’s largest manufacturing networks and that’s a big advantage that can give any drug an instant worldwide reach.

The Seagen acquisition has also given it a leading platform in known as antibody-drug conjugates (ADCs). These are a more targeted cancer treatment than chemotherapy.

Pfizer’s pipeline also has a lot of potential. It includes a Phase 3 lung cancer treatment, a replacement breast cancer drug, and a monthly obesity injectable. The last of these is particularly interesting. The firm has faltered in the GLP-1 market, but it’s optimistic about launching a meaningful competitor to Eli Lilly and Novo Nordisk.

The verdict

A lot of investors think that pharmaceuticals are outside their circle of competence. That’s fair enough – it’s hard to weigh the strength of one drug pipeline against another.

The same investors however, are more than happy to buy semiconductor companies. And I’m not sure there’s anything less technical about the processes involved there.

Pfizer isn’t straightforward, by any means. But it has a world-class manufacturing platform and a pipeline that could have genuine blockbuster potential.

Add in a 6.6% dividend yield and the stock might be a rare opportunity for dividend investors. I think it’s absolutely worth a closer look.

Should you invest £5,000 in Pfizer right now?

When investing expert Mark Rogers and his team have a stock tip, it can pay to listen. After all, the flagship Twelfth Magpie Share Advisor newsletter he has run for nearly a decade has provided thousands of paying members with top stock recommendations from the UK and US markets.

And right now, Mark thinks there are 6 standout stocks that investors should consider buying. Want to see if Pfizer made the list?

Stephen Wright has no shares in any of the companies mentioned.