Looking at out-of-favour UK stocks isn’t exciting or glamorous. But I think it can be a great source of potential opportunities for long-term investors.

While everyone else is trying to figure out whether – or how – to buy SpaceX shares, the real opportunities might be closer to home.

Home improvement

Housing and home improvement companies are about as fashionable as a 1970s avocado bathroom suite. And investors got a brutal reminder of that this week.

DIY giant Homebase fell into administration. Weighed down by debt and weak demand, its final stores have ceased trading.

There’s nothing fun about a major corporate collapse. But the cold reality of capitalism means the home improvement industry is now less competitive.

When a major operator vanishes, its market share doesn’t evaporate. It gets redistributed among the surviving businesses.

It’s unemotionally Darwinian, but it’s the way things are. And this kind of thing can create opportunities for investors.

A differentiated business

Enter Howden Joinery Group (LSE:HWDN). The company sells home improvement supplies – including the kitchen sink.

Importantly, though, the firm isn’t another Homebase. It’s almost entirely focused on trade customers, not DIY enthusiasts or weekend warriors.

If someone in my house wants a new kitchen cabinet hinge, we go to a DIY store. Then we get confused, buy the wrong thing, and get someone else to sort it.

When proper builders want to buy something, they go to Howden. And that’s a big advantage for the FTSE 100 retailer for a couple of reasons:

- Tradespeople come back more often than DIY customers, creating better repeat business.

- Professionals don’t need expensive showrooms – Howden’s can operate out of low-cost warehouses.

That makes Howden fundamentally different from something like Homebase. But the stock market seems to be lumping them in together.

Going cheap

Shares in Howden Joinery Group are trading at a price-to-earnings (P/E) multiple of just 16. But that doesn’t tell the full story.

The industry is very cyclical. That means earnings are unusually high or unusually low a lot of the time, which distorts this ratio.

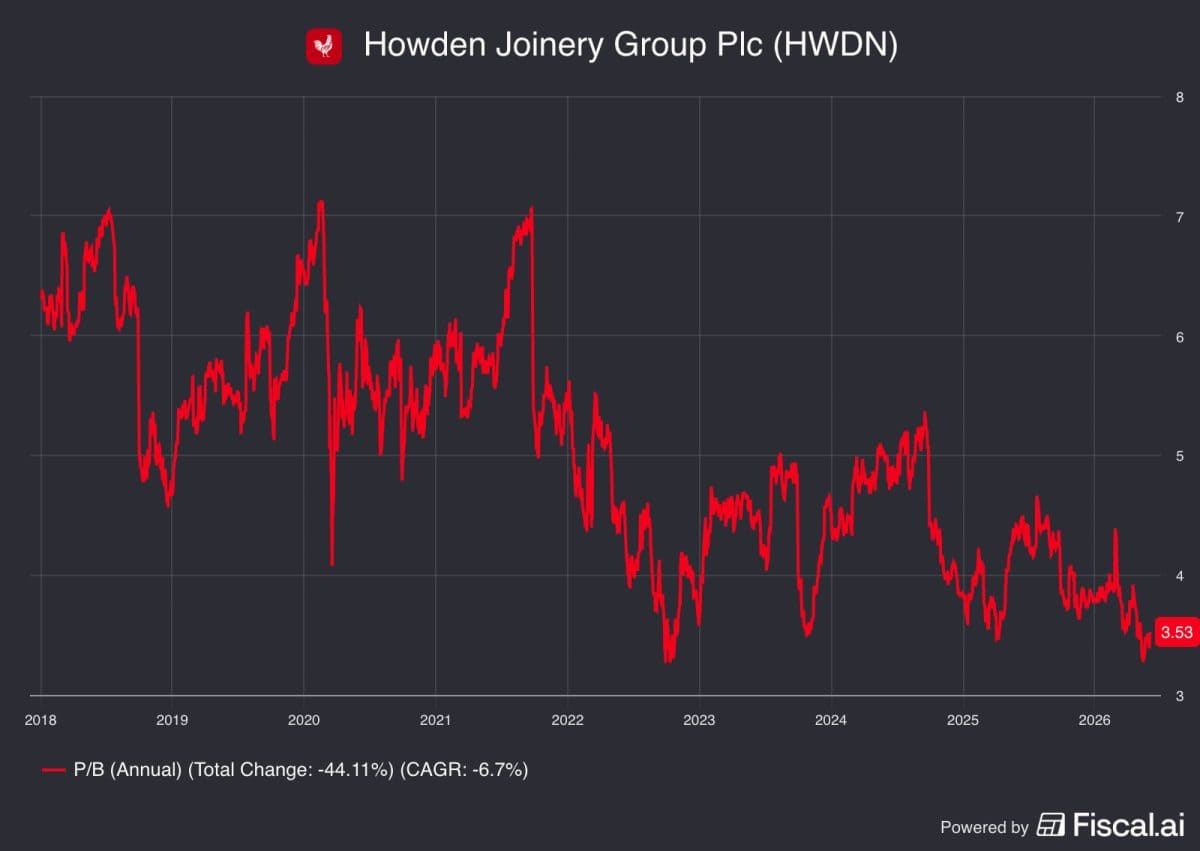

In these cases, I think the price-to-book (P/B) multiple is a good one to use. A cyclical firm’s book value is typically much less volatile than its earnings.

Source: Fiscal.ai

On this basis, Howden is unusually cheap at the moment. And that suggests to me that it’s worth taking a look right now.

The company isn’t immune from the effects of a downturn in the home improvement market. But I think it’s in a better position than most of its rivals.

Time to buy?

Can Howden’s shares go lower from their current levels? Yes – it’s entirely possible that things get worse before they get better.

The market for home improvements can stay depressed. And in that situation, all the company – and its shareholders – can do is wait.

Importantly, though, this isn’t a struggling retailer trying to convince homeowners to paint their spare bedrooms. It’s a trade-only logistics machine with a real cost advantage.

The stock market is focused on other things right now and that’s fine. But for long-term investors, this might be the place to look.