Many investors underestimate what a Stocks and Shares ISA is capable of over the long term. Because the amounts involved can feel small at first, it’s easy to assume they are not enough to build meaningful wealth.

That often leads to a second belief — that serious outcomes only come from either large lump sums or consistently maxing out ISA allowances every year.

But is that really how long-term wealth is actually built?

Lump sum vs contributions

To test how wealth is actually built inside a Stocks and Shares ISA, I modelled a simple long-term scenario.

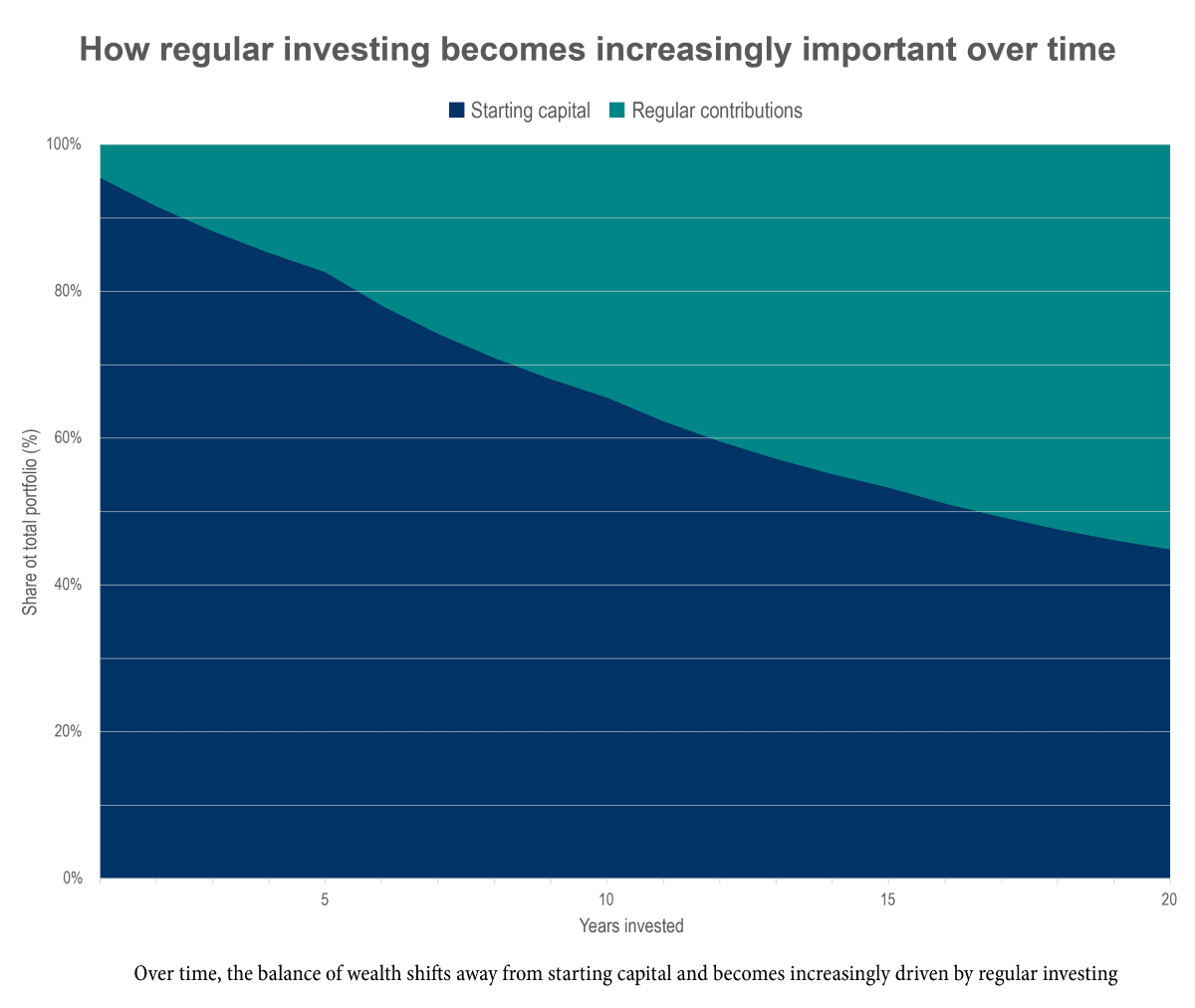

It assumes an investor starts with a £40,000 lump sum, alongside annual contributions that rise over time. The contributions start at £2,000 in the early years to £8,000 later, reflecting a typical earnings path.

The chart below shows how starting capital and ongoing contributions evolve over 20 years, assuming a 6% annual return.

At first, the result is heavily skewed towards the lump sum. In the early years, it accounts for more than 95% of total portfolio value — simply because it has more time to compound.

But that balance does not stay static.

As time passes, regular contributions build up and earlier payments begin compounding themselves. The structure of wealth gradually shifts.

By the later stages, the majority of total portfolio value is no longer coming from the initial lump sum. Instead, it’s driven by consistent investing and the compounding of those additions.

What starts as a story about starting capital becomes a story about consistent, disciplined investing over time.

Chart generated by author

Quality compounder

To reach higher long-term ISA return assumptions, investors need to find businesses capable of compounding steadily through cycles rather than relying on short-term earnings swings.

That is why Experian (LSE: EXPN) stands out to me.

FY26 was another record year, with organic revenue growth of 8% and earnings per share up 15%.

But the more important point is consistency. This is the second consecutive year the group has delivered against its medium-term framework, with margins also ahead of expectations as scale and cloud migration benefits continue to flow through.

Diversified model

The real attraction is the underlying business model.

Experian sits at the centre of global credit, fraud, and identity decisioning. Its proprietary data is deeply embedded into customer workflows, making it difficult to displace once integrated. That supports high renewal rates and continued wins across North America, Brazil, and the UK.

Strategically, the business is entering a more powerful phase. Cloud migration is largely complete, improving flexibility, while AI is being embedded into products and platforms. Management estimates more than $15bn of incremental opportunity from these capabilities, spanning credit analytics, fraud detection, and healthcare applications.

This is not just efficiency-led technology adoption. It is expanding the number of use cases where Experian’s data becomes essential to decision-making.

The main risk is valuation and expectations. With strong execution already priced in, any slowdown in growth or disruption to client demand could quickly reset sentiment.

Even so, the combination of sticky data, long-term contracts, and expanding platform use creates a compounding profile that’s difficult to replicate. But it is by no means the only long-term compounder on my radar.

Should you invest £5,000 in Experian Plc right now?

When investing expert Mark Rogers and his team have a stock tip, it can pay to listen. After all, the flagship Twelfth Magpie Share Advisor newsletter he has run for nearly a decade has provided thousands of paying members with top stock recommendations from the UK and US markets.

And right now, Mark thinks there are 6 standout stocks that investors should consider buying. Want to see if Experian Plc made the list?

Andrew Mackie owns shares in Experian.