Most people think of a Stocks and Shares ISA as a way to supplement their income. But what if it could replace it entirely?

According to the latest figures from the Office for National Statistics, average full-time weekly earnings stand at £766. That works out at roughly £3,064 a month.

Generating that level of income from investments is possible. The question is how large an ISA would need to be to make it happen.

The income target in context

Replacing a monthly salary of £3,064 requires annual income of £36,768.

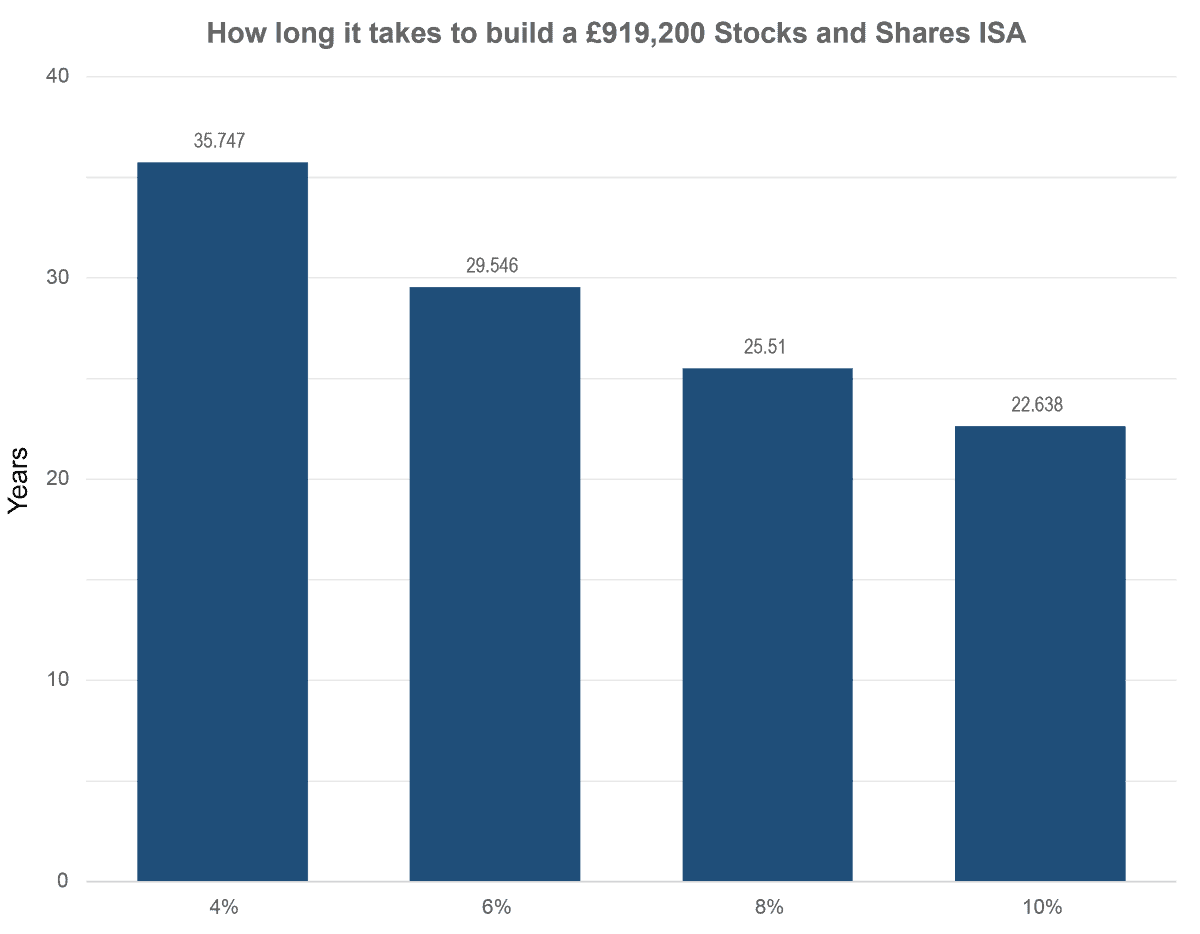

Using the widely followed 4% withdrawal rule, this implies an ISA worth approximately £919,200.

At first glance, that is a daunting figure.

However, it’s worth remembering that the earnings benchmarks from the ONS are based on gross income, before tax. By contrast, a Stocks and Shares ISA sits inside a tax-free wrapper, which can reduce the effective income requirement in real terms.

Even so, the scale of the target remains significant.

The key question isn’t just what the number is, but how long it might realistically take to reach it.

If an investor contributes £12,000 a year (£1,000 a month), the chart below shows how long it would take to reach a £919,200 portfolio under different return assumptions.

Chart generated by author

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice. Readers are responsible for carrying out their own due diligence and for obtaining professional advice before making any investment decisions.

Quality compounder in practice

That range of return outcomes highlights why the type of businesses held inside an ISA matters so much. Moving from lower single-digit returns to something closer to 8%-10% a year is not just a small improvement — over time, it can dramatically change the end result.

One example of a company operating at a very different level of growth quality is Diploma (LSE: DPLM).

The company’s latest half-year results underline that point clearly. Revenue rose 17% to £851m, supported by 15% organic growth — well ahead of its long-term 10% trend. This is not low-single-digit compounding; it is double-digit expansion at scale.

Profitability also strengthened meaningfully. Adjusted operating profit increased 33% to £209m, while margins expanded by 300 basis points to 24.5%. That combination of faster growth and rising margins is a hallmark of genuine pricing power, not just volume expansion.

Earnings momentum was even stronger. Adjusted earnings per share rose 36%, reflecting both operational leverage and disciplined execution across the group.

Growth drivers

Importantly, this is not being driven by a single lever. Diploma continues to expand through a mix of organic growth and disciplined acquisitions, completing 15 deals over the past year, while still maintaining a conservative balance sheet with leverage at just 0.8 times.

The result is a business delivering growth that consistently sits well above typical industrial peers — the kind of profile that, if sustained, supports the higher return assumptions shown in the ISA chart.

There are risks, particularly around acquisition execution and sustaining elevated growth rates. But the underlying quality of the compounding engine is clear to me.

Building an ISA capable of replacing a meaningful level of income is rarely about one decision — it is about the consistent ownership of high-quality compounders over time.

Diploma is one example of the type of business that can support that journey, but it is not the only one I am watching closely at the moment.

Should you invest £5,000 in Diploma Plc right now?

When investing expert Mark Rogers and his team have a stock tip, it can pay to listen. After all, the flagship Twelfth Magpie Share Advisor newsletter he has run for nearly a decade has provided thousands of paying members with top stock recommendations from the UK and US markets.

And right now, Mark thinks there are 6 standout stocks that investors should consider buying. Want to see if Diploma Plc made the list?

Andrew Mackie owns shares in Diploma.