Molina Healthcare (NYSE:MOH) was one of the worst-performing S&P 500 stocks of 2025. But it’s rebounded strongly from its recent lows.

The stock is up 57% from its 52-week lows. So is it time for me to think about selling my shares and redeploying the cash elsewhere?

Investment thesis

My investment thesis for Molina Healthcare is pretty straightforward. I think it has a durable competitive advantage in an important industry.

The company is a US healthcare provider. That means the amount it can charge is fixed – so there’s no differentiation on that front.

The firm’s advantage comes from having lower costs. It achieves this in several ways, from focusing on specific areas to maintaining a unified digital system.

Pricing for managed care can be cyclical. But a lower cost base allows Molina to remain profitable even when competitors are losing money.

That hasn’t changed in the last few months. But the question is whether it’s still worth hanging on to at today’s prices.

When to sell?

I don’t think Molina has unlimited growth prospects. So there should be a price at which I consider it overvalued and am willing to sell.

The company is in a difficult part of the cycle at the moment. Rising care costs have been cutting into profit margins.

This is true for managed care providers across the board. But the situation is almost guaranteed to improve in the future.

The premiums that operators collect are required to be actuarially sound. In other words, they have to give providers a chance at making money.

Given this, I think Molina’s situation has to improve in the next couple of years. But does the current share price now already reflect this?

Valuation

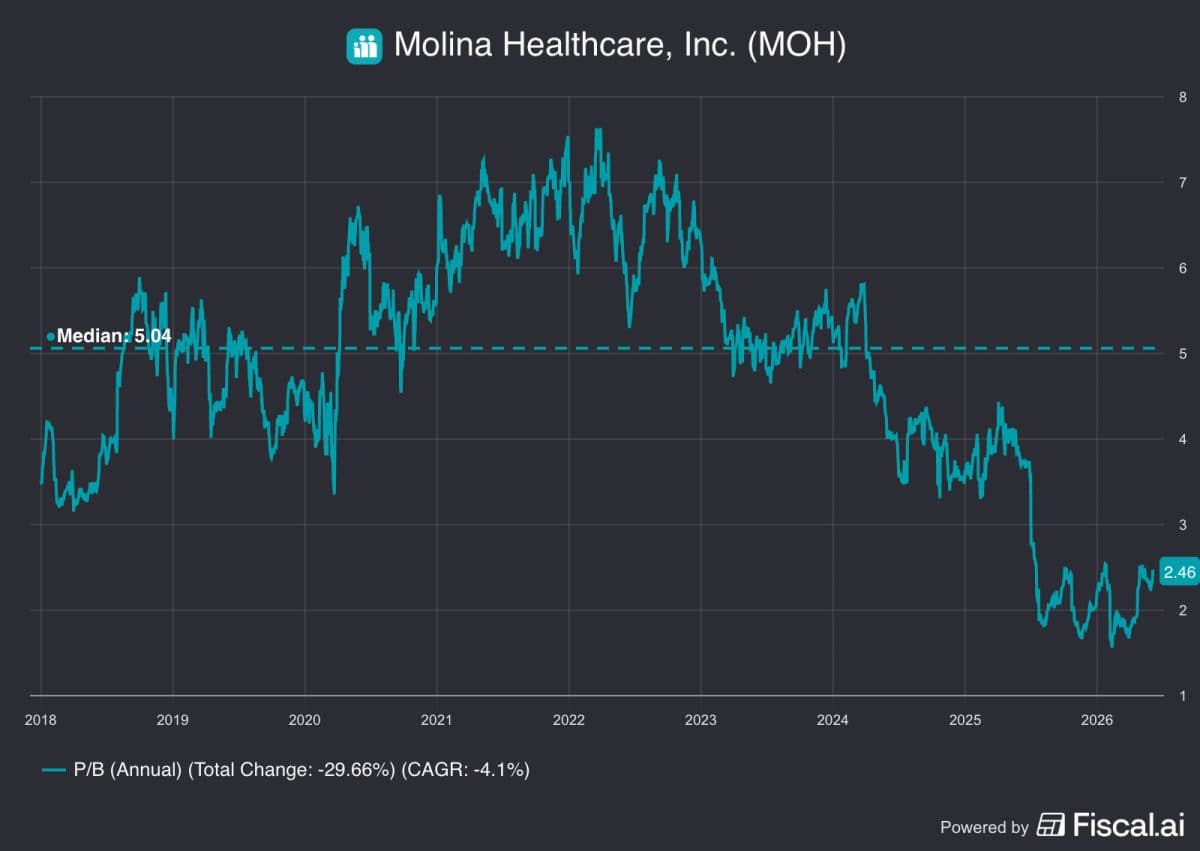

The price-to-book (P/B) multiple is a good way to value cyclical businesses. And Molina certainly fits into that category.

Source: Fiscal.ai

Despite the rising share price, the stock is still historically cheap in price-to-book terms. So it doesn’t look like a stretched valuation.

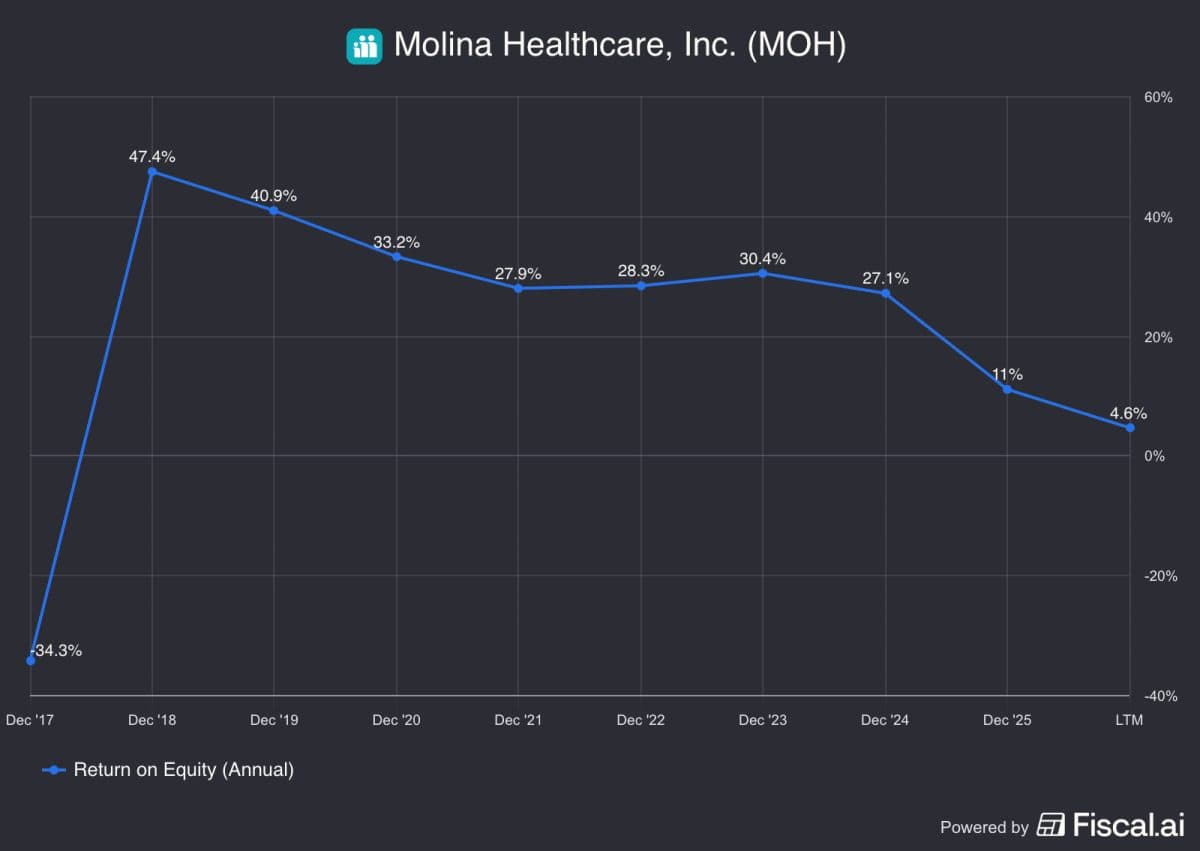

There’s also no question Molina is in a cyclical downturn. The firm’s returns on equity are well below where they have been over the last few years.

Source: Fiscal.ai

There’s no guarantee that the firm will get back to those levels. The risks of rising medical costs are ongoing threats.

Nonetheless, the time to think about selling stocks is when they’re expensive. And this doesn’t look like it’s the case to me right now.

What should I do?

Historically, figuring out when to sell stocks has been a weakness of mine. I’ve been too quick to move on and left returns behind. I’m mindful of trying not to make the same mistake with Molina. And that involves paying close attention to the business.

I think the firm is still in a relatively low part of the cycle. If I’m right, there’s still a long way to go in terms of improvements.

The stock might be up off its lows, but my view is that it’s too soon for me to sell. So I’m going to stick with it for some time.

Buying more is tricky in the context of balancing my portfolio. But I’ve no intention of selling any shares at today’s prices.

Should you invest £5,000 in Molina Healthcare right now?

When investing expert Mark Rogers and his team have a stock tip, it can pay to listen. After all, the flagship Twelfth Magpie Share Advisor newsletter he has run for nearly a decade has provided thousands of paying members with top stock recommendations from the UK and US markets.

And right now, Mark thinks there are 6 standout stocks that investors should consider buying. Want to see if Molina Healthcare made the list?

Stephen Wright owns shares in Molina Healthcare.