Reports of a potential takeover sent easyJet (LSE:EZJ) shares up 9.8% yesterday (1 June). But the long-term picture is less attractive.

The stock is 45% lower than it was five years ago and 65% below its pre-pandemic highs. And there’s an important lesson here for investors.

What’s the latest?

Castlelake – a US-based investment firm – already owns around 2.14% of the FTSE 250 airline. And it says it’s considering an offer for the rest.

The offer would be for at least 403.23p per share. But that’s already below the level the stock closed at yesterday.

There’s another ownership complication. European airlines have to be majority-owned by investors within Europe.

Ryanair CEO Michael O’Leary pointed this out when Elon Musk made noises about buying it. But it’s also an issue for Castlelake.

Given all of this, it might be a surprise that the stock has gone to 427.60p. The real story, however, might just be beginning.

A takeover target?

I doubt Castlelake is going to buy easyJet. But the firm’s interest might force other potential buyers to show their hands.

I’m not thinking of other private equity firms. I mean other airlines that might have a strategic interest in easyJet’s assets.

The firm has bases at Paris Charles de Gaulle and London Gatwick. And these are very valuable to an airline.

Runway slots at busy airports are limited and in high demand. And easyJet’s might be genuinely attractive to a competitor.

That’s where I think a real takeover might come from. But Castlelake’s speculation might jolt some other buyers into life.

Opportunities

According to easyJet, the takeover interest is highly opportunistic. The stock is down due to higher jet fuel prices.

There’s some truth to this, but it’s only part of the story. There’s also a balance sheet issue to pay attention to.

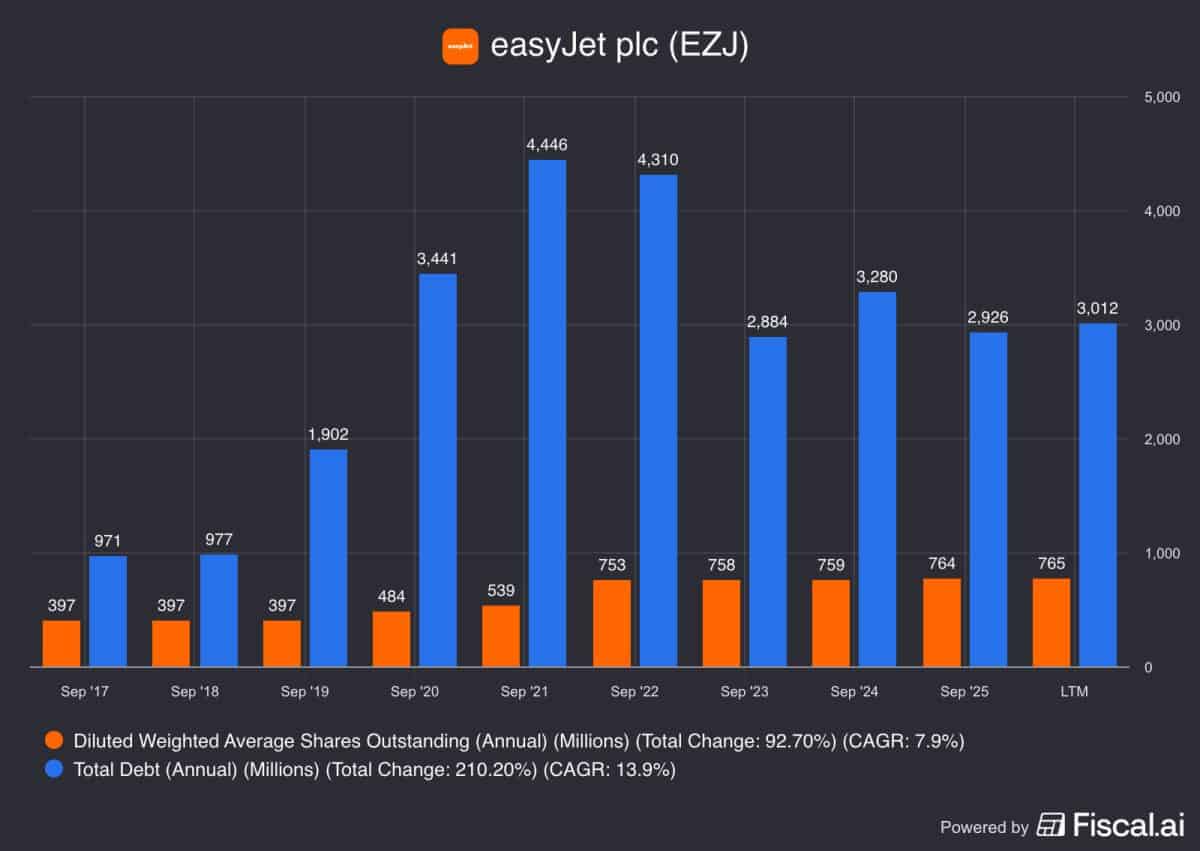

Ryanair just paid off the last of its bonds. Meanwhile easyJet still has £2.9bn in debt weighing on its share price.

Source: Fiscal.ai

The firm has almost twice as many shares outstanding as it had before Covid-19. Ryanair’s share count, by contrast, is lower.

This is why the share price is low. Jet fuel prices aren’t helping, but the real reason goes back much further than this.

Five-year returns

Over the last five years, easyJet’s share price has turned £10,000 into £5,437. And that’s not just about this year’s jet fuel prices.

Travel demand might have recovered sharply after Covid-19. But the damage to the business is more durable.

The lesson for investors is that buying falling shares indiscriminately isn’t a strategy. Looking at the underlying business is vital.

Castlelake might be looking to take advantage of a low share price. But I don’t see anything wrong with that.

It does mean, however, that investors who bought the dip five years ago are in danger of not getting their money back.

What next?

It will be interesting to see what happens next. Castlelake’s interest might draw other potential buyers out of the woodwork.

Equally, however, the takeover interest could evaporate entirely. So investors need another reason to think about buying the stock.

Is there one? The share price is down and it has some valuable assets, but my view is that there are more attractive opportunities to consider elsewhere.

Stephen Wright has no position in any of the companies mentioned.