Today (17 April), Barclays (LSE:BARC) shares are worth 134% more than they were in April 2021. It means someone who bought £5,000 worth five years ago would now be sitting on a paper gain of £6,746. If dividends are included, the return on the 2,645 shares would be even higher.

However, the same amount spent on the bank’s shares today would only stretch to 1,126 — some 1,519 fewer. Does this mean it’s too late to take a stake? Or could this amazing bull run continue? Let’s take a closer look.

Others have done even better

Although I’m sure shareholders will be pleased with Barclays’ recent share price performance, it has to be said that the four other banks on the FTSE 100 have done even better.

| Bank | Share price performance 18.4.21 to 17.4.26 (%) | Market cap at 17.4.26 (£m) |

|---|---|---|

| Standard Chartered | +264 | 39,772 |

| HSBC | +213 | 230,156 |

| NatWest Group | +188 | 49,692 |

| Lloyds Banking Group | +137 | 60,487 |

| Barclays | +134 | 60,451 |

Admittedly, Lloyds has only marginally outperformed the UK’s third-largest bank (by market-cap) but, nonetheless, investors have enjoyed a larger gain over the past five years.

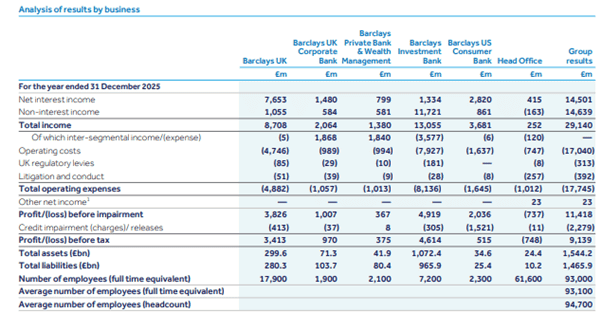

The reason for this is probably due to the mix of Barclays’ earnings. In 2025, 50.5% of its profit before tax was derived from its investment banking division, where returns can be volatile.

Earnings of the other banks are more concentrated in day-to-day transactional banking, mortgages, and other loans. The profit from these activities tends to be more stable and predictable. And they’re influenced more by interest rates. The post-pandemic rise in borrowing costs has helped improve the margin on traditional banking products and boosted earnings.

An attractive valuation?

In terms of valuation, Barclays has the second lowest historic (2025) price-to-earnings (P/E) ratio – beaten only by NatWest – and the lowest price-to-book (PTB) ratio.

The latter’s particularly interesting because Barclays had a book value over £30bn higher than Lloyds at the end of 2025. In fact, its total assets were a staggering £600bn more.

Yet, investors value Lloyds more highly. It has a P/E ratio of 14.8, compared to 9.4 for Barclays. Their PTB ratios are 1.3 and 0.8 respectively.

Clearly, investors view Barclays’ vast investment portfolio as high(er) risk and place less of a premium on its earnings. As a result, its shares trade at a discount to Lloyds and most of its peers.

My view

Even though I acknowledge that the blend of its earnings means it should be viewed differently to the Footsie’s other banks, I think investors are taking an overly cautious view when it comes to valuing Barclays.

Of course, a global economic slowdown would be bad news for its £362bn loan book. Increased financial distress is likely to lead to a rise in defaults and a general downturn in new business. And a recession could affect the performance of its investment arm.

However, as experienced investors know, global instability can bring about some lucrative opportunities. In particular, a chance to buy shares in some great companies at a knock-down price. I’m sure Barclays’ investment bankers have already taken advantage of market nervousness following recent events in the Middle East.

Personally, I think the same could apply to Barclays itself. Indeed, its share price is now 21% below its 52-week high. I believe it’s a high-quality business and that’s why I think it’s a stock to consider.