There are plenty of high-yielding shares around that I believe are worth considering for inclusion in a Self-Invested Personal Pension (SIPP). Here’s one that I think could be locked away and forgotten about for years to come.

Who?

With a current (10 April) yield of 8.4%, Legal & General’s (LSE:LGEN) shares are likely to be on the radar of income investors. However, experienced observers of the stock market know that high yields should be treated with caution.

A return nearly three times higher than that offered by the FTSE 100 could be a sign that the City’s expecting a cut. In effect, investors are demanding a premium for the perceived additional risk associated with owning stock in the savings and retirement group.

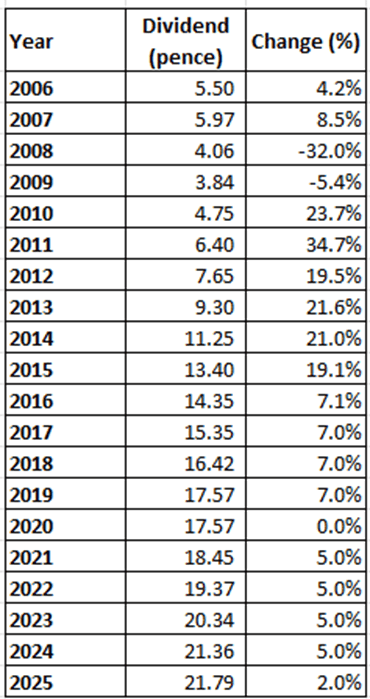

Personally, I think this is unjustified. Why? Well, history shows that Legal & General has an excellent track record of increasing its payout. Looking back over the past two decades, it kept it unchanged in 2020. It was last cut it in 2009 – the second year in a row — as a result of the global financial crisis. Otherwise, it’s been increases all the way.

Delving deeper

Of course, history may not be repeated. That’s because dividends are a distribution of profit, which means they can fluctuate in line with earnings. But a closer look at payments over the past two decades is revealing.

Maintaining the payout in 2020 – described as a “pause year” – was understandable given the uncertainty caused by the pandemic. And in 2008, the group reported a huge loss of £37.7bn on its investment portfolio. For context, its current market cap is £14.8bn.

In these circumstances, the group’s directors felt they had no alternative but to reduce its dividend. At the time, the group said financial markets were “left reeling after narrowly avoiding a systematic failure of the banking system and entering one of the sharpest, deepest recessions on record”.

This means that only in the most extreme circumstances has the group cut its dividend in the past 20 years. And during this period, we’ve had other economic downturns, Brexit, and a pandemic.

My view

Of course, there can never be any guarantees. But the group’s dividend looks safe for now. The current ceasefire in the Middle East has probably – if it holds – avoided a 2008-style market meltdown.

In 2025, the group reported a 9% increase in core operating earnings per share. It says it’s on course to increase its next two annual payouts by 2% a year. And it’s launched a £1.2bn share buyback programme.

However, there are a couple of things to keep an eye on. The group has signalled that it has a new target for its Solvency II ratio of 160%-190%. Okay, this is comfortably above the regulatory minimum of 100%. But it’s well below the 217% reported in June 2025.

And it operates in a competitive industry with challenger brands seeking to take market share.

But I think the group’s in pretty good financial shape. It’s continuing to secure a large number of pension schemes to manage from its large pipeline of potential new business. And its retirement division should do well as the State Pension age rises further.

In fact, I think it’s a top income share with an amazing yield that investors could consider.