The International Consolidated Airlines Group or IAG (LSE:IAG) share price has been a casualty of the Gulf conflict. And the causality is fairly obvious.

There has been significant re-routing and assets stuck in the wrong place. But it’s also an issue of jet fuel prices.

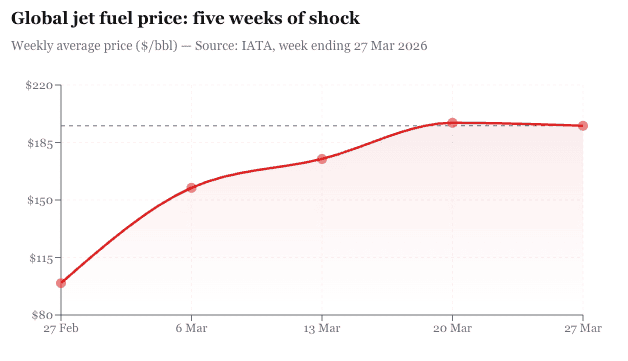

According to IATA data, the global average jet fuel price stood at $99.40 per barrel in the final week of February. By mid-March it was $175.

By the week ending 27 March, it had hit $195.19 — a near-doubling in five weeks. For an industry where fuel is typically the single largest operating cost, these rises are not background noise.

The benefits of hedging

IAG and its European peers don’t simply buy fuel on the spot market and hope for the best. They hedge. This means buying financial contracts — usually options or swaps — that lock in a price for future fuel purchases months or even years in advance.

It’s like an insurance policy if the prices spike. If prices fall, you’ve overpaid for protection — but most airlines consider that a price worth paying for budget certainty.

IAG looks reasonably well-covered for now. The group had around 75% of its Q1 2026 fuel requirements hedged, falling to roughly 64% in Q2, 58% in Q3, and 50% by Q4.

For the full year, that averages out at about 61%. In other words, the first half of 2026 is largely shielded, but as hedges roll off through the summer and autumn, IAG becomes increasingly exposed to whatever spot prices do next.

And the IATA crack spread — the refining margin between crude oil and jet fuel — has blown out to $81.44 per barrel, up 287% compared to a year ago, suggesting structural pressure beyond just crude.

A better entry point

Strip out the geopolitical noise and the numbers — which is where every investment thesis should start — are attractive.

IAG trades on a forward price-to-earnings of just 5.5 times and an enterprise value-to-EBITDA of 3.16. This is certainly more attractive than it was five weeks ago.

Analyst consensus sits at a price target of €5.70 — implying around 42% potential appreciation from here. Net debt has fallen dramatically, from nearly €10bn in 2021 to under €6bn last year. What’s more, the operating margins are incredibly strong for the sector.

What’s more, it’s also diversified in a way that’s easy to underestimate. British Airways on premium transatlantic routes, Iberia into Latin America, Vueling as a budget European operator, and Aer Lingus offering low-cost transatlantic. Different brands, different cabins, different geographies.

That diversification matters when one market goes cold.

The bottom line

I held IAG as my favourite in the sector for a long time. But after a significant re-rating (surging more than 200%), I shifted attention to Jet2, which I think offers considerably better value once you adjust for the balance sheet — a net cash position that IAG simply can’t match.

On a risk-adjusted basis, Jet2 is the more compelling opportunity to me and appears to be slightly better hedged. Nonetheless, both stocks are worth considering… investors just need to keep one eye on the conflict.