Few stocks on the London market have generated as much excitement as Rolls-Royce (LSE:RR) over the past few years. The stock has surged and the underlying business is genuinely in a great place. Operating margins have surged to nearly 25%, return on capital sits at 28%, and revenues are compounding at 13% annually.

These numbers are testament to a business that has been genuinely transformed under CEO Tufan Erginbilgiç. The long-term story — growing demand with civil aviation, the defence spending boom, and an expanding power systems division — remains highly attractive.

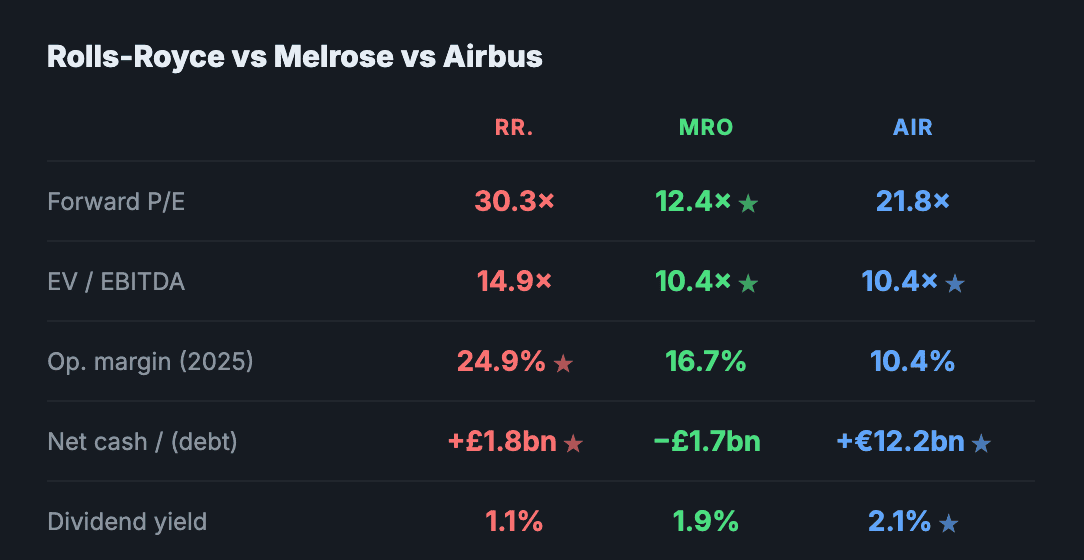

The issue however, is the price. At 30 times forward earnings and a price-to-earnings-to-growth (PEG) ratio over two, it’s by no means cheap. The risk is simple. If execution stumbles at all, that multiple compresses fast.

For new investors, the risk/reward may look a little stretched. The company still offers a huge amount, including in nuclear technologies, but the meaningful undervaluation isn’t there.

Something much cheaper

Melrose Industries (LSE:MRO) provides exposure to the same aerospace upcycle, but at a much lower valuation. Down 28% from its 52-week high, the stock trades at just 12.4 times forward earnings with a PEG ratio of 0.9, suggesting the market’s paying very little for what is forecast to be 16% forward earnings growth.

One key operational highlight here is that Melrose holds a sole-source position for 70% of its produced components. This means there’s no alternative supplier. That creates genuine pricing power and sticky, recurring revenue as the global fleet expands and ages.

The risk worth watching is the balance sheet, with net debt sitting a little ahead of where you’d want to see it. Currency fluctuations are also something to keep an eye on.

Hidden in plain sight

I think many Britons don’t realise that they can invest in Airbus. It’s a household brand and perhaps the most straightforward quality case of the three.

As one half of a global commercial aviation duopoly, Airbus has pricing power on a generational scale. Its order backlog stretches years into the future and revenue is forecasted to grow from €73bn in 2025 to over €100bn by 2028.

The earnings forecast — largely curated before the outbreak of war — is on a clear upward trajectory from €6.60 to €10.77 over the same period. On 2027 numbers, the stock trades on just 18 times earnings.

That’s a huge discount to Rolls. It also offers a 2.1% dividend yield and a has a rock-solid balance sheet with €12.2bn in net cash.

The main risk is operational. Airbus has struggled to ramp production rates to meet demand, and the supply chain has been problematic. Tariff exposure on transatlantic trade is also worth monitoring.

However, the valuation cushion is substantial, as is the moat.

All three companies are worth considering for long-term investors. But Rolls-Royce, for all its quality, asks investors to pay a premium price for a premium business. Melrose and Airbus, by contrast, offer a lot of the same at a considerably more attractive entry point.