The FTSE 250 can be a great place to find stocks that go unnoticed by other investors. And there’s one in particular that continues to catch my attention.

It’s a business that’s managed to average 32% annual growth for the last 44 years. And it’s still going strong. Care to guess what it might be?

Retail

The answer is Frasers Group (LSE:FRAS). Mike Ashley started what would eventually become the FTSE 250 retail firm that exists today in 1982 with a £10,000 loan.

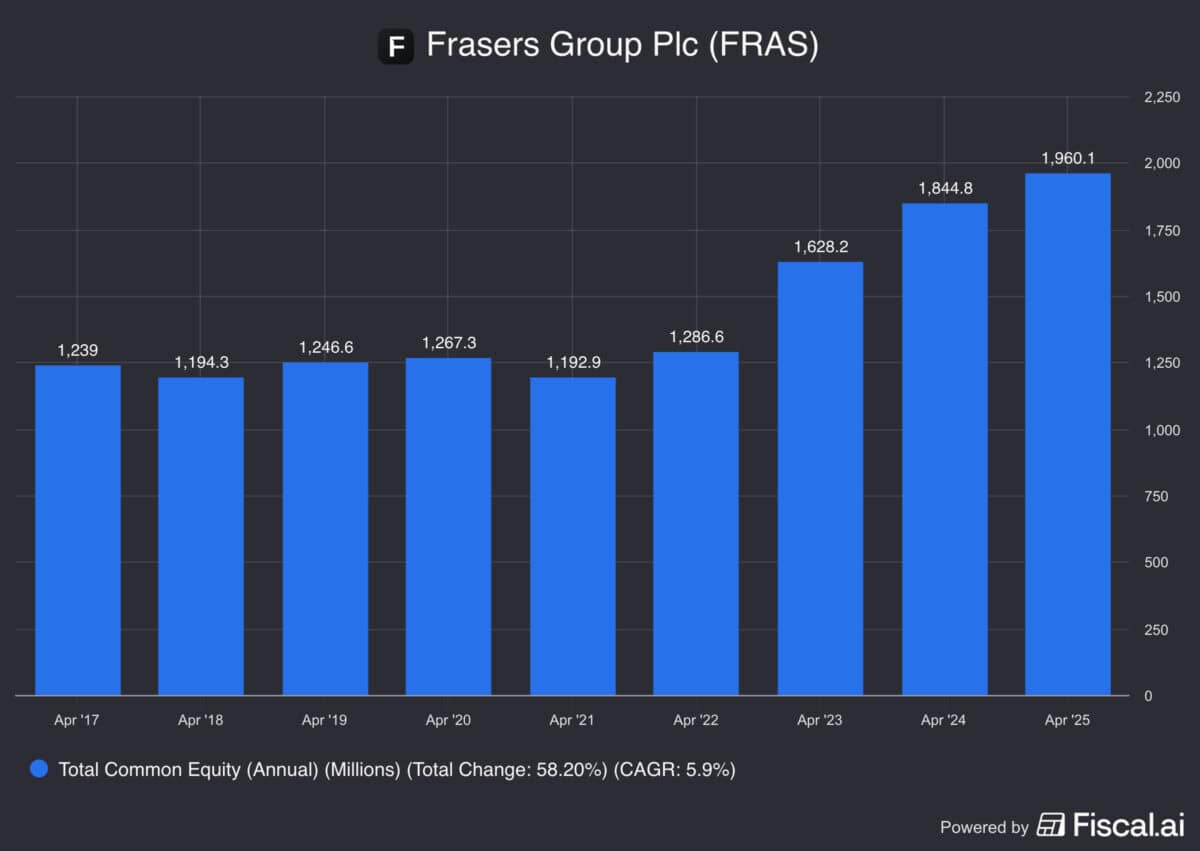

Jumping ahead to today, the company’s book value is £1.99bn. That implies an average annual growth rate of around 32% over the last 44 years, which is an incredible achievement.

The company, which owns Sports Direct, Flannels and more, isn’t still growing like it was in its earliest years. But it’s managed an annual average of 9% over the last five years, which is still a very strong result.

Source: Fiscal.ai

On top of this, the stock isn’t particularly expensive. It’s trading at a price-to-book (P/B) ratio of 1.25, which isn’t at all high for a business that’s still putting up strong growth numbers.

Growth

Whether it’s sofa.com or the CBS Arena, Ashley’s known as a bargain hunter. But it’s no accident the company has grown so much since it was first formed.

It’s explicitly set up for growth. One example of this is the fact that it doesn’t pay a dividend, which allows it to retain all of the cash it generates to find acquisitions.

Passive income investors should probably look elsewhere. But while the company keeps moving forward at 9% a year, growth investors don’t really have much to complain about.

There are some risks to consider, but I think this is a stock that doesn’t necessarily get the attention it deserves. So investors might well want to take a closer look.

Strategy

Since Mike Murray (Ashley’s son-in-law) took over as CEO in 2022, Frasers has undergone a deliberate and strategic shift towards higher-end products. And that’s not all.

The firm has been investing heavily in its technology stack. It’s become a leader in Agentic Commerce in Europe and its Frasers Plus product gives it data about more than one million customers.

The transition might be the right one at the right time, but it marks a move away from the approach that gave it so much success in its early days. And that can also be risky.

Investors don’t seem to be giving the firm much credit. But the presence of Ashley as an adviser should reassure shareholders that it’s still ready to do things. Like buying a 5.8% stake in sportswear giant Puma.

A stock to buy?

UK retail stocks can be a bit of a mixed bag. But it’s hard to argue with the success Frasers Group has had since 1982.

It’s even harder to think of someone who understands UK retail better than Ashley. Simon Wolfson at Next might be one candidate, but that’s the only name that comes to mind.

Despite a change of direction, the company’s still growing impressively. So I think UK investors should take a serious look at what could be a very nice long-term investment.