Sometimes, when a stock pulls back from a recent high, an opportunity suddenly presents itself to buy into a quality business at a knock-down price. I say ‘suddenly’ because such reversals are often unexpected.

But is this the case with Lloyds Banking Group (LSE:LLOY)? After rallying 34% in a year, is it really a surprise that the stock’s now (6 March) changing hands for 14% less than it was four weeks ago? Or, does this suggest investors believe it was over-priced? Let’s take a look.

Events, dear boy, events

Undoubtedly, some of the fall is due to this week’s events in the Middle East, which are beyond the control of the bank. But if the conflict continues for much longer, I’m sure there will be further nervousness among investors. However, setting this to one side, there’s some evidence to suggest that Lloyds’ valuation was becoming stretched. Perhaps a large number of shareholders believe it’s time to bank some profit?

Often, a decision to exit a position coincides with the publication of results. Indeed, all of the FTSE 100’s five banks have now reported their 2025 earnings. This presents an opportunity to make a comparison of current valuations.

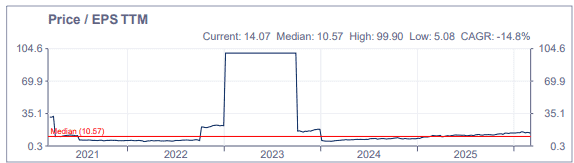

According to figures compiled by the London Stock Exchange Group, Lloyds has a trailing 12 months price-to-earnings (P/E) ratio higher than its peers. And as the chart below shows, it’s been steadily rising over the past year, or so. It’s now above its five-year average (median) of 10.57.

It’s a similar story with the bank’s price-to-book ratio. The recent share price rally has created a bigger mismatch between its stock market valuation and its underlying net assets position, as reported on its balance sheet.

In some respects, this doesn’t matter as long as the bank can continue to grow. Rolls-Royce is a perfect example of investors seemingly prepared to overlook an apparently generous valuation multiple – its stock trades on nearly 45 times its 2025 earnings. Rolls-Royce commands this premium because of its frequent earnings upgrades. This continues to give momentum to its share price.

What about Lloyds?

And if analysts’ predictions prove right, the Lloyds share price could beat its 52-week high. That’s because they’re expecting earnings per share to rise to 12.8p by 2028. Applying its five-year average P/E ratio to this figure suggests its shares are worth 135p, 38% above today’s price.

Moreover, analysts are forecasting 2026-2028 dividends of 14.94p a share. This means someone investing £10,000 today could generate passive income of £1,532 over the next three years. Of course, there can be no guarantees when it comes to dividends. If the bank’s earnings were to come under sustained pressure, it would probably cut its payout to help preserve cash.

While I like to think I’m a positive person, these forecasts seem too optimistic to me, especially for a bank that generates most of its income domestically.

On Tuesday (3 March), the Chancellor announced that the Office for Budget Responsibility had downgraded its 2026 UK growth forecast. Business confidence is shaky and consumers remain under pressure. I feel an 83% increase in EPS by 2028 – compared to 2025 – is a bit of a stretch.

On this basis, I believe there are many more exciting opportunities to consider elsewhere.