The Rolls-Royce (LSE:RR) share price has clocked up another impressive year. As a result, anyone who invested £1,000 in the stock five years’ ago now has an investment worth £9,868.

Analyst price targets for 2026 suggest another strong year for the FTSE 100’s version of Nvidia could be on the cards. So despite the stock being up 889%, is there still a buying opportunity?

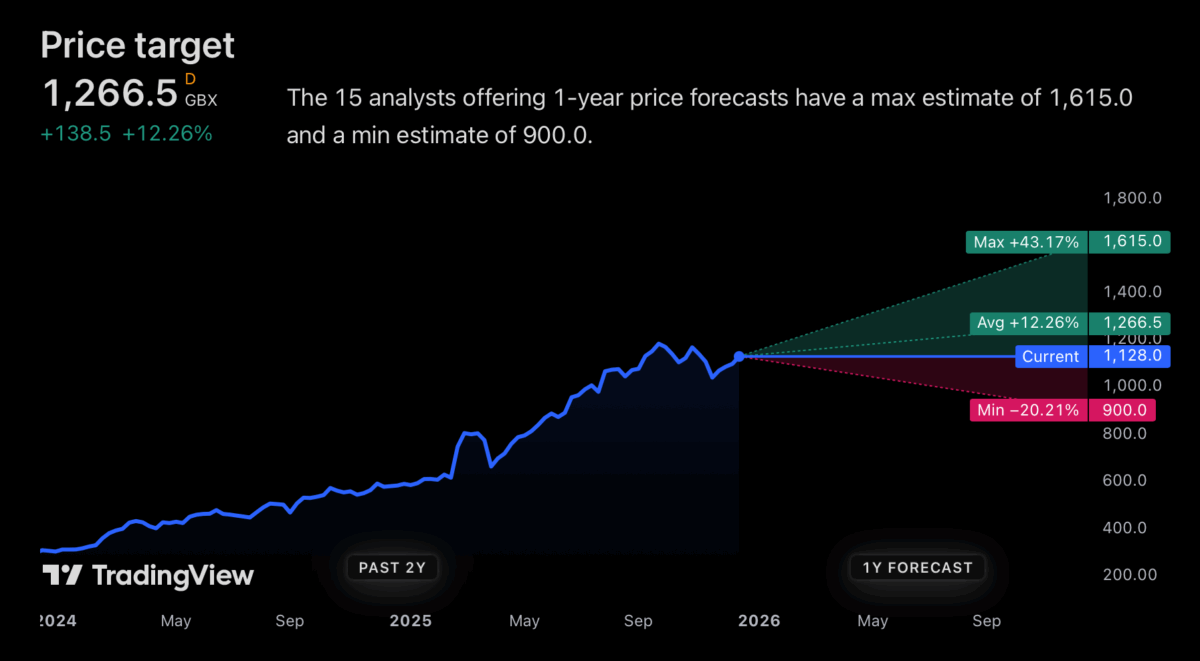

Analyst forecasts

Right now, the average analyst price target for the stock is around 12% higher than the current level. That’s more than the FTSE 100 manages in an average year.

Source: TradingView

If things go well, there’s a case for thinking the Rolls-Royce share price could do even better. The highest estimate is just over £16 – 43% above where the stock’s trading right now.

It’s trading at a price-to-earnings (P/E) ratio of 16, but that includes some one-off boosts to profits that won’t be repeated. Adjusting for these, the multiple is more like 35. That means some things will need to go right for the firm and these can’t be guaranteed. And that means the high multiple is a risk with the stock going into 2026.

Air travel

In recent years, the biggest force propelling Rolls-Royce forward has been its civil aviation business. Air travel demand has been strong and this looks set to continue in 2026. There is, of course, always a risk with this industry. Downturns can come suddenly and out of nowhere when businesses are least expecting them and they can have a big impact.

Economic growth has been relatively weak recently and that means a cyclical downturn is a real possibility. And high fixed costs mean margins can contract quickly.

Importantly though, Rolls-Royce has been at the centre of a couple of important long-term trends recently. So even if air travel demand falters, there might still be room for positivity.

Defence and power

Two of the biggest themes in 2025 have been defence and artificial intelligence (AI). These are both areas that Rolls-Royce has exposure to, either directly or indirectly.

NATO commitments to increase defence spending should boost demand for aircraft, submarines and ships. And that’s like to bring increased demand for the firm’s engines.

In terms of AI, the data centres that big tech companies have been building need reliable backup power. And Rolls-Royce provides both generators and battery solutions.

Importantly, both of these divisions should provide growing earnings well beyond 2026. So they’re also key reasons to be positive about the stock over the long term.

Long-term investing

I’m a little hesitant when it comes to Rolls-Royce shares next year. Anything can happen with the firm’s civil aerospace division and the stock can move sharply in either direction.

From a long-term perspective things look a bit more positive, with the company exposed to some key growth industries. And that means investors might want to take a look.

My sense though, is that it’s hard to see this as the best FTSE 100 stock to buy right now. While it has a lot of momentum, I think there could be better opportunities to explore.