According to the latest data from Bank of America, fund managers looking to stand out from the crowd in 2026 are looking at UK stocks. But should ordinary investors do the same?

Earning above-average returns in the stock market involves doing something different. And that might be looking for undervalued opportunities in the FTSE 100 and the FTSE 250.

Outperforming the stock market

Outperforming the stock market’s hard even for the best investors. But those who just buy funds that track an index give themselves zero chance of doing this.

There’s nothing wrong with earning an average return. Historically, stocks and shares have generated better long-term returns than cash and bonds and this is no accident.

For professional fund managers though, this is no good. They need to find ways to do better than average to justify charging their clients fees for managing their money.

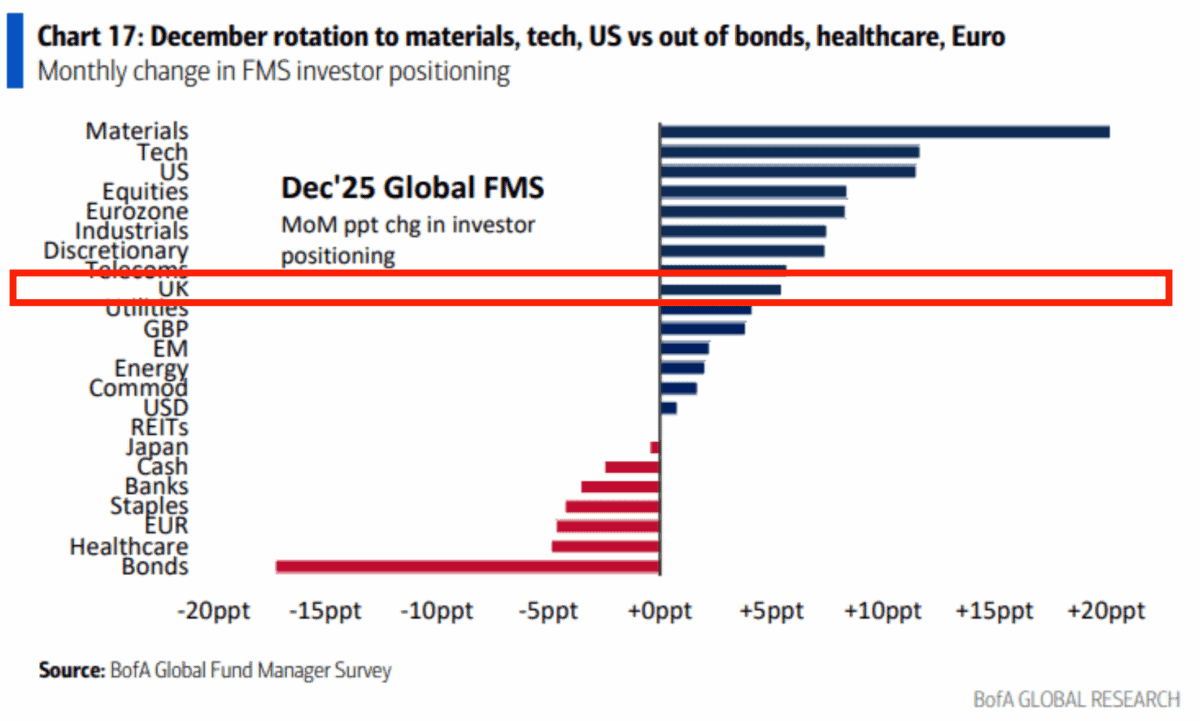

The Bank of America Fund Manager Survey comes out monthly. And it gives investors an interesting insight into what the smart money’s thinking and doing.

Follow the money…

According to the latest data, the most popular stocks for fund managers as 2026 approaches are technology, materials, and US equities. But a select few are taking an interest in UK shares.

Source: Hedge Fund Tips

In other words, UK stocks are far from a consensus choice, but a handful of investors are taking a chance on a potential opportunity. And I think that’s worth paying attention to.

Fund managers typically have to tell their clients how they’ve done each year. And that makes it natural to think in 12-month periods (or potentially even shorter).

I’m looking further ahead with my investing. But even in that context, there might be buying opportunities in UK stocks now that might not be there at the end of next year.

UK value

On the subject of contrarian views, JD Wetherspoon’s (LSE:JDW) a UK stock I plan to own for a long time. It’s been a tough year for the hospitality industry, but the stock’s up 23%.

Unlike many investors, I think the tough environment might well be part of the reason why the company’s done well. As competitors have been closing venues, the firm has seen like-for-like sales increasing.

It’s an unorthodox view, but I think the biggest risk is the government attempting to help the hospitality sector. My sense is it would help JD Wetherspoon’s competitors than its business.

The company’s cost advantage comes from its scale and its freehold assets that reduce lease liabilities. And I’m willing to bet it’s going to be one that endures for a long time to come.

Doing things differently

Whether it’s the next 12 months or 12 years, investors can only get above-average results by doing something different. But it doesn’t have to be anything drastic.

It can be as simple as thinking that UK shares are better value than most investors think. And that seems to be the view of some fund managers right now.

JD Wetherspoon shares have outperformed in 2025 and I think they can do the same over the long term — or even quicker.