At the time of writing (1 December), Lloyds Banking Group (LSE:LLOY) shares are changing hands for around 95p. This means they’re just 5.3% away from reaching the psychologically important barrier of £1.

Will they get there? Or could they go in the opposite direction? Let’s review the evidence.

The bearish view

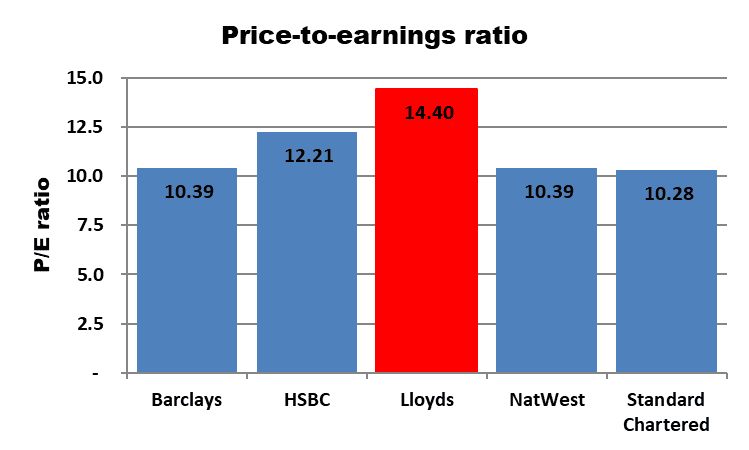

Based on the forward (2025) price-to-earnings (P/E) ratios of the FTSE 100’s five banks, Lloyds’ shares are the most expensive. If they were rated in line with the average, they would be around 25% cheaper, at 76p.

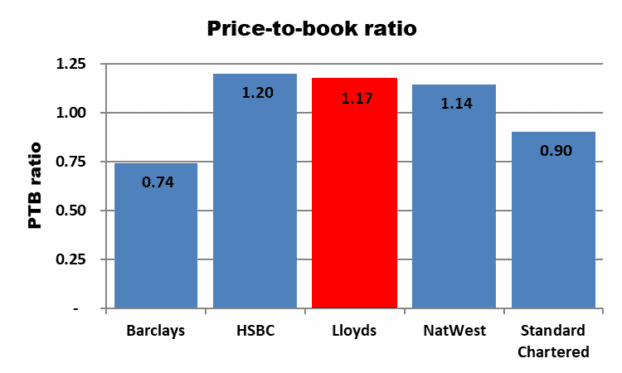

Looking at the balance sheets of the five, Lloyds is the second most expensive. It has a price-to-book (PTB) ratio of 1.17. According to McKinsey & Company’s latest research on the global banking industry, the average PTB for the sector is one. In other words, banks are generally valued in line with their net asset value.

This might sound reasonable but many industries attract far higher valuations. McKinsey’s report cautions that investors appear to be questioning the “sustainability of bank’s recent highs”. It blames “declining interest rates [and] shifts in technology and consumer behaviour”. The management consultancy also notes that fintechs, private credit firms, and wealth managers are gaining customers from more traditional financial institutions.

So Lloyds might not be able to command a stock market valuation significantly higher than its accounting value.

Also, its near-total reliance on the UK economy for its income could be an Achilles’ heel. Last week’s Budget saw growth forecasts for 2026 and beyond downgraded.

The bullish view

If the analysts are correct, the bank’s recent share price rally isn’t over yet. They have an average 12-month share price target of 99.5p. Okay, that’s short of the magic three figures but it’s close enough. The most optimistic forecast suggests 110p is a fair price.

This rosy picture is underpinned by an expectation that, compared to 2024, earnings per share will have grown 79% by 2027.

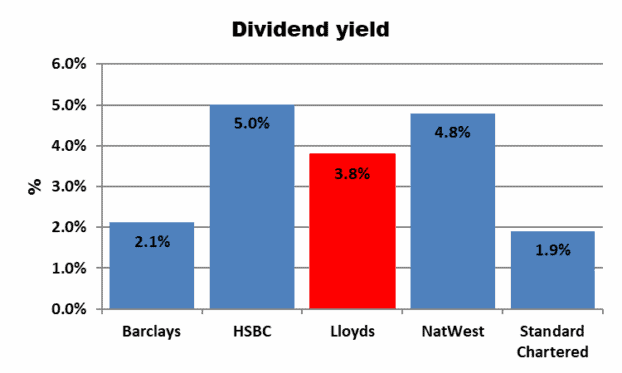

And the stock’s good for income too. Based on the past 12 months, it’s yielding 3.8%. Although it’s currently not the highest of the five, brokers are expecting its dividend to increase by 51% over the next three years. This gives it a forward yield of 5.1%.

My view

On reflection, I’m leaning more towards the bearish arguments. I already think Lloyds shares are on the expensive side so I reckon the scope for further growth’s limited. That’s why the stock’s not for me.

Having said that, I wouldn’t be surprised if the shares did reach 100p before the end of 2025. But for them to go much higher, I suspect something fairly significant has to happen. However, the only major events I can see occurring are negative ones, centring on the UK economy, which appears fragile.

Despite my concerns, I don’t think the shares will fall as low as 76p. The bank remains popular with smaller investors – it has more shareholders than any other company in the country – and its earnings are growing. This should help support its share price.

And even though I have concerns about Lloyds’ valuation, I still think it’s a well-run quality company. I just think the FTSE 100’s other banks look a bit cheaper at the moment.